El Niño Doesn’t Break the Global Wheat Market

The Snapshot

- El Niño does not cause a global wheat shortage, it shifts production between regions

- Major producers like the US, EU, China and India remain relatively stable

- Volatile regions can swing both up and down, often offsetting each other

- Global wheat prices do not reliably rise during El Niño years

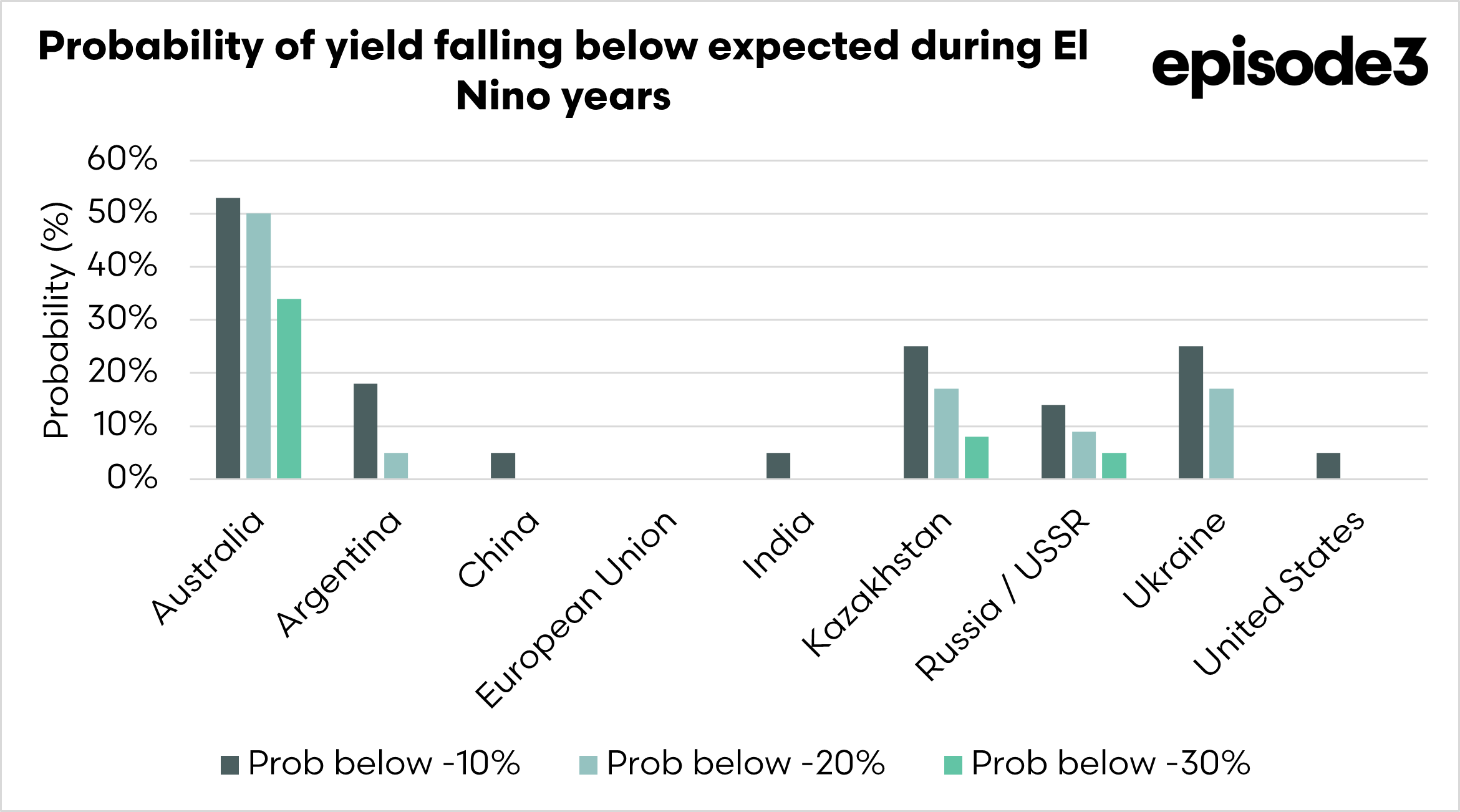

- Australia faces the highest downside risk, with a 50 pc chance of yields falling more than 20 pc

- Farmers carry the production risk locally, without a guaranteed lift in price

- The real threat is margin compression, not just lower yields

The Detail

El Niño is often talked about as a global production risk, but the data tell a different story. When you look at wheat yields across the major producing countries since 1960, there is no sign of a global collapse. Instead, El Niño shifts production around. Some regions have poor seasons, others have good ones, and overall, the system tends to balance out.

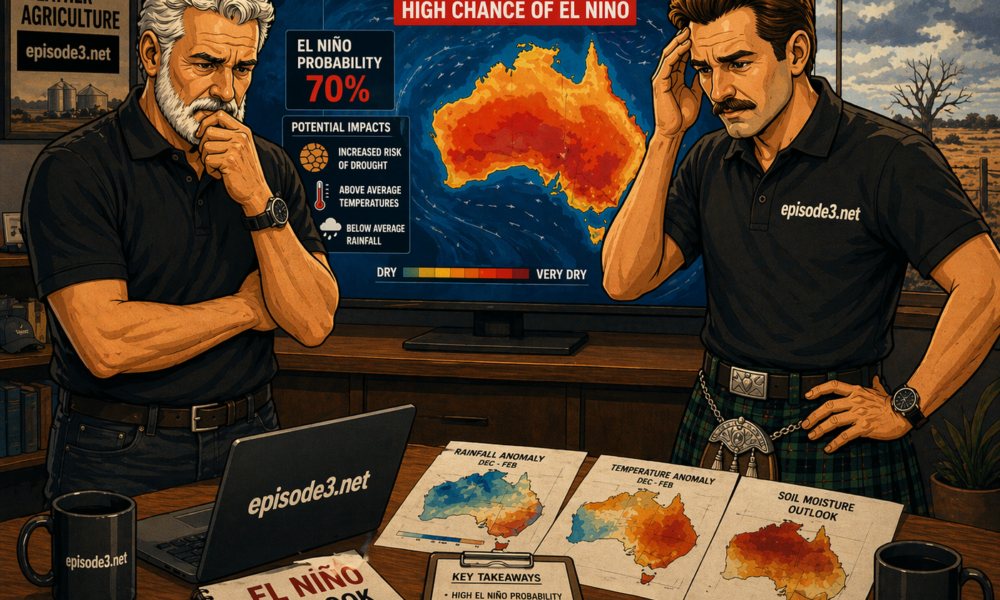

In the United States, yields are basically a coin toss in El Niño years. About half the time they are above normal, half the time below, and big losses are rare. Europe shows a similar pattern, with slightly more downside than upside, but the swings are small. China and India are even more stable. In both countries, yields tend to hold up, and large shortfalls are almost unheard of.

Where things get more interesting is in the more weather-exposed regions. Argentina, Kazakhstan and Ukraine can swing both ways. Argentina often benefits from El Niño conditions, with yields above normal in most years, but it still has a meaningful chance of a poor season. Kazakhstan and Ukraine are more volatile again. They can have big upside years, but also carry real downside risk when conditions turn. The key point is that even in these regions, bad years are often offset by good ones elsewhere.

That is what keeps the global system steady. When one region has a poor crop, another tends to pick up the slack. There is no consistent pattern of multiple major producers all having bad seasons at the same time.

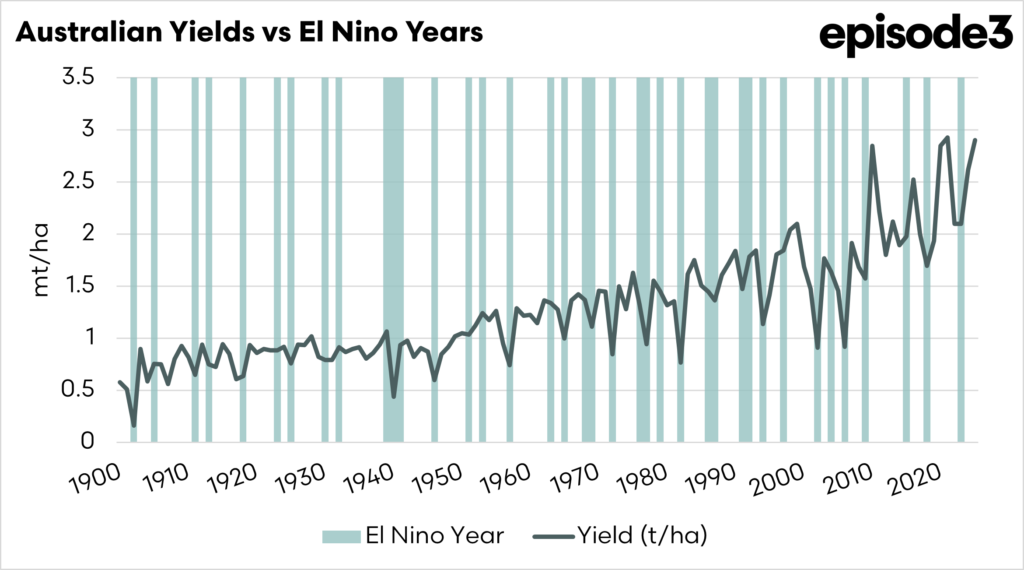

For Australian farmers, the story is very different. Australia sits at the extreme end of the downside risk. On average, yields in El Niño years are about 15 pc below normal. More importantly, there is a 50 pc chance of being more than 20 pc below expectations, and a 34 pc chance of being more than 30 pc below expectations. No other major exporter in this dataset comes close to that level of risk.

The problem is that this production risk is not matched by price. Australia is a major exporter, but only a small share of global production. When Australian crops fall short, the US, Europe or the Black Sea can often make up the difference. That keeps global supply relatively steady and limits any price response.

This creates a tough position. You can have a season where your yield is down 20 pc or more, but the market barely moves. The usual expectation that a poor crop leads to higher prices does not reliably hold in an El Niño year. Instead, you are carrying the downside while the global system absorbs the shock.

That is the real risk. El Niño is not a global shortage event, it is a regional one. The global wheat market is resilient, but that resilience comes at a cost. For Australian farmers, it means wearing a disproportionate share of the downside, without a guaranteed lift in price to offset it.