Sheep meat processors get small gains

Sheep Processor Trading Conditions Model

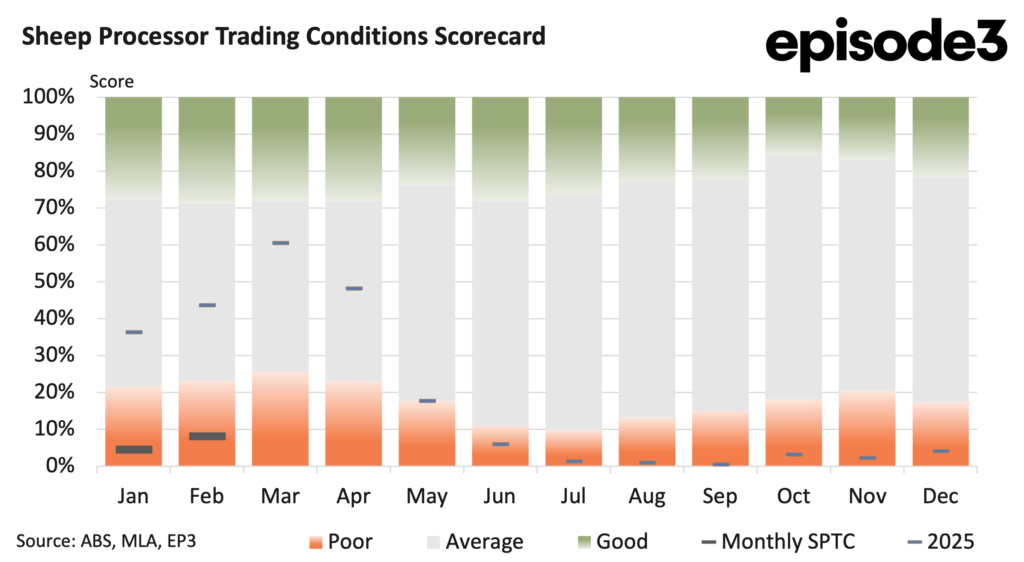

Sheep meat processor trading conditions improved modestly in February, but the broader picture remains one of significantly weaker margins compared to the same time last year. The February 2026 SPTC came in at 8.1 percent, improving from the revised January figure of 4.5pc.

Despite the month-on-month improvement, the annual average SPTC for the first two months of 2026 now sits at just 6.3pc, a dramatic decline from the 40pc annual average recorded at the end of February last year.

The scale of that deterioration highlights the growing disconnect between processor input costs and revenue growth across both domestic and export channels. While sheep meat processors have seen some recovery in margins compared to the weak finish to 2025, trading conditions remain historically constrained. The primary driver behind the weaker conditions has been the substantial rise in livestock procurement costs over the past twelve months.

Compared to February last year, heavy lamb prices are now 35pc higher, significantly increasing the cost of securing finished stock for processors. Trade lamb prices have also risen sharply, sitting 43pc above year earlier levels, adding further pressure to operating margins given the importance of this category to processor throughput. Light lambs have experienced an even larger increase, climbing by 57pc compared to last February. The strongest movement has come from mutton, with sheep prices now sitting 113pc higher than a year ago.

For processors, however, the rapid escalation in sheep prices has created a major margin squeeze, particularly where export and domestic pricing have not risen at the same pace. While livestock input costs have surged over the past year, export revenue growth has been far more subdued.

Average export prices into China are approximately 11pc higher than they were in February last year, representing a moderate improvement in returns from one of Australia’s key sheep meat markets. The United Arab Emirates has also strengthened, with export values rising by around 13pc over the same period. Malaysia has provided the strongest improvement among the major destinations, lifting by roughly 32pc year on year. However, the United States market has moved in the opposite direction, with export values easing by close to 3pc compared to last February.

Given the importance of the United States as a high value destination for Australian lamb, this decline has reduced the ability of processors to offset rising livestock procurement costs. When averaged across the major export destinations, overall export values have only increased by around 10pc since last February.

This relatively modest rise stands in stark contrast to the scale of livestock price inflation faced by processors over the same period. The mismatch between procurement cost growth and export revenue growth explains much of the deterioration in processor trading conditions over the past year. Even in markets where export pricing has improved, the gains have not been large enough to fully compensate for the dramatic increase in livestock costs.

The domestic market has provided somewhat stronger support. Retail lamb prices are now nearly 13pc higher than they were at the same time last year, indicating that some price increases have been passed through the supply chain to consumers. However, even the rise in domestic retail pricing remains well below the increases recorded in livestock procurement costs. This means processors continue to absorb a substantial portion of the margin pressure rather than fully passing it on downstream.

The current margin environment also continues to be clouded by incomplete co product and offal data. Updated values for offals, rendered products and co products from Meat and Livestock Australia remain unavailable, with no releases since September 2025. As a result, these components cannot yet be included in the SPTC calculations for recent months.

Given the importance of co product returns to total carcass value, the absence of these figures means the current processor margin estimates remain incomplete and could be revised once the missing data becomes available. Depending on the direction of those revisions, processor conditions may prove to be either slightly stronger or weaker than currently estimated.

Despite the improvement in the February index compared to January, the broader trend remains clear. Processor margins have deteriorated substantially over the past twelve months as livestock costs have risen much faster than revenue streams across both export and domestic markets. The extraordinary rise in mutton prices has been particularly significant, while lamb procurement costs across all categories have also lifted sharply.

At the same time, export markets have delivered only moderate pricing growth overall, with weakness in the United States further limiting revenue gains. Domestic retail pricing has increased more strongly than exports, but still not enough to offset the scale of input cost inflation.