Queensland pushes ahead as southern beef kills ease

Market Morsel

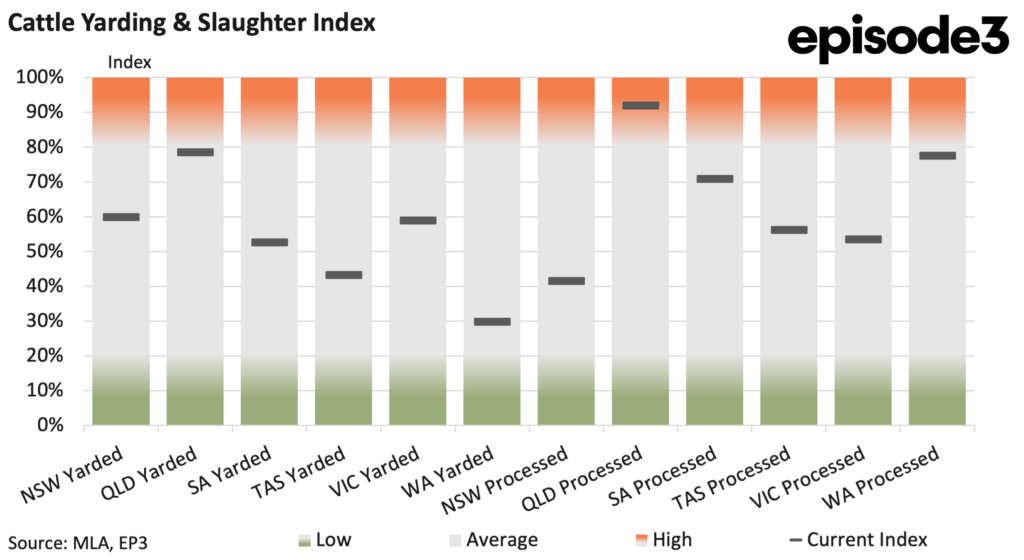

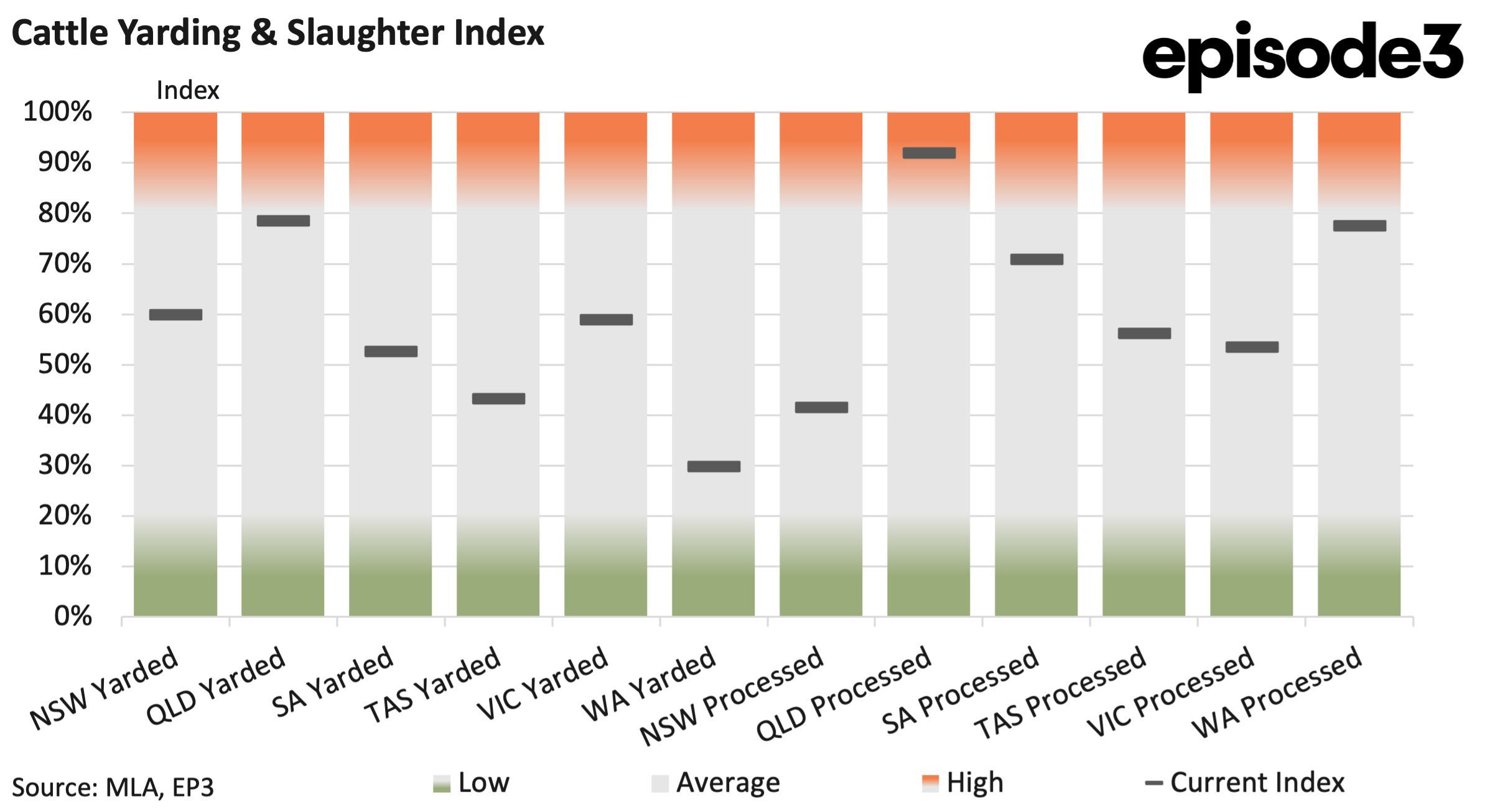

The latest Cattle Slaughter and Yarding Index shows the market has become increasingly fragmented as winter takes hold, with processor activity diverging sharply between regions while cattle prices begin to tell a more nuanced story. Unlike previous months, the June data does not point to a simple tightening or loosening of supply. Instead, it reflects a market where regional availability, export conditions and processor confidence are all pulling in different directions.

The most notable change during June occurred in Queensland. Yardings lifted from 56 percent to 79pc, signalling a significant increase in cattle coming forward. Processing activity also increased, rising from 79pc to 92pc. Queensland was the only major state to record higher slaughter activity during the month, reinforcing its position as the country’s primary source of cattle supply. Elsewhere the picture was very different.

New South Wales yardings eased from 79pc to 60pc while processing activity dropped sharply from 95pc to 42pc. South Australia recorded higher yardings, rising from 30pc to 53pc, but processing eased from 88pc to 71pc. Victoria experienced a modest increase in yardings from 54pc to 59pc, yet slaughter activity fell substantially from 95pc to 53pc. Tasmania also saw both supply and processing retreat, with yardings falling from 72pc to 43pc and slaughter declining from 90pc to 56pc. Western Australia remained relatively stable, with only modest movements in both measures.

Together, the June figures highlight a market that is becoming increasingly regionalised. Queensland continues to carry the weight of national cattle availability, while much of the southern processing sector appears to be operating more cautiously. The contrast between yardings and slaughter is particularly important. Higher yardings would normally be expected to translate into stronger processor activity. Instead, outside Queensland, processors have generally reduced throughput despite cattle availability improving in some regions. This suggests the market is now being influenced by more than simply the number of cattle available for sale.

Export conditions have become more challenging, particularly for manufacturing beef, while changes to trade settings have altered the economics of several important overseas markets. At the same time, processors have become more selective in their procurement strategies as margins remain under pressure.

The latest MLA price indicators reinforce that view with the processor cow prices declining by 8 cents over the last month. Heavy steer prices have also eased, down 5 cent over the same period. These are the two categories most closely aligned with export processing demand, and both remain under pressure. The softer pricing reflects a market where processors have greater leverage over finished cattle than they did only a month earlier.

Queensland’s increased throughput has undoubtedly contributed to that outcome, providing processors with greater access to cattle even as export returns have softened. The younger cattle market, however, is telling a different story. Feeder steer prices have increased by 33 cents over the past four weeks and feeder heifers have risen by 20 cents. Restocker yearling steers are up 28 cents.

These movements suggest confidence remains relatively strong further back through the production chain. Restockers and feedlots continue to compete for younger cattle despite weaker conditions for processor categories. Improved seasonal conditions across many grazing regions have encouraged producers to retain cattle and rebuild numbers where feed availability allows. The result is a distinctly two speed market. Finished cattle destined for immediate slaughter have softened as processors respond to changing export conditions and increased northern supply. At the same time, younger cattle continue to attract strong competition from buyers looking beyond the current marketing season.

That divergence is one of the more interesting features of the current market cycle. Only a few months ago processor cows, heavy steers and young cattle were all moving broadly in the same direction. Today the market has clearly separated into different demand streams. The CSYI data reflects this changing dynamic with Queensland processors continue to operate at high levels because cattle are available. Southern processors appear to be balancing tighter regional supply against a more uncertain export environment, resulting in lower throughput despite improvements in yardings in some states.

The next few months will largely depend on whether Queensland continues to provide elevated cattle numbers and whether southern supply begins to recover as winter progresses. Export demand will remain equally important. If offshore markets stabilise, processors may become more willing to increase competition for finished cattle. If export returns continue to soften, pressure on processor categories could persist despite relatively stable overall cattle numbers.

Supply remains adequate in some regions and increasingly constrained in others. Processors are responding differently depending on location and market exposure. The price data suggests those differences are now flowing directly into cattle values, creating a market where geography is becoming almost as important as the number of cattle available.