Grain Market Weekly: All eyes on Tehran – but there are more factors at play.

The Snapshot

• The escalating conflict involving Iran has become the dominant short-term driver of global grain markets.

• Grain markets moved higher as crude oil surged nearly 30%, highlighting the strong link between energy and agricultural markets. They also followed energy markets when they collapsed.

• Short covering by speculative funds amplified the rally as traders were forced to buy back positions during the price rise.

• Global planting decisions and weather issues, including delayed sowing and frost damage in Ukraine, are adding further uncertainty to grain supply.

Last week, I talked about how all eyes were on the skies in Australia. This week, all eyes are on the skies above Iran. The conflict in the Middle East has been the biggest driver of the market, but there are some other topics to unpack.

Global grain markets have begun to respond to a rapidly changing mix of geopolitics, energy prices and planting decisions across several major producing regions. While the past few weeks have delivered plenty of uncertainty, they have also produced some notable shifts in pricing and production expectations.

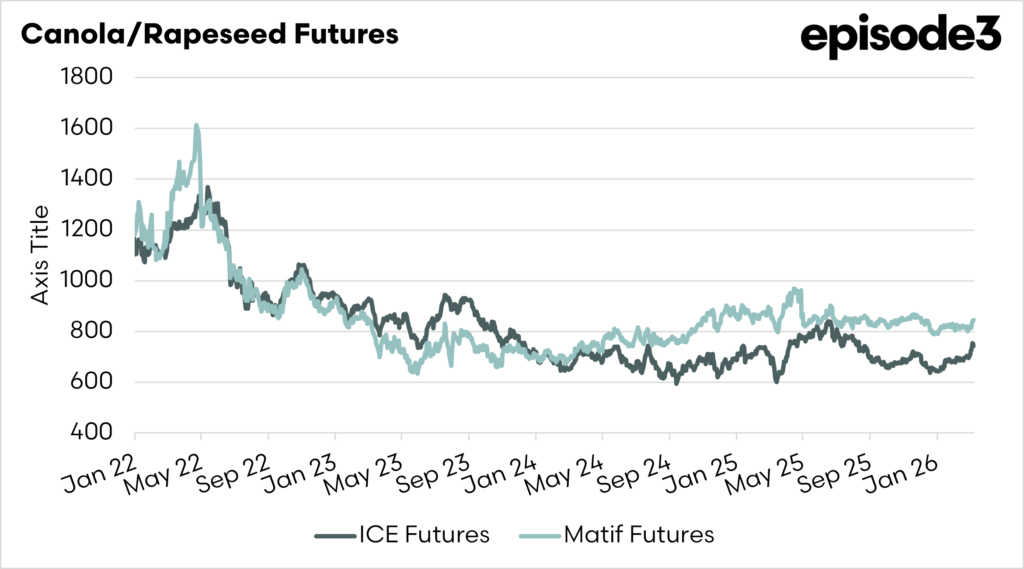

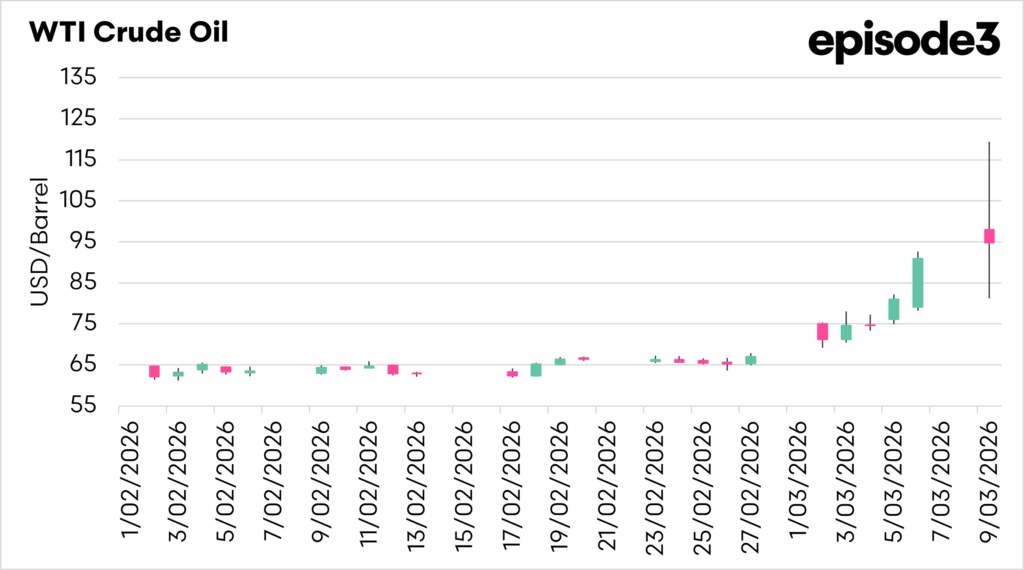

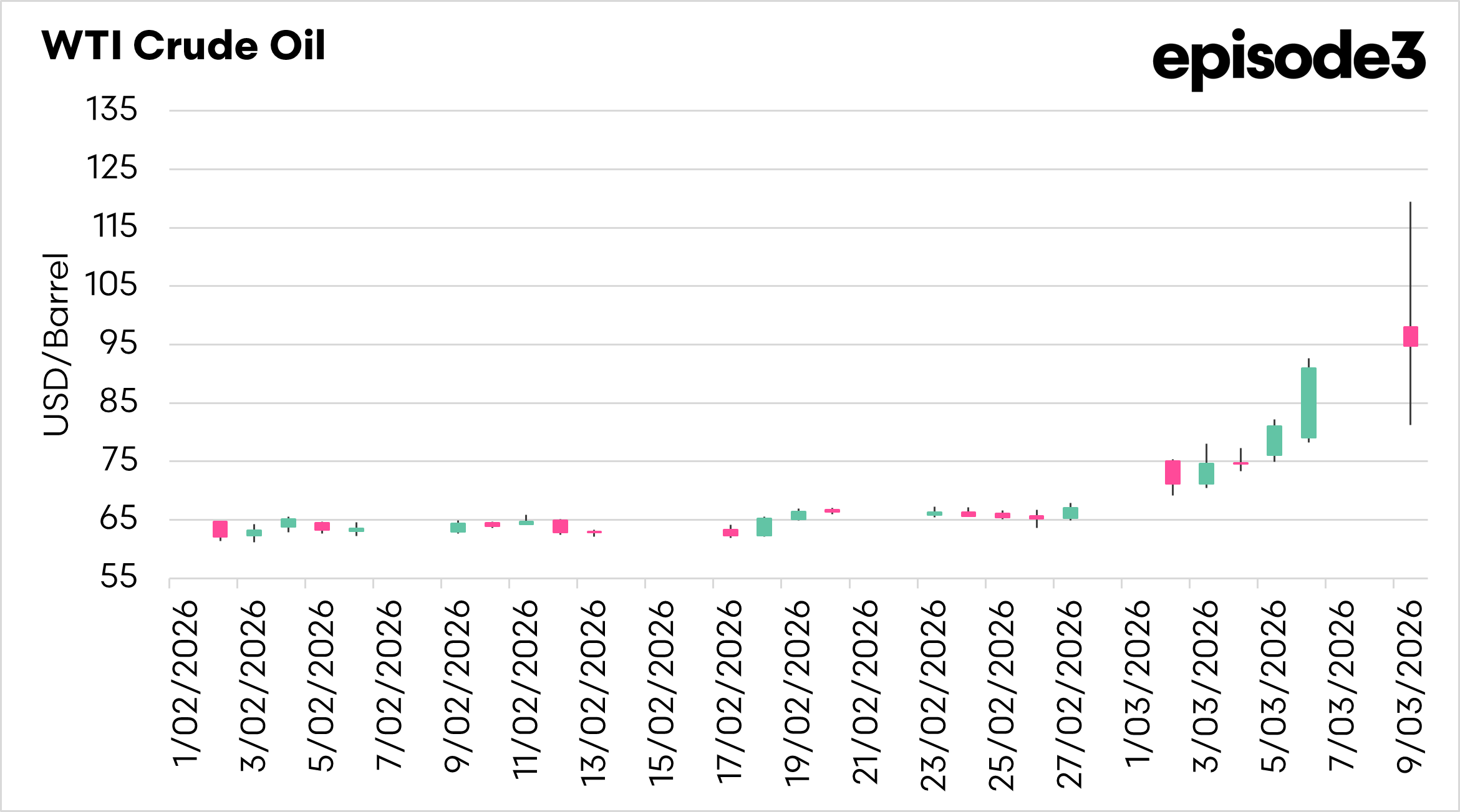

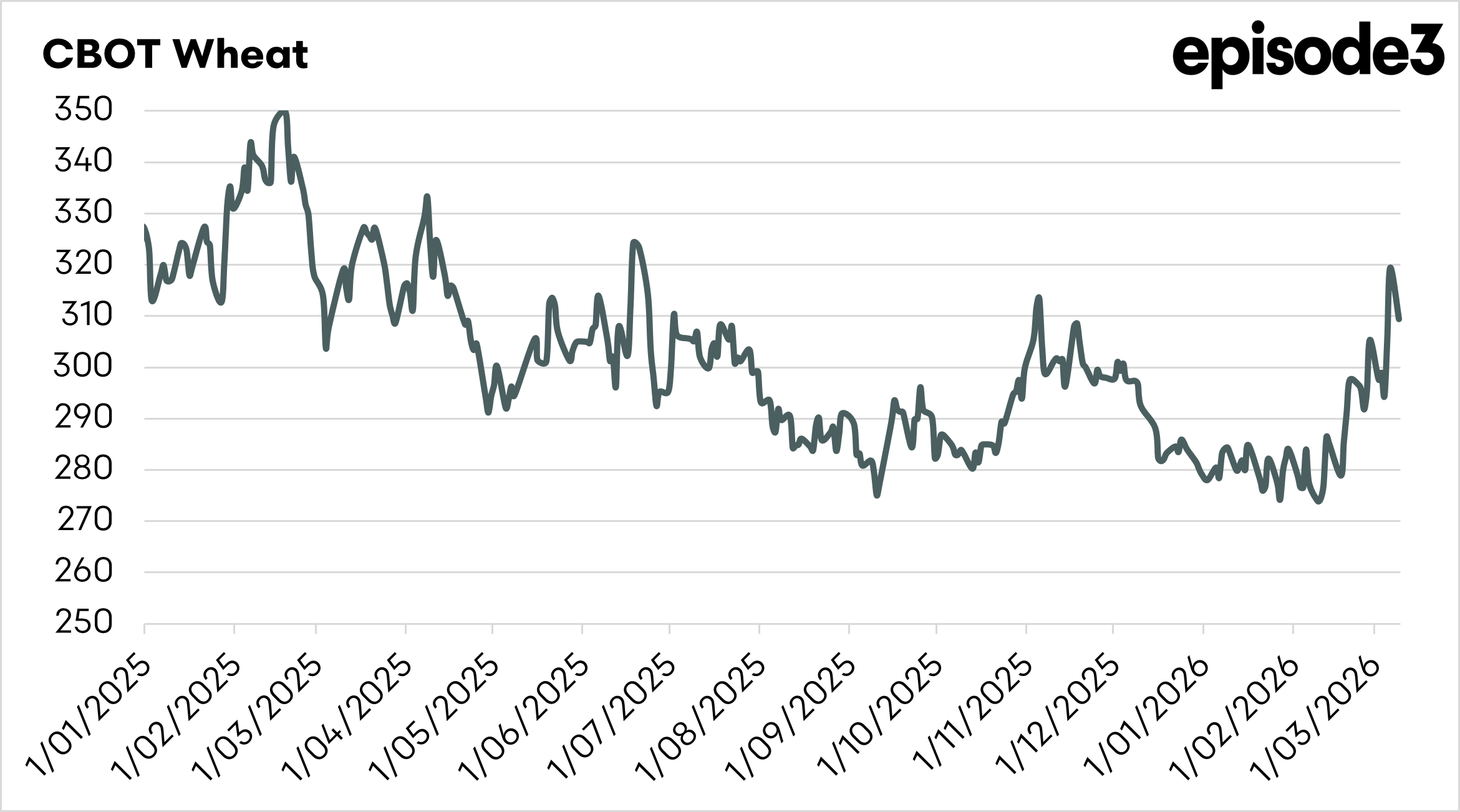

Wheat markets have recently found support amid surging crude oil prices amid the escalating conflict involving Iran. Initially, grain markets were slow to react. Unlike the Russia–Ukraine war, which directly involved two major wheat exporters, Iran itself is not a significant player in global wheat supply. As a result, the early stages of the conflict did not immediately threaten global grain availability, and prices remained relatively stable.

However, sentiment changed as energy markets began to rally sharply. Brent crude futures briefly surged nearly 30 per cent, reaching around US$119 per barrel before easing back below the US$100 mark as concerns about global economic growth re-emerged. The spike in oil prices was driven by fears that instability in the Middle East could disrupt energy production, as Israel attacked multiple oil storage facilities.

Grain markets followed energy prices higher, before retreating as oil prices fell. The relationship between oil and grain is well established. Energy influences agricultural markets through multiple channels, including the cost of diesel, fertiliser, freight and processing. Higher crude prices also increase the value of biofuels, which in turn lifts demand for grain and oilseeds used in renewable fuel production.

Another factor amplifying the rally was the behaviour of speculative traders. Large funds had been holding significant short positions in wheat futures, effectively betting on falling prices. As geopolitical risk pushed commodity markets higher, many of these traders were forced to buy back their positions to close out those shorts. This process, known as short covering, can accelerate price movements and create sharp bursts of buying in futures markets.

While global grain supplies remain relatively comfortable for now, production decisions for the 2026 season could shift as farmers respond to rising input costs and uncertain market conditions.

In Canada, early planting intentions show modest changes in crop mix. Farmers expect to seed around 26.7 million acres of wheat, slightly lower than last year but still well above the five-year average. The canola area is expected to rise to roughly 21.8 million acres as expanding domestic processing capacity and stronger vegetable oil markets support demand. Barley acreage is also expected to increase, while lentils, peas and oats are forecast to decline due to large existing stocks and weaker returns.

Some analysts believe actual canola plantings could rise even further. Futures prices for 2026 canola have jumped more than A$100 per tonne since December, improving profitability for growers. However, my view is that growers may now temper that view of increased canola planting due to the cost of inputs.

Weather is also beginning to shape global production prospects. In Ukraine, spring planting is expected to start about two weeks later than usual due to frozen soils and lingering snow cover. Severe frosts in February damaged some winter crops, with losses estimated at up to five per cent nationally and significantly higher in parts of central Ukraine.

Areas lost to winterkill are typically replanted with corn or sunflowers, meaning final planting decisions will depend heavily on prices and market conditions in the weeks ahead.

Things change quickly in markets. Rising energy prices, shifting planting intentions and weather disruptions highlight how quickly global grain markets can move when geopolitics, input costs and seasonal conditions collide.