Australia’s Urea Supply Is Now a Race Against the Clock

The Snapshot

- Australia relies heavily on the Middle East for urea, with about 69% of imports sourced from the region, leaving fertiliser supply highly exposed to disruptions in the Gulf.

- The closure of the Strait of Hormuz has effectively halted a major export route, trapping fertiliser shipments and severely tightening global supply.

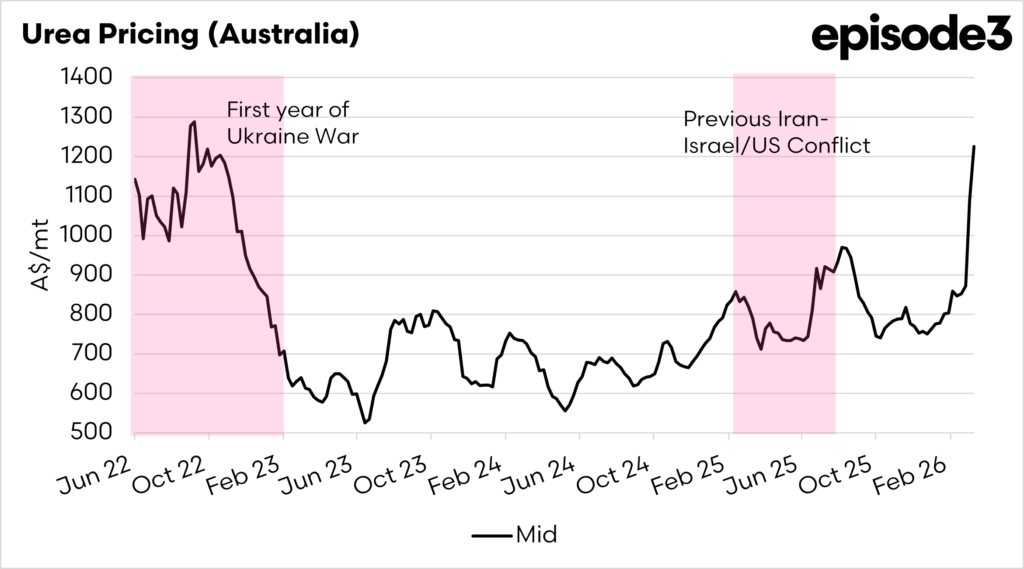

- Global urea prices have surged rapidly, with Australian model prices jumping from around A$872/t in late February to over A$1,200/t in mid-March.

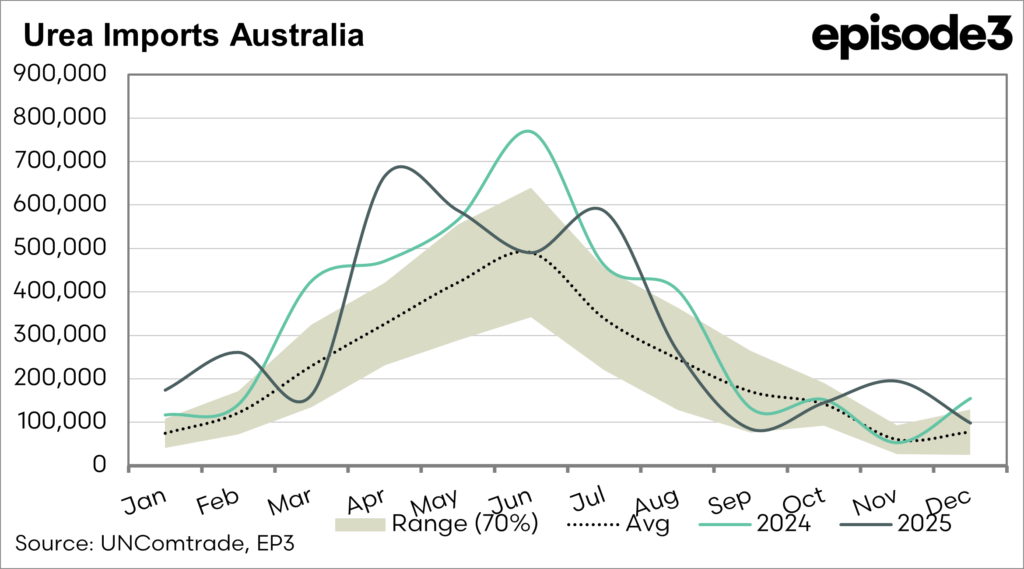

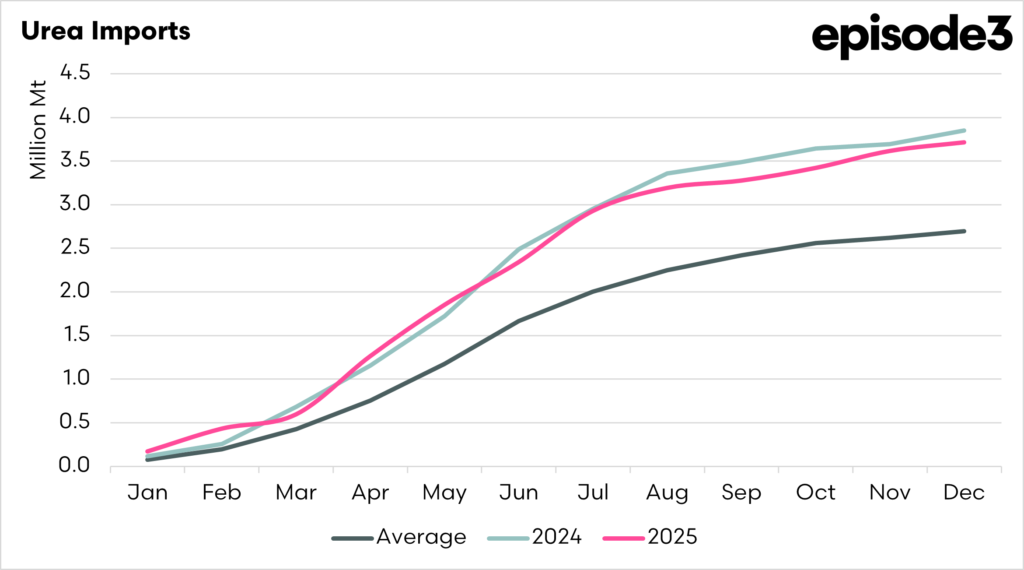

- The timing of imports is critical, as the majority of Australia’s fertiliser shipments normally arrive between April and June ahead of winter cropping demand.

- If Middle Eastern supply does not resume within the next four to six weeks, Australia risks both extremely high prices and potential fertiliser shortages during the winter cropping season.

The Detail

The global urea market has moved sharply higher in recent weeks as geopolitical tensions in the Middle East have disrupted both production and logistics across one of the world’s most important nitrogen exporting regions. The escalation of conflict involving Iran has had immediate consequences for fertiliser markets, given the region’s central role in supplying nitrogen products to global agriculture. Much of the world’s exportable urea originates from countries surrounding the Persian Gulf, and the disruption to shipping through the Strait of Hormuz has effectively halted a major artery of global fertiliser trade.

The immediate impact has been a rapid tightening of supply. A large volume of urea cargo has been stranded in the Gulf while shipowners and insurers reassess the risks of entering the region. At the same time, several production facilities across the Middle East have experienced operational disruptions, including outages at large export-oriented plants. Even in areas where production remains technically operational, the inability to move product out of the region has created a functional supply shortage in international markets.

This tightening has translated directly into price increases across key global benchmarks. Export prices from North Africa have surged, with Algerian and Egyptian products trading at levels not seen since the volatility of 2022. Southeast Asian producers have also lifted offers sharply, reflecting both stronger demand from importing nations and the lack of competing tonnes from the Gulf.

The Episode3 fair value model clearly shows how rapidly the market has responded. At the start of 2026, the mid price sat near A$775 per tonne. Through February, prices strengthened gradually, reaching around A$872/t by 26 February. However, once the conflict escalated and concerns over Gulf exports intensified, the market moved dramatically. The mid price jumped to roughly A$1,091/t in the week ending 5 March and then climbed again to about A$1,226/t by the end of last week. That represents an increase of more than A$350/t in just a few weeks.

Timing is now the critical issue for Australia. Our fertiliser import program typically accelerates from March onwards as importers position product ahead of winter cropping demand. Historically, only a small portion of the annual supply has arrived by the end of March, with the bulk of shipments occurring between April and June. That means the next four to six weeks are crucial for securing the tonnes required for the coming season. If the conflict doesn’t end, we may need to adjust our planting strategy to account for reduced availability.

If Middle Eastern supply does not resume within the next month, the implications for Australian agriculture will be severe. Shipping lead times from alternative origins quickly coincide with fertiliser application schedules, making it increasingly difficult to source replacement volumes. In simple terms, the system relies on those Gulf cargoes arriving on time. If they do not, the market will face not only extremely high prices but also the very real risk of physical shortages during the winter cropping season.