Feedlot update Q1, 2026

March 2026 cattle on feed update

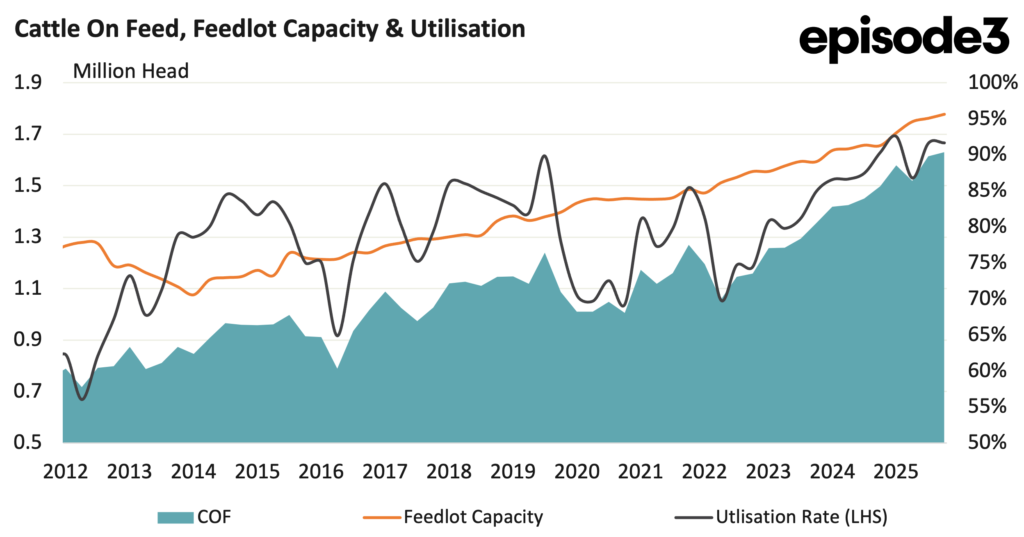

Australian feedlots did not just hold their ground in the opening quarter of 2026. They pushed into new territory. The March quarter feedlot survey showed another record for the sector, with national feedlot capacity lifting to 1.778 million head, up 1 percent from the December quarter and 7.3pc higher than a year earlier.

Cattle on feed also reached a new high at 1.630 million head, up 1pc on the previous quarter and 8.9pc above March 2025. Utilisation remained at 92pc, which is the key number in the story.

The sector is still expanding, but the extra space is being filled almost as quickly as it is built. That makes the Q1 result a continuation of the trend seen through 2025, rather than a pause after last year’s record run. Feedlots are no longer operating as a secondary pressure valve for the cattle market. They are now one of the central engines of the Australian beef supply chain.

The clearest evidence of that is in turnoff. Australian feedlots sent 1.047 million head to abattoirs in the March quarter, breaking the one million head mark for the first time. That compares with 947,200 head in the December quarter and 858,613 head in the March quarter of 2025. In other words, grain fed turnoff was up 10.5pc quarter-on-quarter and 21.9pc year-on-year.

Queensland remains the anchor of the system. It held 988,599 head of built capacity, equal to around 55pc of the national total, and turned off 632,873 head during the quarter. NSW also lifted capacity to 542,473 head, but numbers on feed eased after a strong lift in turnoff. These two states continue to dominate the national feedlot picture, but the broader message is that the system is running hard across most regions.

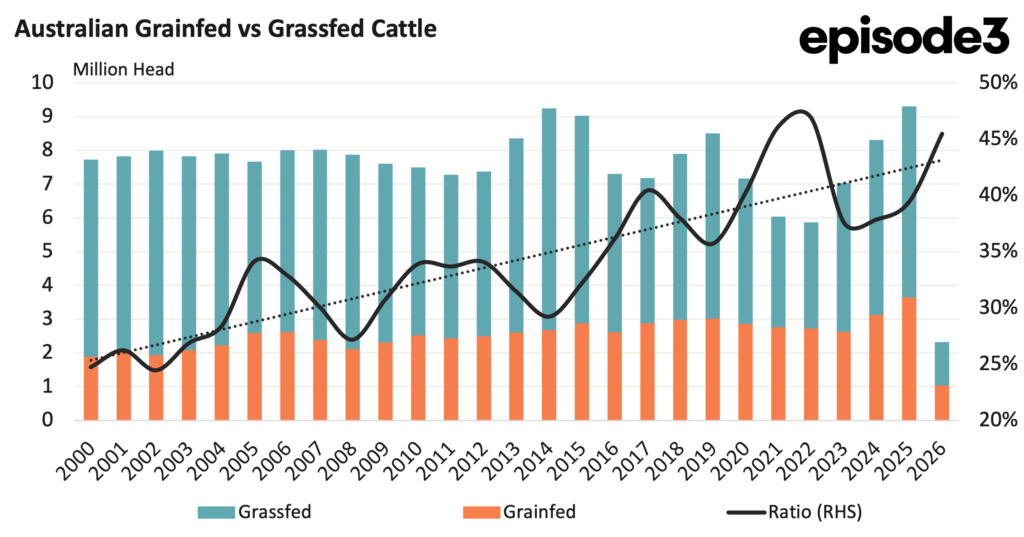

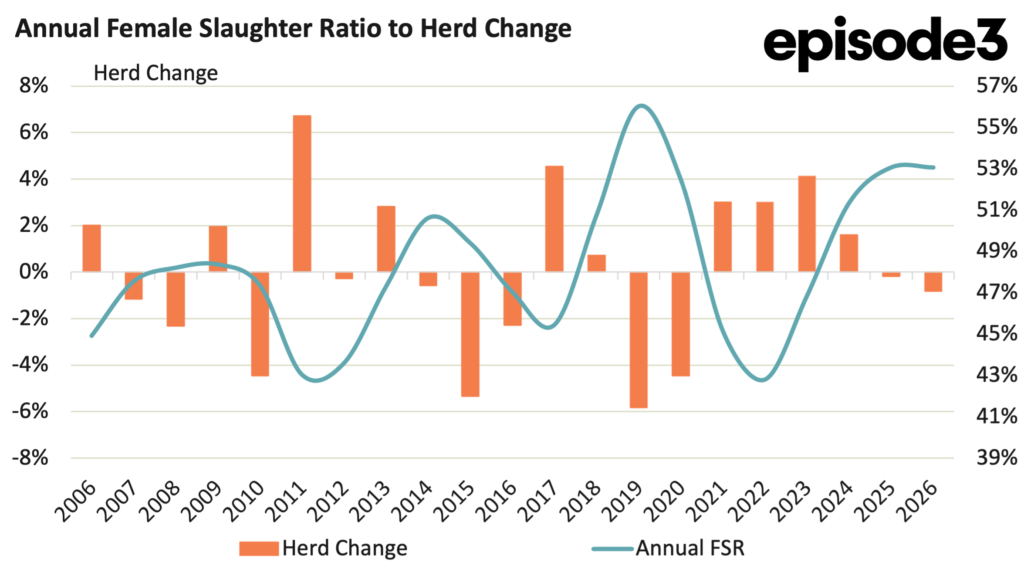

The more interesting shift is in the balance between grain finished and grass finished cattle.

In Q1, Australia processed 1.04 million grain finished cattle compared with almost 1.26 million grass finished cattle.

That lifted the grain finished share of adult cattle slaughter to 45.5pc, which is a substantial step up from the 2025 annual figure and much closer to what would normally be expected when a herd rebuild begins. In a classic rebuild phase, fewer cattle are available off grass because females are retained on farm and producers pull back slaughter numbers. Feedlots often take a larger share of the kill because they provide a more controlled and consistent supply stream when pasture-finished availability tightens.

On that measure, the Q1 feedlot data looks like a rebuild signal. The problem is that the female slaughter ratio is not telling the same story. The FSR sat at 53.1pc in Q1 2026, which is well above the level normally associated with herd rebuilding. A genuine rebuild phase usually requires a much sharper reduction in female slaughter, with more cows and heifers being held back to lift future breeding capacity.

At 53.1pc, the data points more towards continued liquidation pressure than meaningful retention. That fits with MLA’s forecast for the national cattle herd to decline in 2026

That makes the current feedlot data more complicated than it first appears. The rising grain fed share of slaughter could be read as a rebuild signal, but the FSR suggests the rebuild has either stalled or failed to get going properly.

Instead, the feedlot sector may be increasing its share because it is better positioned to manage supply chain demand, export specifications and processor requirements during a period of elevated slaughter.

Feed costs remain a risk. Darling Downs grain prices had lifted sharply since the start of the Iran conflict, adding pressure to feed costs. That matters because the sector is now operating at scale. When cattle on feed are above 1.6 million head, small shifts in feed grain prices have large implications for margins.

The Q1 feedlot numbers therefore tell two stories at once. The first is that Australian lot feeding keeps getting bigger, more utilised and more important to national beef supply. The second is that the growing grain fed share looks like a rebuild signal, but the female slaughter ratio says the underlying herd has not yet turned the corner.

Feedlots are doing more of the heavy lifting, but they are not necessarily doing it because the herd rebuild is underway. They may be doing it because the rebuild is delayed, grass fed supply is uneven, export demand remains strong, and processors need consistency in a cattle market that is still trying to find its next cycle.