Prices ease as northern supply improves

Market Morsel

The latest sheep and lamb yarding data from April to May shows a market that is becoming increasingly fragmented between regions, with some states seeing improved throughput as producers respond to elevated prices, while others remain exceptionally tight. At the same time, lamb and sheep prices have softened noticeably over the past four weeks, suggesting that the recent increase in throughput in some regions has temporarily eased supply pressure on processors.

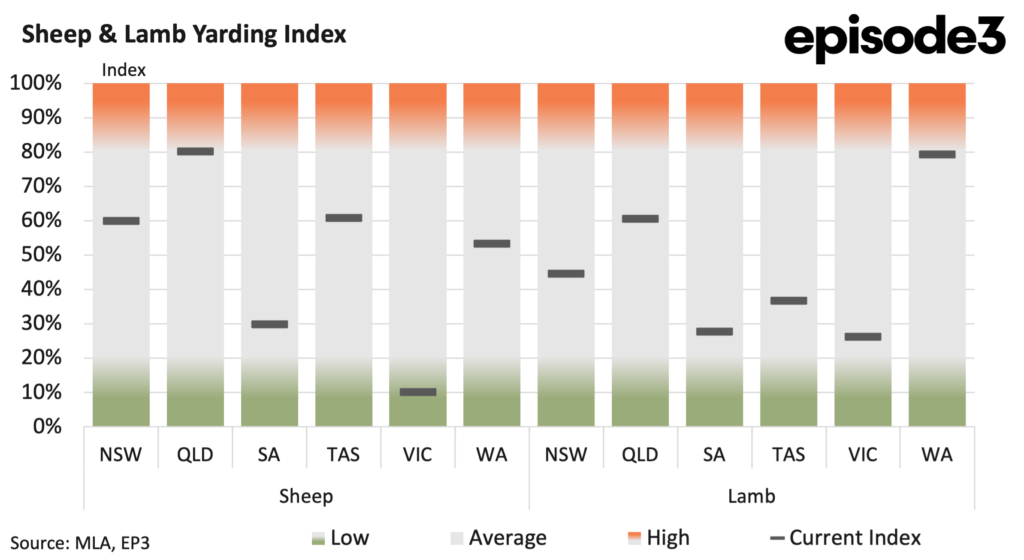

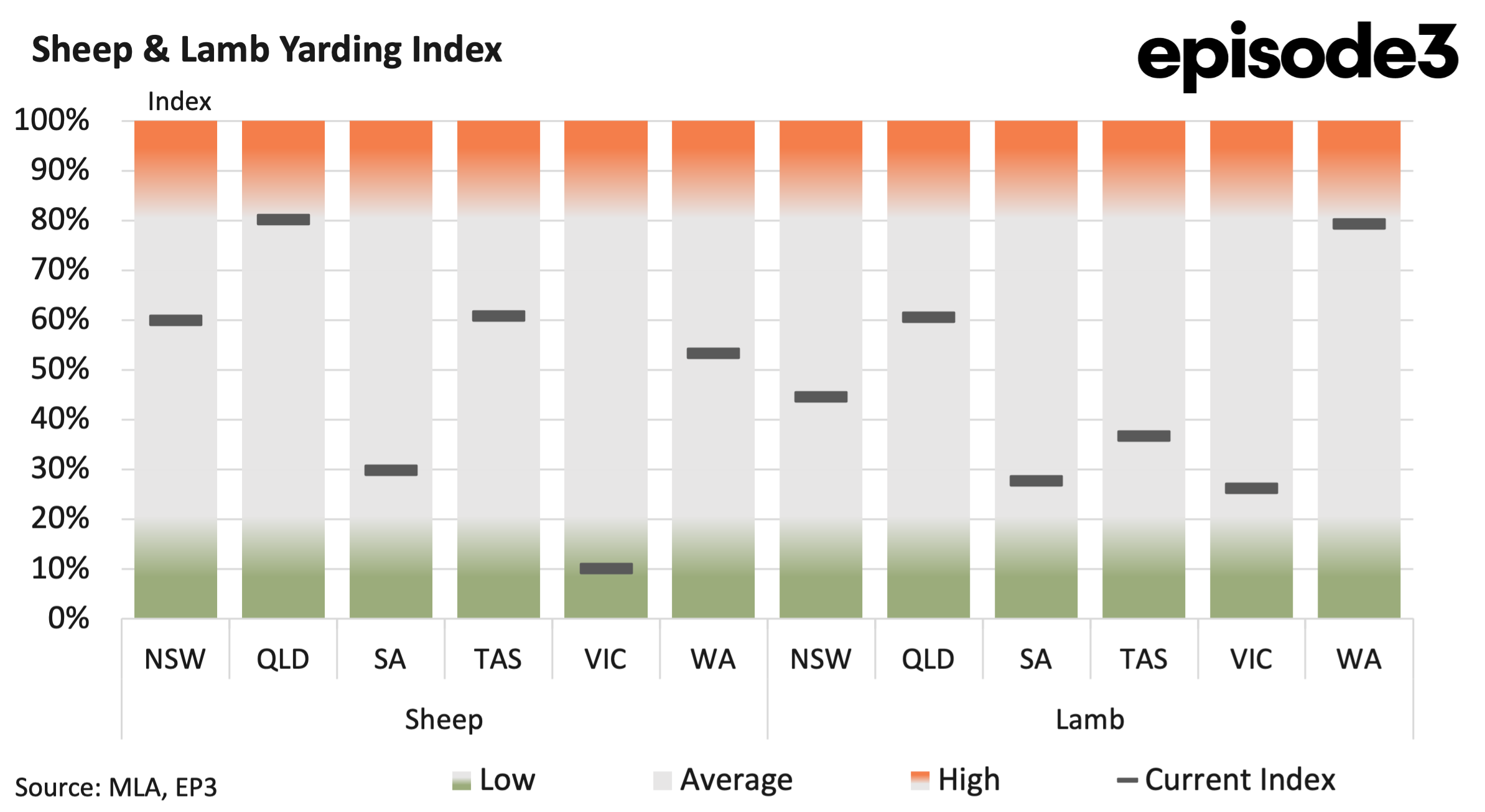

Sheep yardings increased across several major producing states during May, pointing to a modest rebound in marketings following the tighter conditions evident during April. New South Wales sheep yardings lifted from 48pc in April to 60pc in May, indicating a significant increase in throughput and suggesting producers have become more willing to market stock into the stronger pricing environment. Western Australia also recorded an increase, rising from 47pc to 53pc, reinforcing the view that the west continues to provide relatively solid sheep supply compared to conditions across the eastern mainland.

Tasmania edged slightly higher from 59pc to 61pc, suggesting stable supply conditions following earlier fluctuations. Queensland remained the strongest sheep supply region nationally despite easing from 93pc to 80pc, although yarding numbers in Queensland are a fraction of the other states.

South Australia moved lower from 36pc to 30pc, remaining one of the tightest sheep supply regions in the country. The relatively subdued throughput in South Australia highlights the ongoing constraints in sheep availability that have persisted for much of the year. Victoria recorded the sharpest tightening in sheep supply, falling from 18pc in April to just 10pc in May.

This extremely low reading reinforces how constrained Victorian sheep availability has become and suggests that the state is now operating in one of the tightest supply environments nationally. The sheep data shows that while some regions have increased marketings, national supply remains historically constrained, particularly across the southern mainland.

Lamb yardings painted a mixed picture during May, although the broader trend outside Western Australia was one of tightening throughput. New South Wales lamb yardings declined from 52pc in April to 44pc in May, indicating that the earlier seasonal flow of lambs continues to taper off. Queensland also eased from 69pc to 61pc, although throughput there remains relatively solid compared to other eastern states.

South Australia fell from 35pc to 28pc, reinforcing the tightening in lamb supply conditions that has been developing across the southern producing regions. Victoria also recorded a meaningful decline, easing from 39pc to 26pc and confirming that lamb availability is becoming increasingly constrained in one of Australia’s key processing states. Tasmania saw one of the largest changes, dropping sharply from 74pc to 37pc, which suggests that the earlier surge in throughput has now largely passed through the system.

Western Australia was again the clear outlier. WA lamb yardings surged from 58pc in April to 79pc in May, confirming that the west remains the dominant lamb supply region in the country and may still be working through the tail end of its seasonal flush. The divergence between Western Australia and the eastern mainland highlights how uneven supply conditions have become nationally. While much of the east is now moving into a tighter supply phase, Western Australia continues to provide elevated throughput that is helping balance national availability.

The increase in sheep and lamb yardings in some regions has coincided with a notable softening in pricing over the past four weeks. Heavy lamb prices declined by around 62c over the month, easing to approximately 1,066c per kilogram carcase weight. Trade lamb prices also softened significantly, falling by around 58c to sit near 1,135c per kilogram carcase weight.

Light lamb recorded the largest correction, dropping by more than 100c over four weeks to around 1,045c per kilogram carcase weight. Restocker lamb prices weakened by roughly 71c over the same period, indicating that producer demand for replacement stock has moderated following the earlier strong rally. Merino lamb also declined sharply, falling by approximately 88c over four weeks.

Mutton prices proved comparatively resilient, easing by around 32c to sit near 792c per kilogram carcase weight. Despite the recent correction, current prices remain historically elevated when compared to year ago levels.

Trade lamb prices are still nearly 297c higher than this time last year, while restocker lamb remains more than 400c above year earlier values. Mutton prices also remain around 275c above year ago levels, underlining the longer-term tightening in sheep numbers that continues to underpin the market.

Overall, the latest data suggests the sheep meat market has entered a short-term consolidation phase. Improved throughput in some regions has temporarily eased supply pressure and weighed on pricing, but the broader supply environment remains historically tight across much of the country.