Grain Market Update – WC 23rd March 2026

Grain markets are sitting in a holding pattern, caught between rising risk and a lack of conviction to push higher. In Australia, the season has yet to properly begin, and that uncertainty is shaping both farm decisions and market behaviour. Rainfall across northern New South Wales and southern Queensland has been patchy, with storms delivering short-term relief but failing to rebuild subsoil moisture.

Further south, conditions are more favourable. Victoria and South Australia have seen useful falls, and parts of Western Australia are forecast to improve, leaving much of the southern cropping belt in a better position than this time last year. Even so, the national picture remains uneven, and the absence of a clear autumn break means growers are still holding back. Anzac Day is still the key decision point, but the window is tightening.

This uncertainty is already influencing rotations. In drier northern areas, canola is increasingly being replaced by cereals, reflecting both moisture constraints and rising input costs. Growers are also holding grain stocks as a hedge, particularly mixed farmers managing feed risk. The result is a physical market defined by limited liquidity and slow selling.

Cost pressure is reinforcing that caution. Fertiliser and diesel prices remain elevated, and volatility in energy markets is flowing directly into farmgate economics. For many growers, margin risk is now as important as seasonal risk, particularly for nitrogen intensive crops.

Globally, production risks are beginning to build, although this is not yet fully reflected in prices. Conditions across the US southern plains remain dry, raising concerns about wheat yields. The Black Sea region and parts of eastern Europe are also moisture-constrained, while in Europe, expectations for wheat and rapeseed production have started to edge lower.

Elsewhere, conditions are more stable, with China in reasonable shape and India improving after earlier heat concerns. The Northern Hemisphere crop is far from secure, even if markets have yet to fully price that risk. Despite these concerns, global grain markets continue to trade within relatively tight ranges.

Price moves have been reactive rather than directional, with rallies struggling to attract follow-through buying. There is a growing sense that while risks are increasing, the absence of a clear supply shock is limiting upside. At the same time, demand remains steady but not urgent, with little evidence of aggressive buying from importers, suggesting global supply chains are, for now, adequately covered.

Energy remains a key influence across markets. Elevated prices are feeding into fertiliser and fuel costs and shaping biofuel demand and oilseed markets. The link between energy and agriculture has tightened, but it is unclear whether energy needs to move higher again to drive grains more decisively.

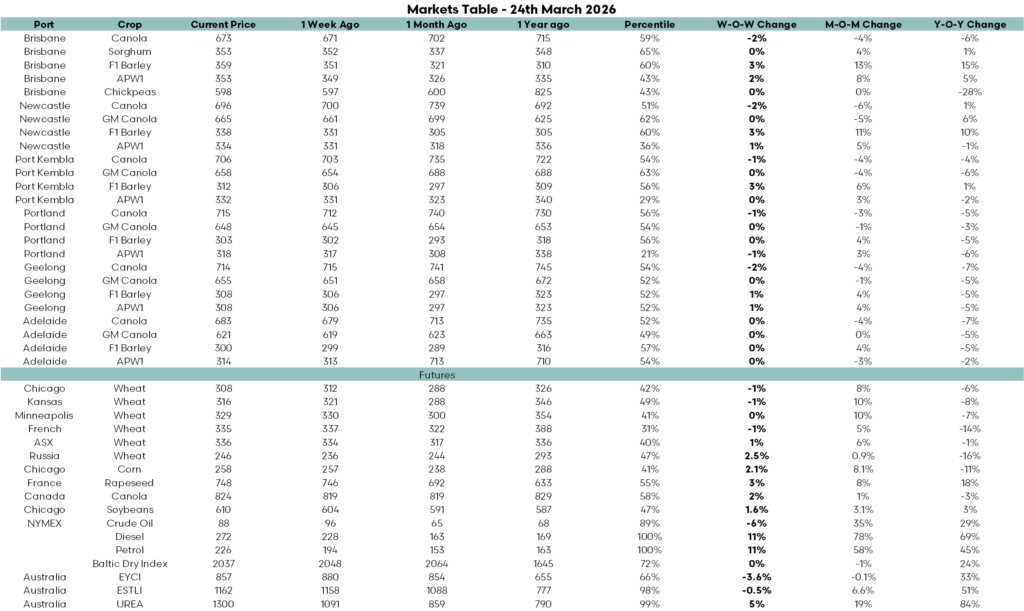

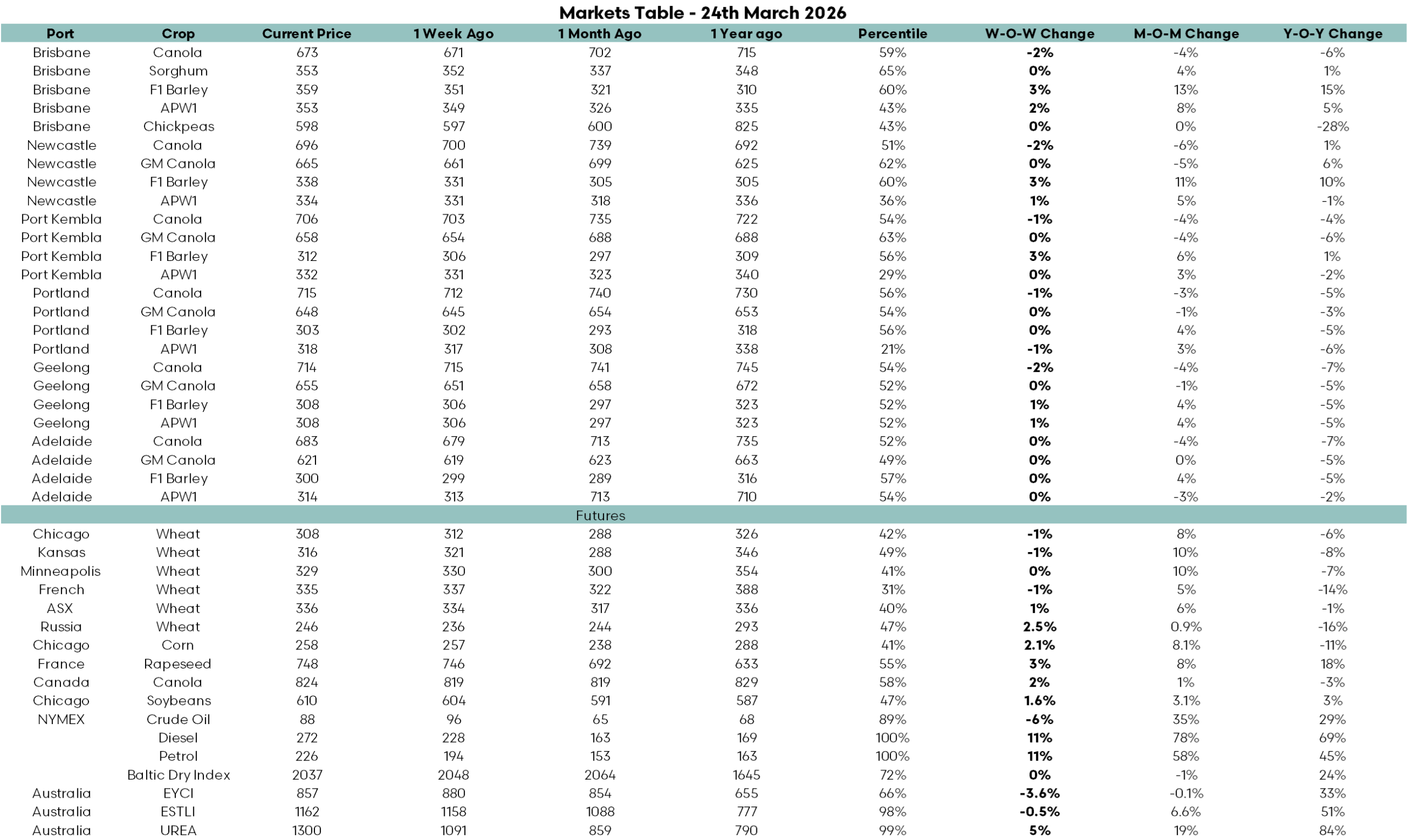

For now, the market remains balanced between competing forces, with uncertainty on both the supply and demand sides preventing a clear direction. Grain prices across the Australian market reflect this, with barley leading, lifting around 3pc week on week and sitting 6pc to 13pc higher over the past month, while wheat has edged higher more modestly, generally up 0pc to 2pc on the week and 3pc to 8pc month on month. Canola has softened, slipping 1pc to 2pc week on week and sitting 3pc to 6pc below month ago levels, despite supportive global signals, while sorghum has remained steady and chickpeas continue to underperform, leaving the domestic market broadly stable but lagging behind stronger moves seen offshore.