Market Morsel: Northern Premiums Ready to Wake

Market Morsel

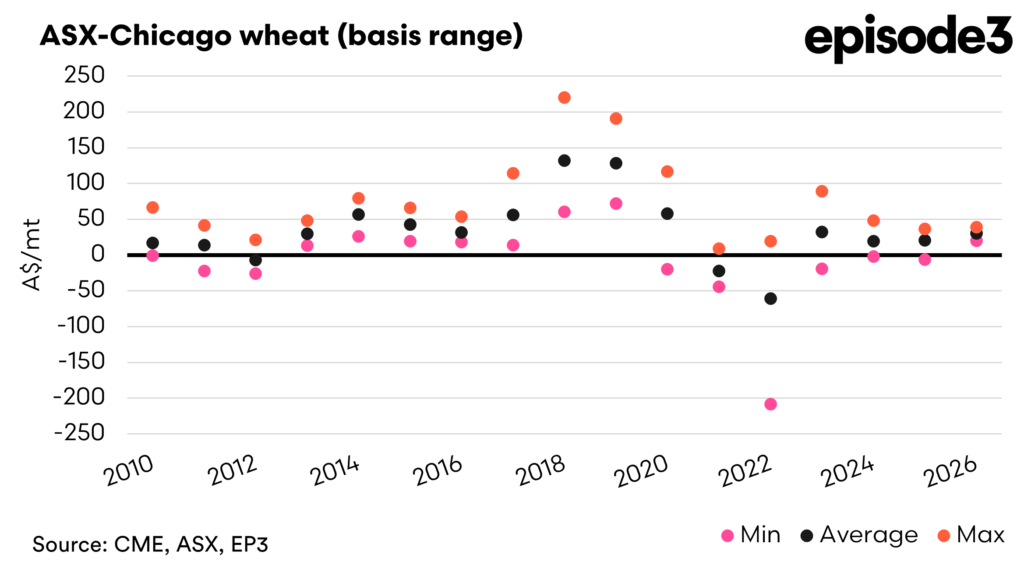

The grain market is beginning to shift, and the signal is increasingly coming from within Australia rather than offshore. Basis, the difference between local cash prices and futures such as Chicago Board of Trade wheat, is where that shift seems to be starting to play out. Basis reflects domestic supply, freight and demand dynamics, and in seasons like this, it often becomes more important than the futures market itself.

At present, global futures have remained relatively steady. Geopolitical tension and Northern Hemisphere weather concerns have not translated into sustained upside, leaving Australian pricing more exposed to local conditions. Those local conditions are starting to tighten, particularly across northern New South Wales and Queensland, where dryness is building and subsoil moisture is declining. With the prospect of an El Niño becoming increasingly credible, the production outlook in the north is carrying more risk than the market currently prices.

Under a typical seasonal pattern, this is the point where the basis begins to lift. As production risk increases, local buyers move earlier to secure supply, while growers become more cautious with forward selling. In northern regions, where feedlots and piggeries underpin a large portion of domestic demand, this effect is often amplified. These consumers cannot afford to be short of grain, and when confidence in supply starts to waver, they tend to act quickly. The result is the emergence of local premiums, with cash prices strengthening relative to futures, sometimes quite sharply.

Basis levels are starting to show some energy but remain relatively subdued despite the emerging seasonal risks. The domestic market has not yet fully priced the potential tightening in supply, particularly in the north, where demand is concentrated, and production variability is highest.

For producers, that is the key takeaway. While the futures may remain relatively flat, the opportunity in a tightening season often sits in the basis. This is more so in areas where there is a disconnect; if Victoria/South Australia produces an average or above-average crop and Northern NSW/QLD doesn’t, the grain will flow north.

If El Niño conditions take hold and dryness persists, local premiums are likely to emerge, particularly in northern markets where domestic demand is strongest. That creates a different pricing environment from recent years, where global moves dominated, and reinforces the need to watch local bids closely.