Global Noise, Local Reality in Grain Markets

Weekly Summary

Global grain markets are starting to stir, with tightening supply risks, shifting policy signals, and geopolitical tensions all beginning to shape the direction.

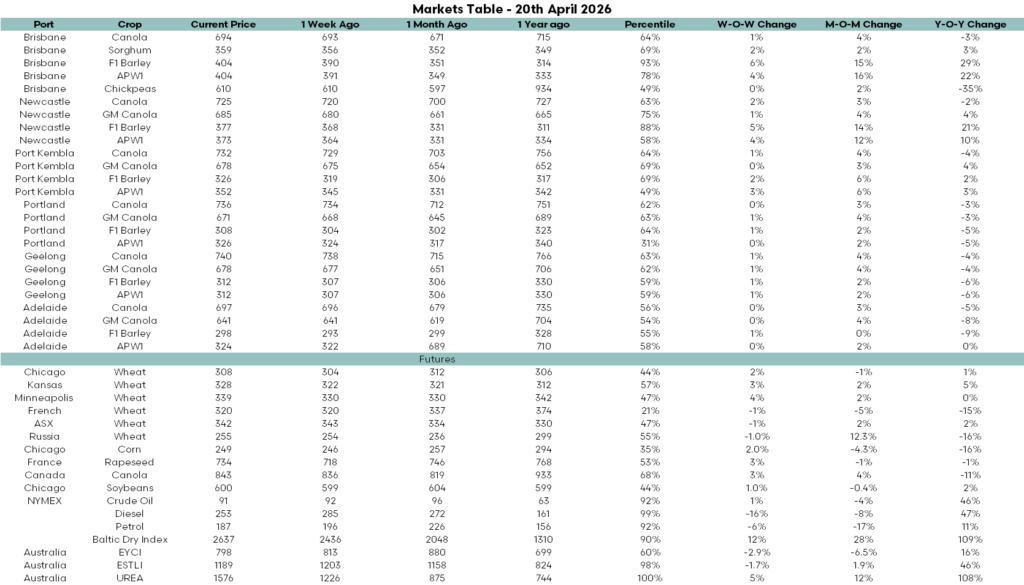

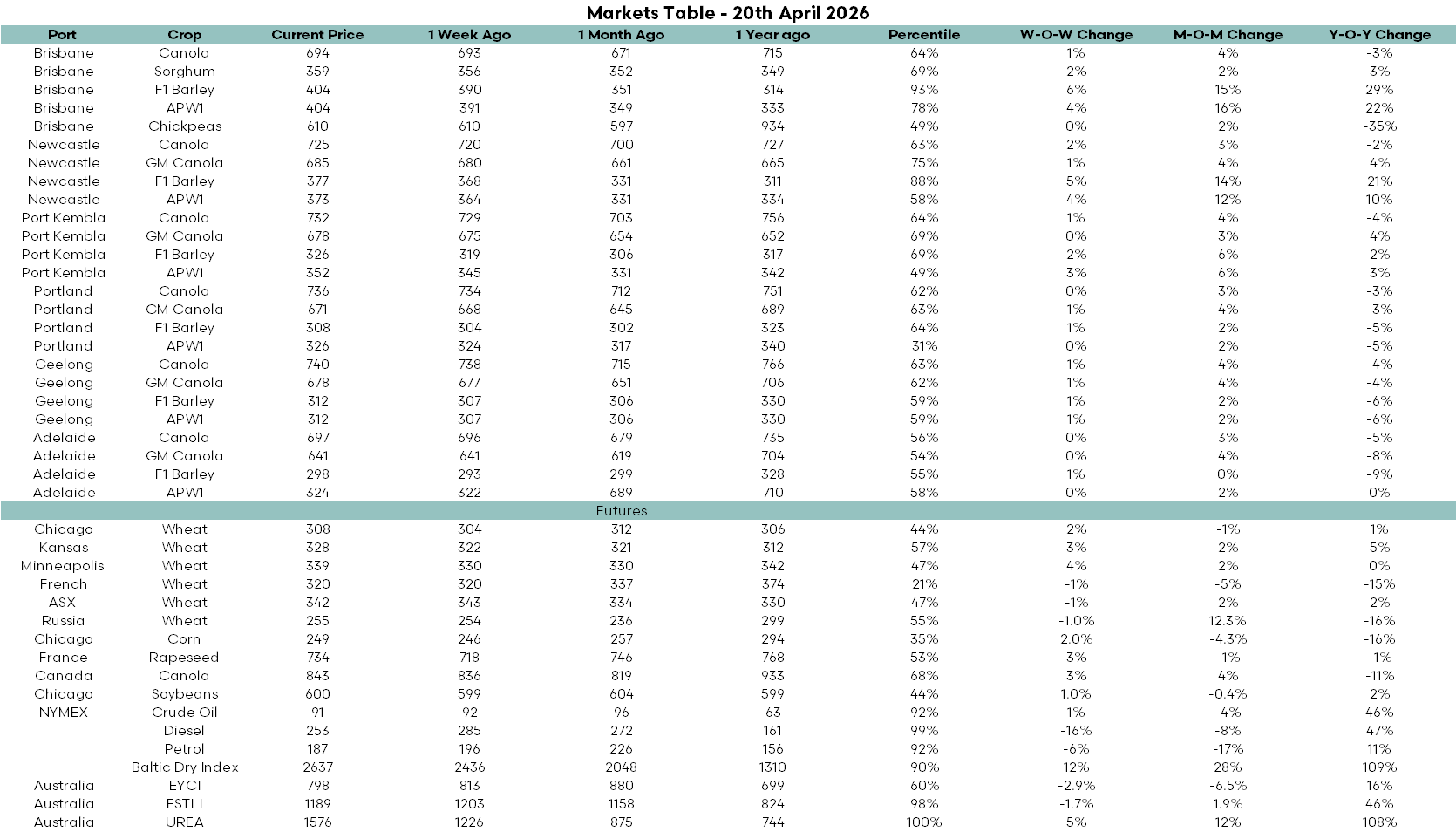

The US wheat crop continues to deteriorate. Just 30pc of winter wheat is rated good to excellent, the weakest level for this time of year since the last major drought cycle, and around 68pc of the crop is now sitting in drought-affected areas. That is starting to underpin wheat values, with Chicago futures lifting slightly week-on-week, although they remain below levels seen a month ago. The market is increasingly sensitive to changes in the weather outlook, particularly across the Plains, where moisture deficits are beginning to bite.

Planting progress in the US is moving at a solid pace. Corn and soybean planting are both tracking ahead of the five-year average, limiting upside in broader grain markets. Early planting momentum, particularly in southern states, is reinforcing expectations of a large northern hemisphere crop if seasonal conditions normalise. For now, the trade is balancing poor wheat conditions against the potential for strong corn and soybean production, keeping price moves in check.

Geopolitical tension remains part of the backdrop. Developments involving the US and Iran have added uncertainty, particularly in energy markets. While crude oil has pulled back 10pc week-on-week, it remains 39pc higher year-on-year, highlighting the volatility still lurking beneath the surface. That volatility is feeding into broader commodity sentiment, even if the direct impact on grain demand remains limited at this stage.

India has also re-entered the market with an increased wheat export quota of 5 million tonnes. In theory, this adds supply to the global balance sheet, but there is scepticism around execution. Traders are already struggling to move the initial allocation, suggesting that logistical or pricing constraints may limit actual exports. As a result, the announcement has had little immediate impact on global wheat pricing.

Broader commodity signals remain mixed. The Baltic Dry Index has surged 17pc week-on-week and is now more than double year-ago levels, reinforcing the elevated cost of moving grain globally. Fertiliser markets remain tight, with urea lifting 5pc week-on-week and 12pc month-on-month, now more than double year-ago levels and at the top of its historical range. That continues to shape forward cost structures, even if it has not yet translated into reduced global output.

Back home, the key story is not futures, it is basis.

The strongest price moves are concentrated in Queensland and northern New South Wales. Brisbane barley has lifted 6pc week on week and 15pc over the past month, while APW1 has climbed 5pc week on week and 15pc month on month. Newcastle is showing a similar trend, with wheat and barley both rising by around 5pc week-on-week. These markets are now sitting in higher percentile ranges, reflecting tightening supply and increased buyer urgency.

Feedgrain markets are showing strength, with sorghum also edging higher. The lift is not extreme, but it reinforces the tightening balance in the north as buyers look to secure coverage amid declining confidence in supply.

Southern markets remain comparatively steady. Victoria and South Australia are generally seeing gains of 0–2pc week-on-week, with several markets still below year-ago levels. Canola values across the south remain under pressure compared to last season, while barley and wheat have only seen modest improvements. The divergence between north and south is becoming more pronounced, with regional dynamics driving pricing outcomes.

Dryness in the north is starting to drive pricing, and the market is beginning to factor in seasonal risk earlier than usual. With an El Niño forecast building, attention is shifting toward the upcoming crop and the potential for lower production across eastern Australia.

If those conditions persist, further gains are more likely to come through basis rather than global futures. Northern premiums are already building, and that trend is likely to continue as local supply tightens and buyers compete for grain. For Australian growers, the signal is clear. Global markets provide the backdrop, but local conditions are increasingly setting the price.