Shorter Easter week prompts tighter supply

Market Morsel

The latest sheep and lamb yarding data reveals a notable tightening in supply over the past four weeks, driven largely by the shorter Easter processing week and the associated reduction in market throughput. This seasonal disruption has temporarily constrained offerings across saleyards, contributing to firmer pricing outcomes and reinforcing the underlying strength evident in the sheep meat market.

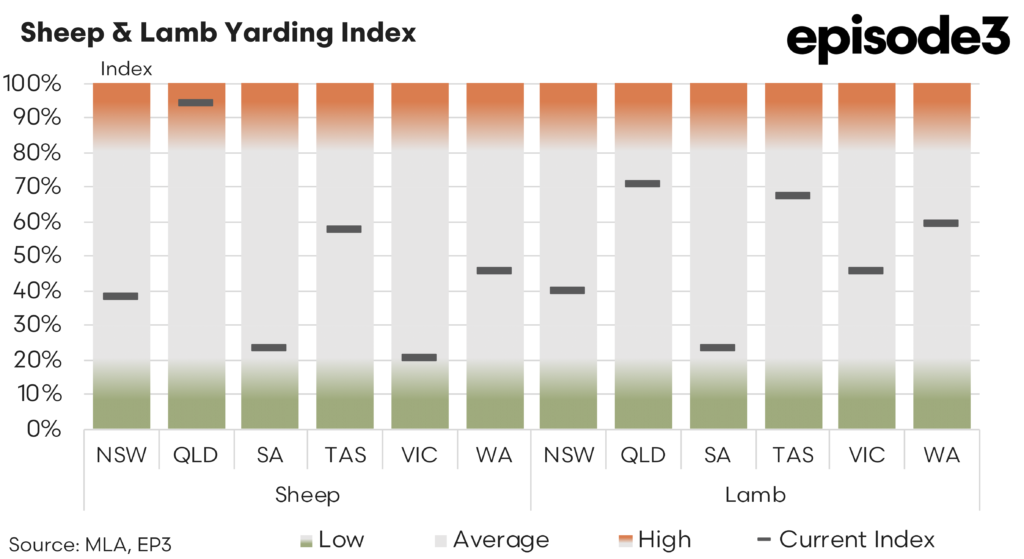

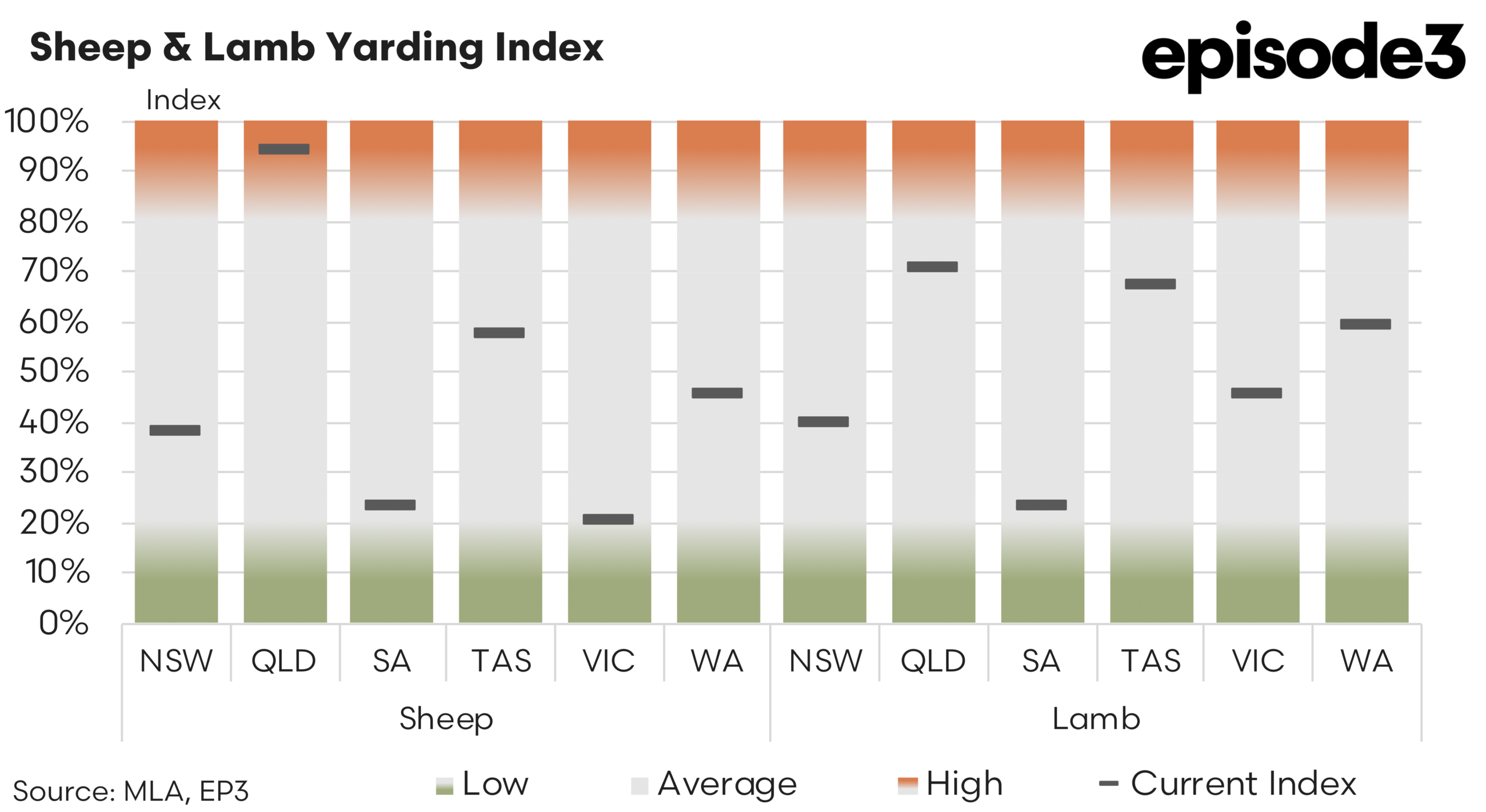

Sheep yardings have declined across several key producing regions, highlighting the impact of the abbreviated processing schedule on supply flows. In New South Wales, sheep yardings fell from 71 percent in the February to March period to 38pc between March and April, signalling a sharp contraction in throughput. Victoria recorded a similar trend, easing from 25pc to 20pc, reflecting tighter availability and reduced marketings.

Western Australia also experienced a decline, slipping from 60pc to 46pc, indicating that supply in the west has moderated alongside eastern states. Tasmania showed a drop from 75pc to 58pc, reinforcing the broader national trend of reduced yardings. South Australia remained relatively subdued, easing from 34pc to 23pc, which underscores the persistently constrained supply conditions in the state.

Queensland stood apart from the broader national pattern, lifting from 83pc to 94pc, suggesting that northern producers continued to bring stock forward despite the shortened trading period, although yarding numbers in Queensland are a tiny fraction of the southern states.

The sheep yarding data points to a tightening national supply environment, albeit with regional variability driven by seasonal conditions and market timing. The widespread reductions across most states indicate that the Easter disruption has compounded an already tightening supply cycle.

Lamb yardings have followed a similar trajectory, with declines evident across the majority of major producing regions. In New South Wales, lamb yardings dropped from 58pc in the February to March period to 40pc between March and April, reflecting reduced offerings as the seasonal flush fades. Queensland also recorded a modest rise, lifting from 67pc to 71pc when comparing the same periods, though supply remains relatively robust by historical standards.

Western Australia fell from 76pc to 59pc, signalling a notable contraction in throughput in the nation’s largest lamb exporting state. Tasmania saw an increase from 40pc to 67pc, indicating a temporary uplift in availability, while Victoria rose from 33pc to 46pc, suggesting improved throughput relative to earlier in the season. South Australia edged higher from 21pc to 23pc, although levels remain historically subdued.

Despite these regional increases, the broader national trend reflects a moderation in lamb supply, particularly across New South Wales and Western Australia. The tightening in yardings has been mirrored by strengthening price movements across most MLA reported indicators over the past four weeks.

Heavy lamb prices have risen by approximately 32c, reaching around 1,134c per kilogram carcase weight, reflecting increased competition for finished stock. Light lamb has also delivered gains, lifting by nearly 24c over the same period to sit at approximately 1,163c per kilogram carcase weight. Merino lamb prices have strengthened by around 49c, highlighting firm demand across wool-bearing categories.

Trade lamb has also posted solid gains, rising by roughly 46c over the past month to approach 1,205c per kilogram carcase weight.

Restocker lamb has recorded a substantial increase of approximately 42c, reinforcing confidence among producers and signalling expectations of continued market strength. Mutton prices have also firmed, rising by nearly 31c over the four-week period to sit above 828c per kilogram carcase weight.

This upward movement aligns with the tightening in sheep yardings and reflects the reduced availability of mature stock. The broad-based improvement in pricing suggests that the market has responded quickly to the contraction in supply. Processors have been forced to compete more aggressively for limited offerings, while restockers have re-entered the market with renewed confidence.

The strength in lighter categories indicates that demand remains robust across both domestic and export channels. The shorter Easter week has played a pivotal role in shaping these trends, temporarily restricting processing capacity and reducing the number of animals presented at saleyards. Such seasonal disruptions often create short-term supply squeezes, which in turn support prices as competition intensifies.

However, the extent of the recent price increases also points to underlying structural tightness rather than merely a temporary holiday effect. Sheep availability remains constrained across several key regions, providing support to mutton values. At the same time, lamb supply, while still present, is no longer expanding at the pace observed earlier in the season.