High Input Costs Don’t Guarantee High Grain Prices

Quicker Updates

For quicker updates as markets move, follow @thewheatwatcher on Instagram. I regularly post short summaries and charts breaking down what’s happening in grain, fertiliser and broader ag markets so you can stay across the key moves without having to read through pages of analysis. If markets are moving quickly, that’s usually where the updates will land first.

The Snapshot

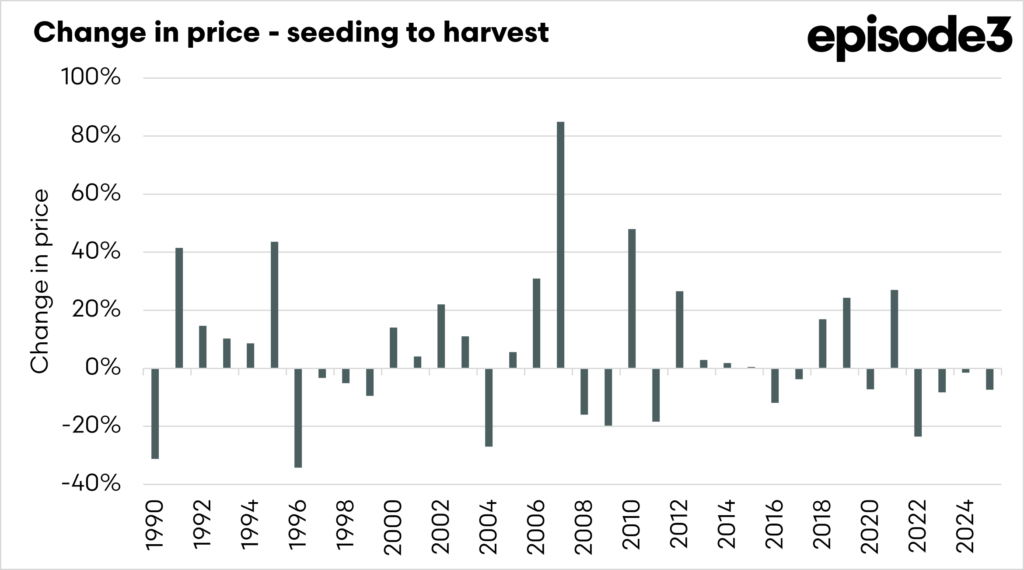

- • Since 1990, wheat prices have moved around $42/t on average between seeding and harvest, showing how much markets can shift during the season.

- • Harvest prices were higher than seeding in 20 seasons and lower in 16, making the direction of the move close to a coin toss.

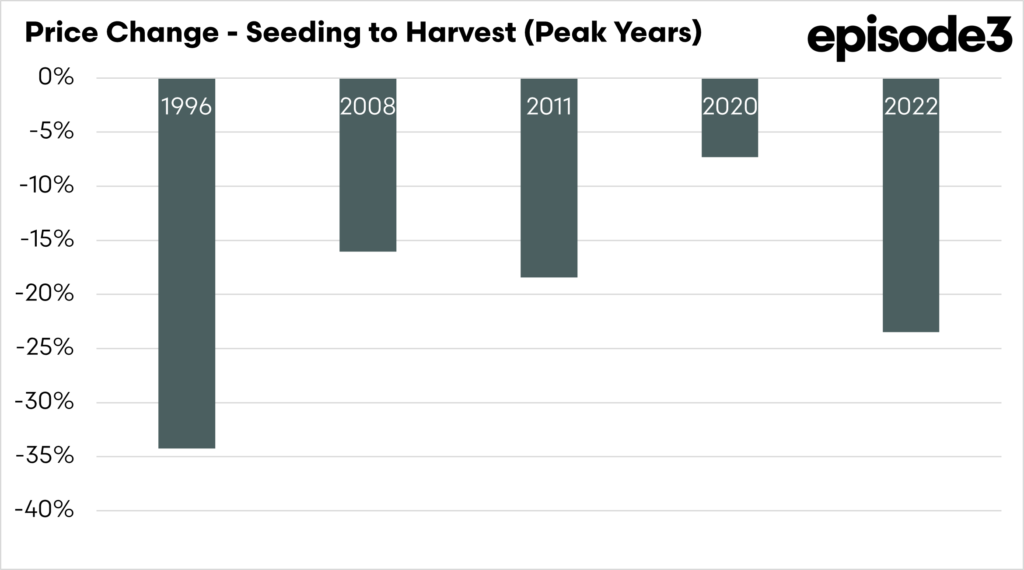

- • In years where wheat prices were unusually high at seeding, harvest prices were lower every time, falling by about $70/t on average.

- • Farmers often lock in most input costs at seeding, yet grain prices can move dramatically over the following eight months.

- • Strong prices at planting do not guarantee strong prices at harvest, meaning the margin risk largely sits with the grower.

One of the persistent assumptions in cropping is that the wheat price available at seeding provides a reasonable guide to the price farmers might receive at harvest. However, a long-term look at wheat futures suggests that this relationship is far weaker than many growers might expect.

Using CBOT wheat futures converted into Australian dollars per tonne and comparing the average price during April (seeding) with the average price during December (harvest), the data since 1990 show that price movements through the growing season are highly variable. CBOT Wheat is used because it has a reliable long dataset, and overseas pricing drives most of our market in Australia. While prices at seeding and harvest often sit within similar historical ranges, the direction and size of the move between those two points can change dramatically.

Across the 36 seasons in the dataset, the average seeding price is around $232 per tonne, and the average harvest price is about $238 per tonne. This suggests there is little difference between the two periods. However, the key statistic is the typical size of the movement between them. On average, wheat prices move by roughly $42 per tonne between seeding and harvest, either higher or lower depending on how global supply and demand conditions evolve during the season.

The direction of those moves is also far from predictable. In 20 of the 36 seasons examined, harvest prices were higher than seeding prices. In the other 16 years, harvest prices were lower. While the market rises slightly more often than it falls, the difference is small enough to provide little predictive value when growers make planting decisions months earlier.

An even more revealing pattern appears when examining years in which prices were unusually high at seeding relative to surrounding seasons. These spike years are periods when the market is already under stress due to supply concerns, geopolitical events, or strong global demand.

The key examples in the dataset occur in 1996, 2008, 2011, 2020 and 2022. In each of these seasons, wheat prices at seeding were significantly higher than in nearby years. Yet in every case, the price by harvest was lower. On average, these spike seasons saw wheat values fall by around $70 per tonne between seeding and harvest.

This pattern reflects the way global grain markets tend to behave. When prices surge early in the season, it often reflects an existing supply shock or uncertainty about production. As the growing season progresses and more information becomes available about crop conditions around the world, some of that risk premium can unwind, pulling prices lower again.

This historical behaviour is particularly relevant in seasons when input costs rise sharply around the seeding window. Fertiliser, fuel and chemical costs often increase alongside global energy or geopolitical shocks, pushing up production costs at the same time that grain prices are already elevated.

For farmers, this creates a difficult margin risk. Growers may commit to higher production costs based on strong prices at planting, but the historical record shows that these prices frequently shift during the growing season and sometimes fall significantly by harvest.

To summarise, higher prices at seeding do not guarantee higher prices when the crop is sold. The data make it clear that while grain markets can move in either direction during the season, the financial risk of that uncertainty largely sits with the grower.

Farmers commit to most of their production costs within a few weeks of seeding, yet the crop price can move dramatically over the following eight months. History shows that even when prices look strong at planting, there is no guarantee they will remain there by harvest. This will also likely be exacerbated if the conflict is over quickly, and the risk uncertainty diminishes.

The reality is that there is no way for a farmer to prepare for a year like this, but make sure that you sit down with your advisors and think strategically and logically.