Iran Conflict Creates Opportunity and Risk for Australian Grain

The Snapshot

The Detail

The escalation of military action involving Iran, Israel and the United States has pushed geopolitics back to the centre of commodity markets, with crude oil prices moving sharply higher, as the conflict escalates, and this could have a major impact on the Australian grain sector.

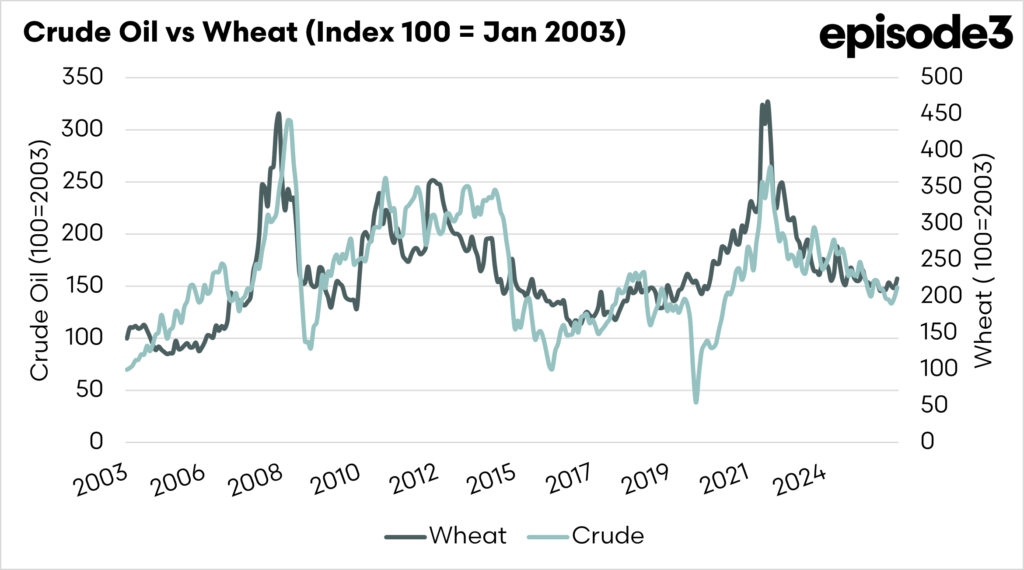

The conflict has already escalated to neighbouring states, and Iran has closed the Strait of Hormuz, through which 20% of the world’s oil transits. Oil prices have risen dramatically, with over-the-counter markets up 8 to 10% over the weekend, and the oil price has a significant impact on grain markets. Energy markets and agriculture are closely linked due to their connections to inputs and biofuels.

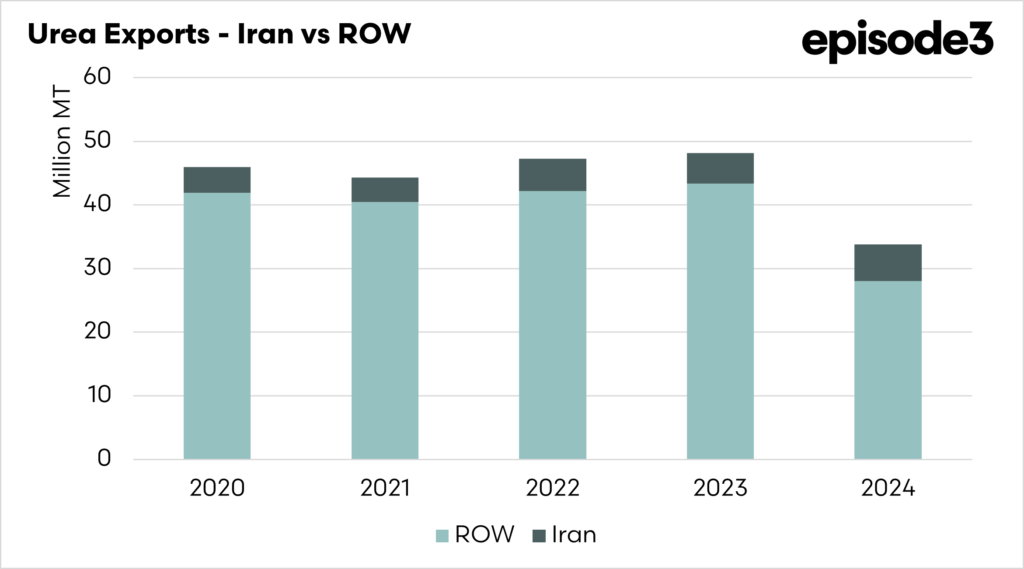

Nitrogen production is closely tied to energy pricing, and instability involving Iran adds an additional layer of uncertainty given the country’s role in global urea supply. Any interruption to exports, shipping access or financial flows has the potential to tighten availability at a time when many Northern Hemisphere producers are approaching planting decisions. Even without outright supply loss, risk alone can lift pricing as buyers move to secure tonnes earlier than planned.

Grain markets are linked to crude oil through biofuels because crops such as corn, wheat, sugar and oilseeds are used to produce ethanol and biodiesel, which compete directly with petroleum fuels in the energy mix. When crude oil prices rise, biofuels become more economically attractive, improving blending margins for refiners and encouraging greater production. This increases demand for feedstock grains and vegetable oils, tightening the supply available for food and feed markets and often supporting prices.

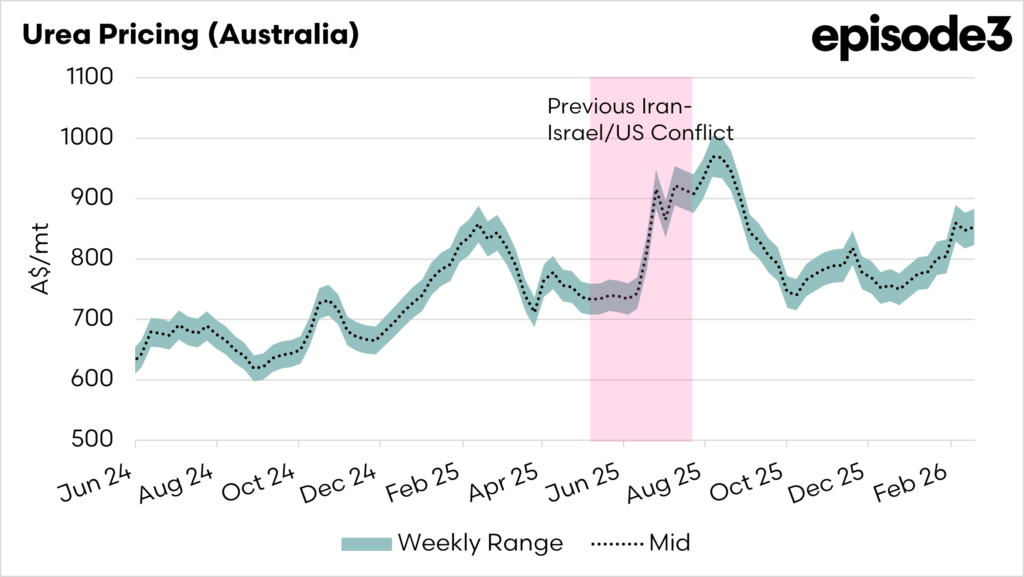

We can look back to June 2025, when Israel and the USA launched limited attacks on Iranian infrastructure, which resulted in fertiliser and grain prices rising significantly, as risk premiums emerged in the market. At this time, urea prices rose over A$150 per tonne. This was a short conflict, and grain prices returned relatively quickly to pre-conflict levels.

This particular conflict was short, but this current event has already escalated to neighbouring countries and will be more sustained, with President Trump calling for a four-week conflict.

At the moment, we expect markets to react strongly to this event, which will be beneficial for grain prices but not for inputs. This can create a timing mismatch.

The majority of farmers in Australia have very little grain left in their hands from the previous harvest to benefit significantly from any current rally. However, they are likely to pay higher seeding prices, but a rally in grain prices may not be sustained through harvest. The risk is high input prices at seeding, but without the corresponding high prices at harvest.

In recent years, farmers have pulled back across the country from forward sales of grain. This current market may be an opportune time to reconsider strategies to include a higher level of forward sales if the market provides attractive pricing.

The key to this entire situation is the duration. If this is a short spike, it will be a volatile spike in markets. If this is a prolonged conflict, we will see structural repricing, which, in the worst case, could significantly impact global planting inventories.