Urea vessels are flowing – but is it enough?

Market Morsel

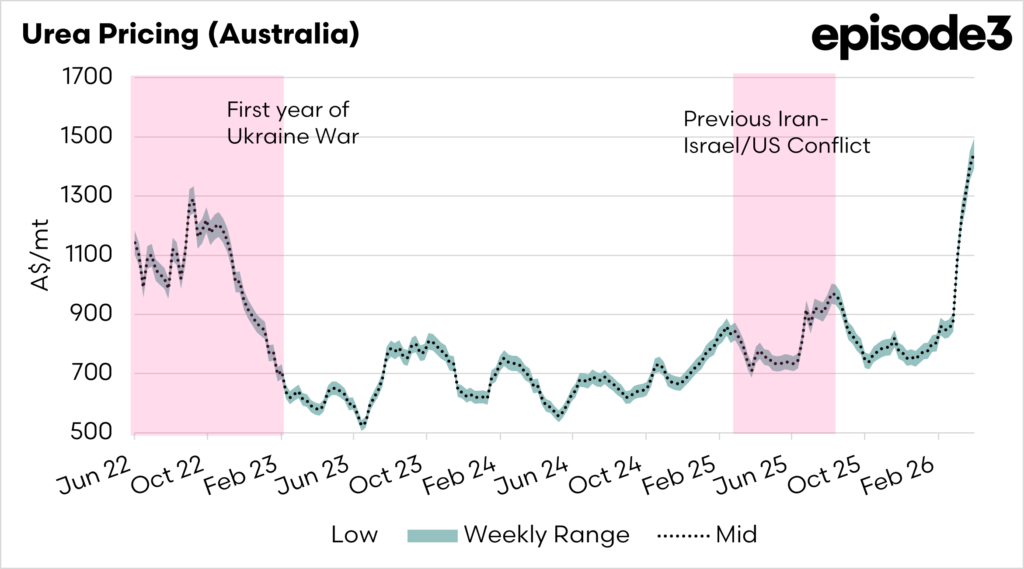

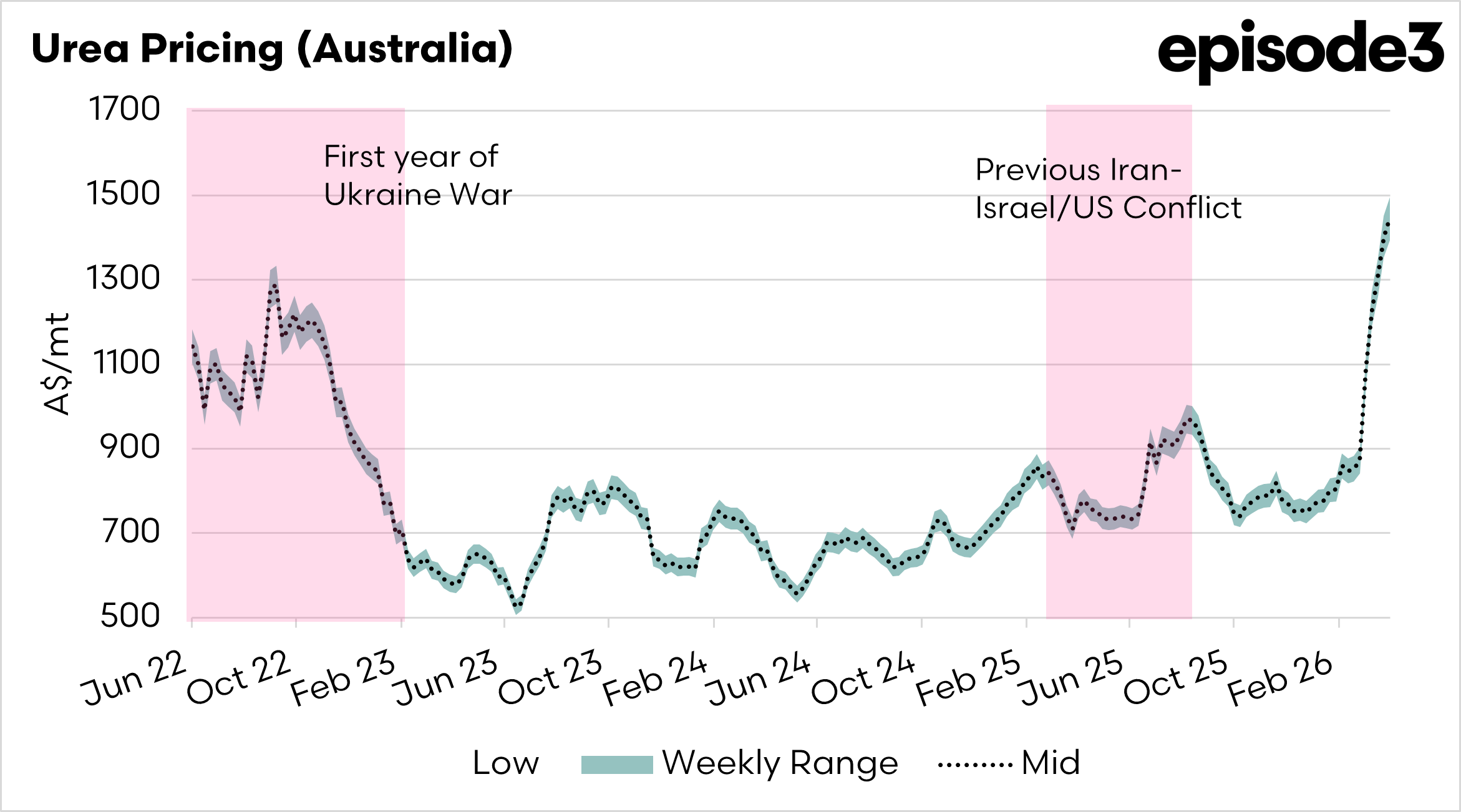

Australian urea prices continue to rise, with the market now firmly in a supply squeeze ahead of the winter cropping program.

The Episode3 landed Australia pricing, which models how much it costs to purchase Urea and land it in Australia suggests a price between A$1445 and A$1495, now significantly higher than the pricing during the height of the Ukraine crisis. The difference was that during that period, grain prices were substantially higher.

Planting for wheat, barley and canola is only weeks away, and both price and supply are major issues.

There appears to be enough product in the system to cover initial planting demand, but confidence drops sharply beyond that window.

There are increasing concerns that while tonnes exist globally, they may not arrive into Australia in time.

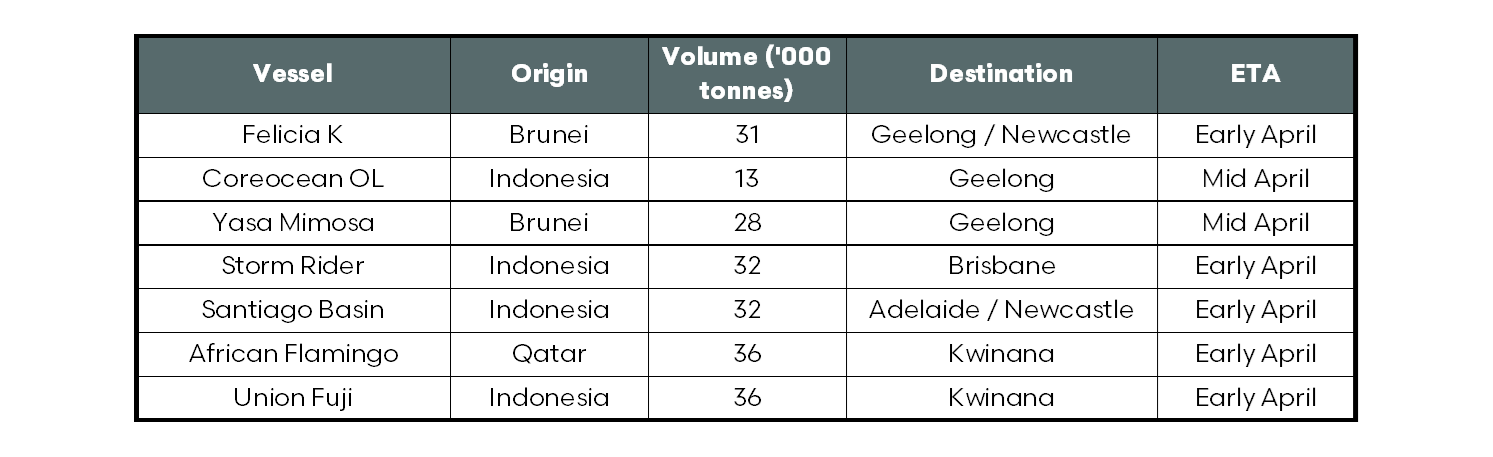

Below is a snapshot of some of the cargoes which, according to our prototype fertiliser tracker, are heading into Australia. Even with this flow of vessels, the system remains tight. And now, another layer of pressure is building offshore.

India has entered the market with a 2.5Mt urea tender. In a normal year, this would be routine. In this market, it is anything but.

India is the world’s largest importer and effectively acts as a price setter when it tenders at scale. With Indian domestic production under pressure and global supply constrained, this tender is expected to clear well above recent benchmarks.

That matters for Australia because we are competing for the same tonnes. In a tight market, the highest bidder, or the most urgent buyer, sets the tone.

The result is a market where prices are rising, supply chains are stretched, and the real risk is not whether urea exists globally, but whether it lands in Australia when it is needed most.