Grain markets caught between drought and diplomacy

The Snapshot

- US winter wheat conditions have deteriorated again, keeping global wheat markets sensitive to further weather risk.

- Grain markets remain heavily influenced by energy, freight and fertiliser volatility linked to the Middle East conflict.

- Faster US corn and soybean planting has capped some upside despite worsening wheat conditions.

- Kazakhstan’s sharply lower crop outlook highlights that production concerns are extending beyond the US Plains.

- Australian grain prices remain firm in northern markets, but elevated input and freight costs continue to pressure margins.

The Detail

Wheat markets are still caught between two competing forces. On one side sit deteriorating crop conditions and growing concern about global production risk. On the other hand, improving planting progress, softer oil prices and still relatively comfortable global stock levels. The result is a market that continues to trade nervously, with volatility staying high across wheat, oilseeds and energy.

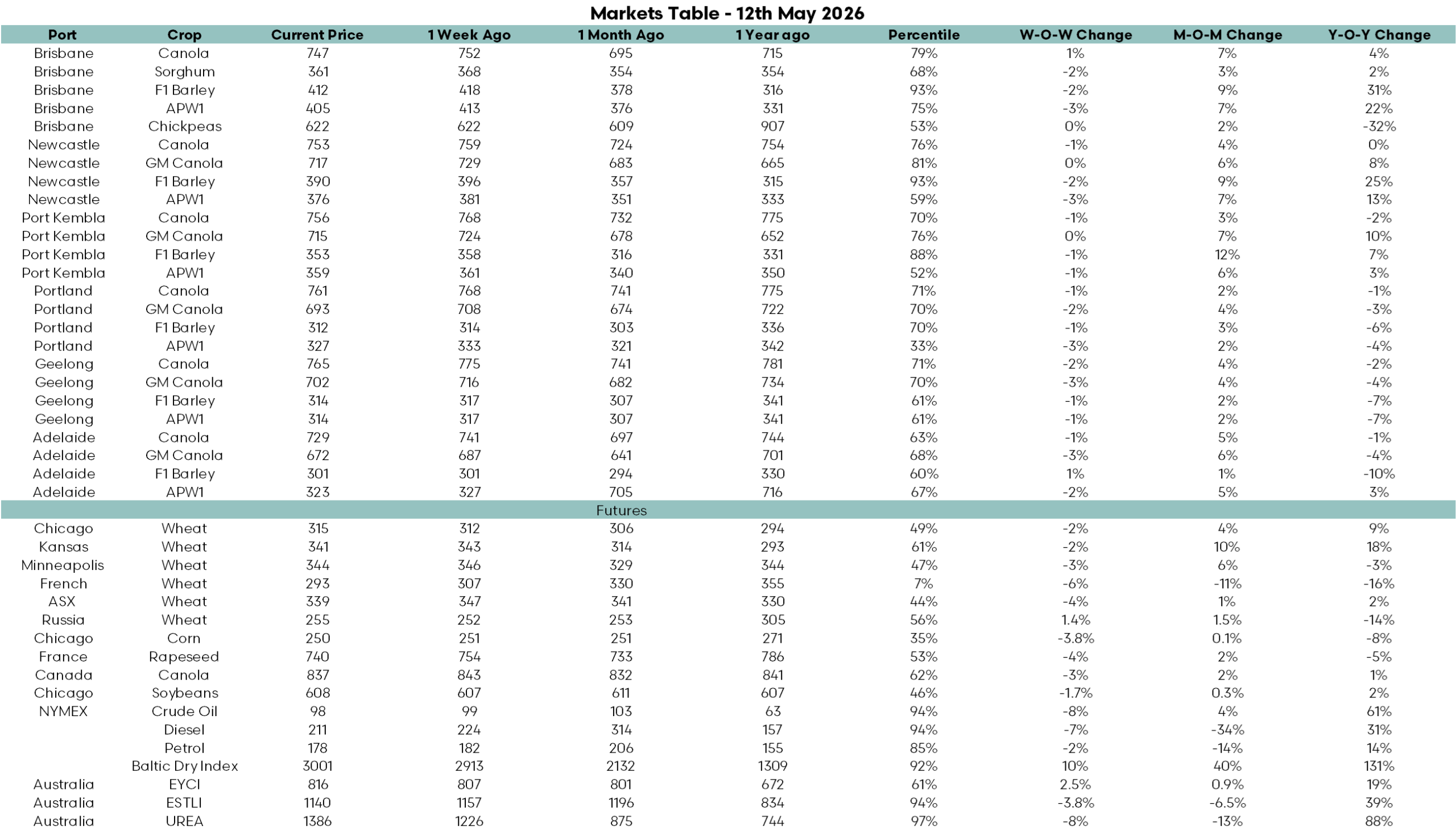

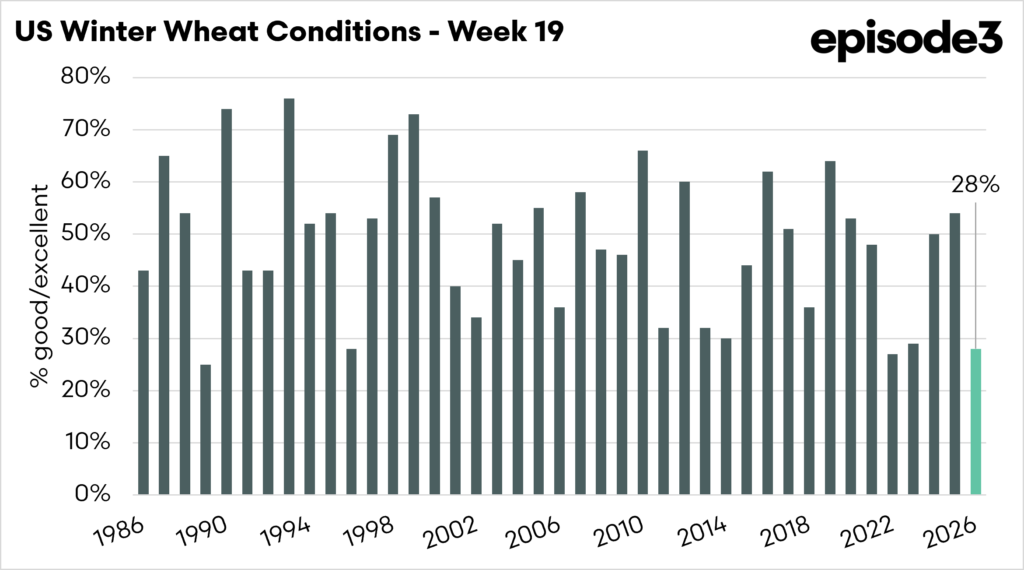

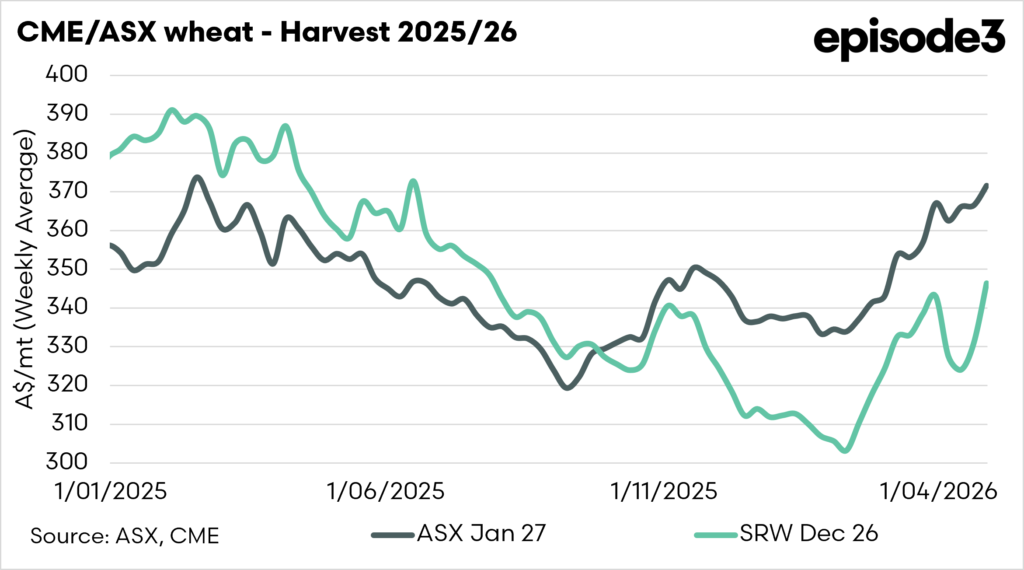

The biggest driver continues to be the condition of the US winter wheat crop. The latest USDA figures showed the national good-to-excellent rating falling to 28pc, down from 31pc the previous week and well below trade expectations. Importantly, this is now the weakest rating for this time of year since 2022. Kansas, the largest winter wheat-producing state in the US, saw conditions deteriorate further, while drought pressure stays widespread across the Plains. Around 70pc of the US winter wheat crop is currently sitting in drought-affected regions, up sharply from 22pc this time last year.

Rainfall across parts of the US and Europe helped stabilise sentiment temporarily during the week, but the market remains concerned that much of the moisture arrived too late or in insufficient volume to fully repair crop damage. Once the market begins pricing in yield loss, that premium tends to remain until harvest provides clearer evidence around production outcomes.

Production concerns are also spreading beyond the US. Kazakhstan is now forecast to see wheat production fall sharply in 2026-27 due to expected planting delays and a hotter, drier growing season. Wheat output is projected to drop from around 18Mt to 14Mt, with exports also expected to decline significantly. While Kazakhstan is not one of the world’s largest exporters, the reduction reinforces the broader theme that weather risk remains elevated across multiple production regions.

Governments are also increasingly focused on food security. Egypt has accelerated domestic wheat procurement this season and continues to push toward greater wheat self-sufficiency as it seeks to reduce exposure to global import volatility. Moves like this highlight how governments remain highly sensitive to food inflation and supply chain disruptions following several years of elevated commodity market volatility.

Oilseed markets were somewhat softer during the week. Falling crude oil values pressured vegetable oils and rapeseed futures, while expectations for record global soybean stocks in the upcoming USDA WASDE report also weighed on sentiment. Even so, the outlook remains mixed. Canadian canola seeding has been running behind schedule, while Western Australia is expected to plant a record canola area this season as growers continue shifting toward crops offering relatively stronger returns.

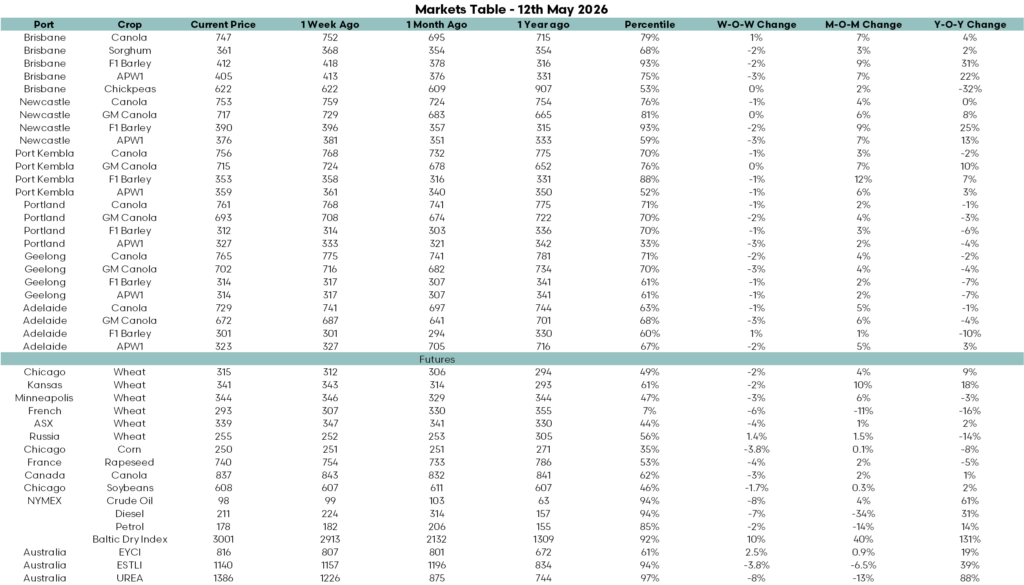

The local Australian market continues to reflect many of these global themes. Northern feed grain and wheat markets are still the standout performers. Brisbane F1 barley is sitting at $412/t, up 31pc year on year and in the 93rd percentile, while Newcastle F1 barley is also sitting in the 93rd percentile at $390/t. Brisbane APW1 is up 22pc year on year to $405/t, while Newcastle APW1 has lifted 13pc over the same period. Southern markets remain softer by comparison, with Victorian and South Australian barley and wheat values generally lower year-on-year despite modest monthly gains. Canola markets remain relatively firm nationally, although gains have been steadier than in feed grains and wheat.

The broader cost structure remains one of the most important themes for growers. Even after recent weekly declines, crude oil is 61pc above year-ago levels and still sits in the 94th percentile historically. The Baltic Dry Index is up 131pc year on year, highlighting the continued freight pressure sitting across global supply chains. Urea has eased from recent peaks but remains 88pc above last year and in the 97th percentile. Diesel prices have fallen sharply over the past month but are still 31pc above year-ago levels.