Tougher Q1 for beef processors

Get short video updates on your phone

For quicker updates as markets move, follow @themeatwatcher on Instagram. I regularly post short summaries and charts breaking down what’s happening in meat proteins and broader ag markets so you can stay across the key moves without having to read through pages of analysis. If markets are moving quickly, that’s usually where the updates will land first.

Beef Processor Trading Conditions Update March 2026

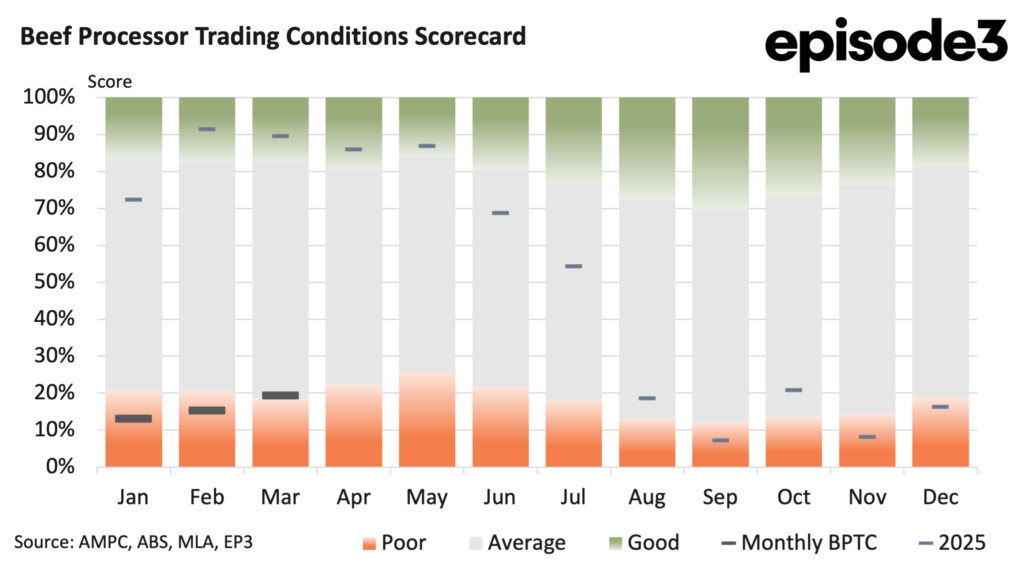

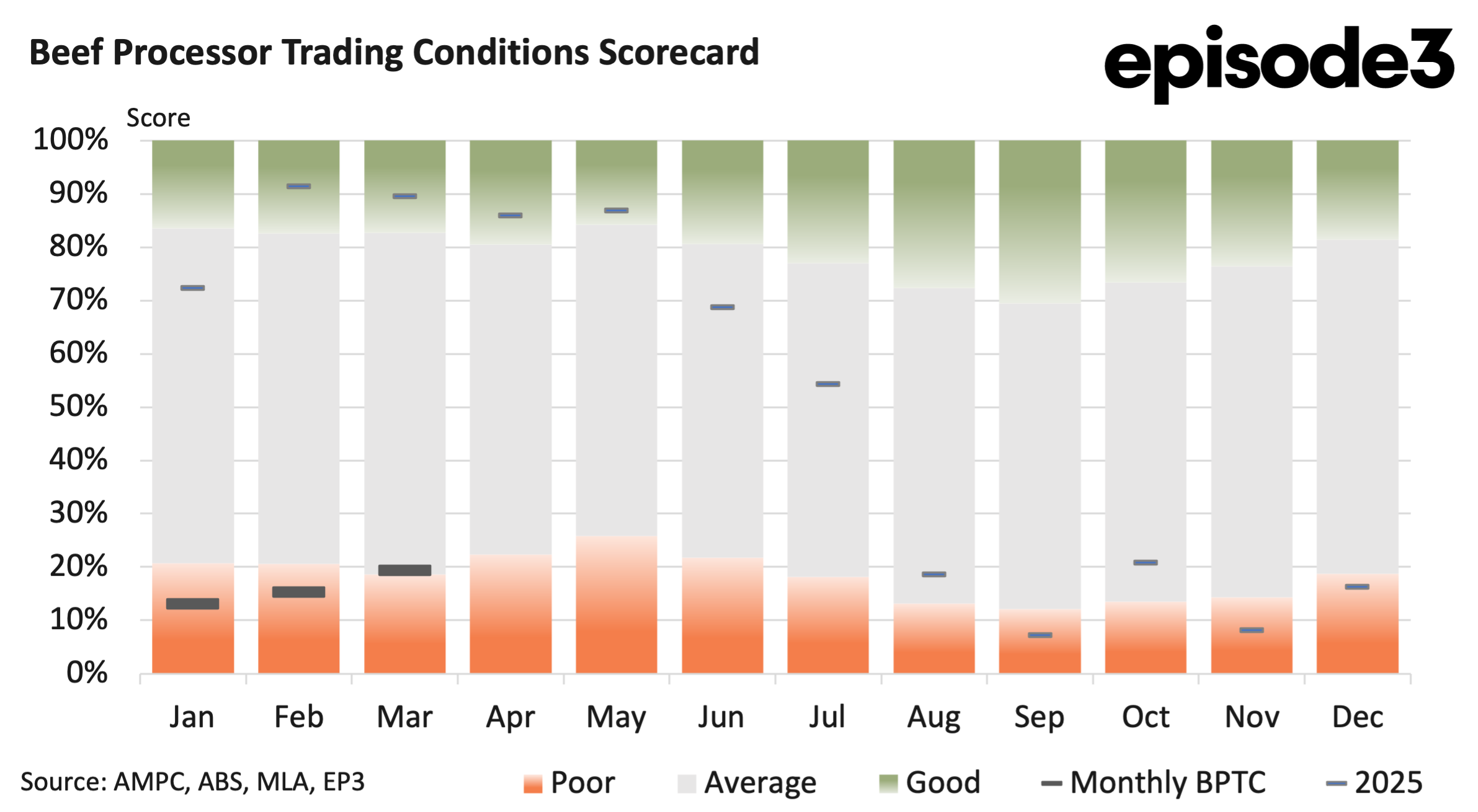

Beef processor trading conditions improved modestly through the first quarter of 2026, but the sector remains a long way from the strong profitability seen at the same time last year. The Beef Processor Trading Conditions index lifted from 13 percent in January to 15pc in February before reaching 19pc in March. This leaves the Q1 average sitting at 16pc for 2026.

While the direction of movement through the quarter has been positive, the broader comparison remains sobering for the beef processing sector. During Q1 2025, the BPTC index averaged 84pc. That represents one of the strongest operating environments seen for processors in recent history.

By comparison, current conditions remain subdued and highly compressed. The contrast between the two periods highlights how dramatically the margin environment has shifted over the past twelve months. Although export values have improved, livestock input costs have risen far more aggressively, squeezing processor margins throughout the supply chain.

Heavy steer prices are now 29pc higher than they were during Q1 last year. Young cattle prices have increased by 34pc over the same period. Processor cow values have also lifted sharply, up 29pc year on year. These increases represent a significant escalation in procurement costs for processors.

Livestock remains the single largest input expense for the processing sector, meaning even moderate increases can place pressure on profitability. The scale of the rises seen over the past year has therefore had a substantial impact on operating conditions.

Export markets have provided some support. Average export values into the United States are up 8pc compared to Q1 last year. Japan has improved by 13pc, South Korea by 5pc, and China by 19pc. Across the top four export destinations, average beef export values have increased by 11pc year on year.

That represents a reasonably solid performance from the revenue side of the equation. However, it has not been enough to offset the rise in livestock prices. This divergence is the key story sitting behind the BPTC figures. Processors are paying materially more for cattle, but export returns have not increased at the same pace. As a result, the margin spread has narrowed significantly compared to last year.

Domestic market conditions have also shifted. Retail beef prices in Australia are now 11pc higher than a year ago. At the same time, manufacturing costs into the food sector have risen by nearly 7pc.

These increases reflect the broader inflationary pressures still flowing through the economy. Labour, freight, energy and compliance costs all remain elevated relative to historical norms. Even where monthly increases appear modest, the cumulative effect continues to pressure operating margins.

The slight improvement in the BPTC through Q1 suggests processors have regained some footing after a particularly difficult finish to 2025. The rise from 13pc in January to 19pc in March indicates conditions stabilised somewhat as the quarter progressed. Part of this improvement likely reflects a gradual increase in cattle availability.

Through March, slaughter activity lifted strongly in several key states, particularly New South Wales and Queensland. This allowed processors to improve plant utilisation and spread fixed costs more effectively. However, the recovery remains fragile. The index levels themselves tell the story clearly. A reading of 16pc remains well below what would historically be considered strong processor conditions.

The broader market environment has also become increasingly volatile. Cattle prices have softened sharply in recent weeks, particularly in cow and younger cattle categories, suggesting supply has started to improve more meaningfully. At the same time, export market uncertainty and logistical disruptions continue to influence processor behaviour.

This creates a difficult balancing act. Improving cattle supply should theoretically support processor margins through lower procurement costs. However, any weakening in export demand or increase in operating costs can quickly offset those gains.

The market has normalised considerably, with processors now operating in conditions that are far more sensitive to incremental changes in either supply or demand. The rise in export values over the past year should not be dismissed. An 11pc increase across the top four export markets is still a meaningful improvement and reflects generally supportive global beef demand.

China has strengthened materially, with export values up 19pc year on year. But the livestock procurement side of the equation has simply moved faster. When cattle prices rise by close to 30pc while export values rise by 11pc, margin compression becomes almost inevitable.

The first quarter of 2026 therefore reflects a processing sector still under pressure, but beginning to stabilise.