Is Canberra distorting the fertiliser market by picking winners?

The Snapshot

- The government’s fertiliser underwriting scheme helps some importers avoid price risk while others trade fully exposed.

- Fertiliser is hard to hedge because there’s no futures market, it’s all physical trading.

- A single cargo price swing can cost an importer millions, threatening the viability of their business.

- The scheme lacks transparency, with key details not shared publicly or with other industry participants.

- Phosphate supply is the next pressure point, and the lessons from this intervention need to be applied before it hits.

The Detail

When the Federal Government announced its fuel and fertiliser security facility, the immediate logic was easy enough to understand. Australia is heavily exposed to imported agricultural inputs. When global supply chains are disrupted, Australian farmers can quickly find themselves at the mercy of international pricing, shipping availability, currency movements, and importers’ willingness to take risks. Fertiliser is not a discretionary purchase for broadacre producers. If the product is not available when needed, yield potential can be lost quickly.

So, on one level, government intervention made sense. If the market was too volatile for private importers to confidently commit to cargoes, then some form of risk-sharing could help ensure fertiliser actually arrived in Australia. From a grower’s perspective, availability matters. A perfect free market is not much use if there is no fertiliser on the farm when crops need feeding. Episode 3 raised a warning on the day the facility was announced. The concern was not that the government had stepped into the market. The concern was that underwriting private import risk could create unintended consequences in pricing, competition, transparency and market behaviour (see here).

That warning now looks increasingly important. The key issue is how underwriting works. This is different from the government simply buying fertiliser and distributing it. It is a price-risk mechanism. If an importer commits to an expensive offshore product and the market falls before that product is sold domestically, the downside risk may be absorbed or offset by the public balance sheet. That changes the commercial equation. A normal fertiliser importer must ask whether it can carry the full risk of a cargo. An underwritten importer can act with more confidence because at least part of the downside may have been shifted off its balance sheet.

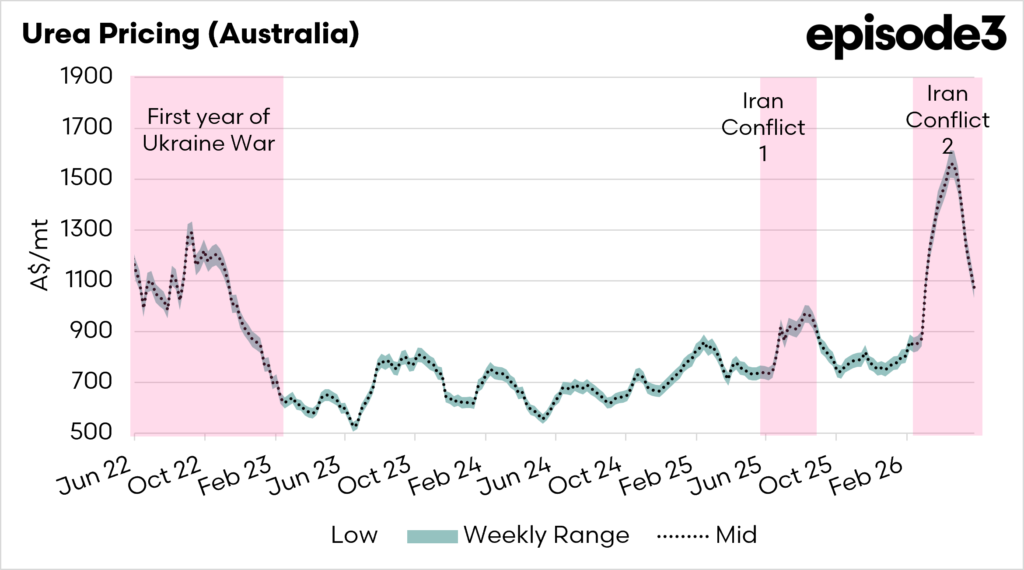

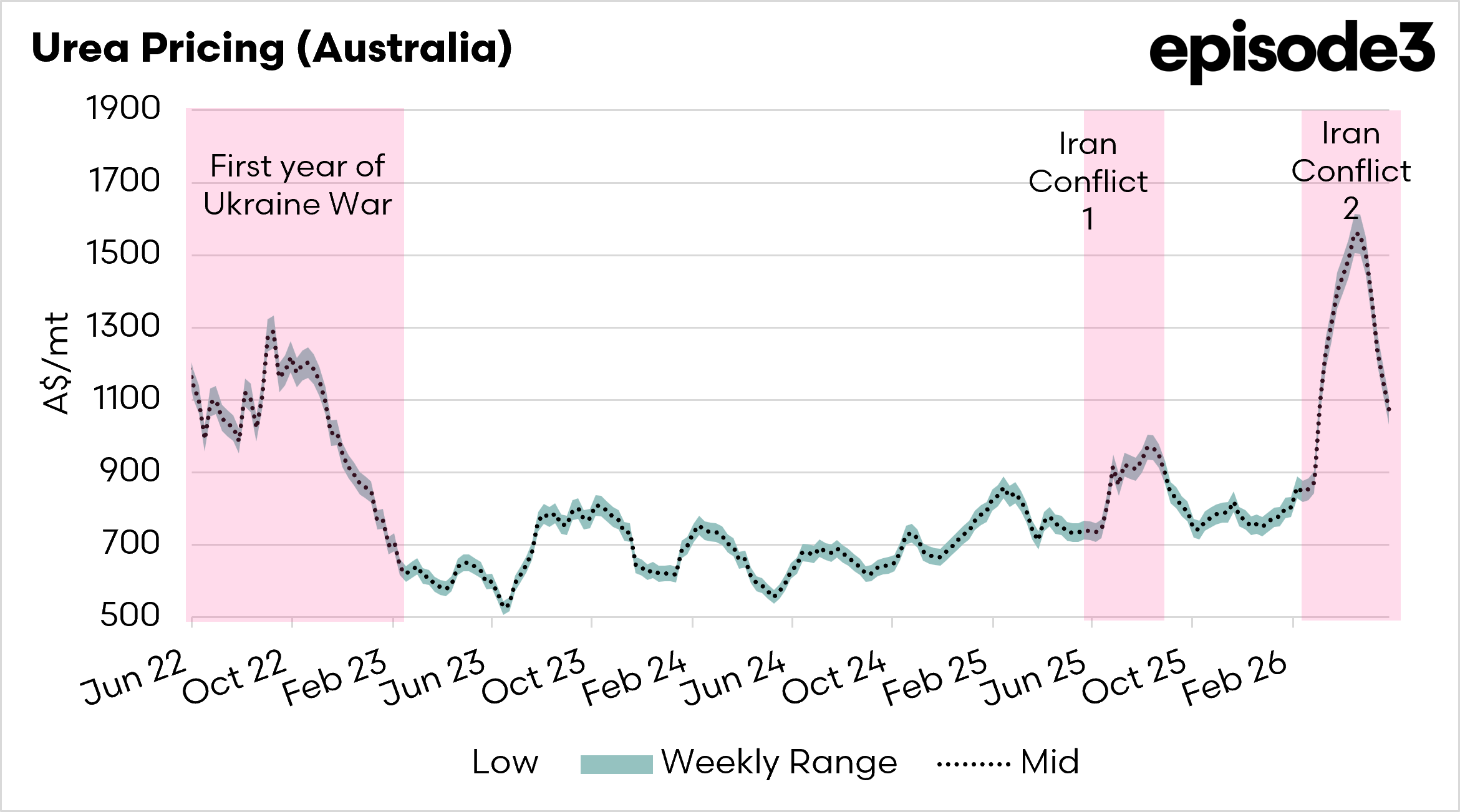

That distinction matters because fertiliser importing is a high-volume, low-margin physical trade. The numbers involved are large, and the market can move sharply. On AgWatchers, Mark Been from Marnco gave a simple example of what that risk looks like in practice. “If an importer brought in urea at US$950 and then the market subsequently moved US$250, an importer would lose US$250 a tonne. Over a cargo, that equals US$7.5 million.” In a low-margin environment, he added, “that could really put a company’s future in jeopardy.” This is the part of the fertiliser trade that many outside the market do not see. A cargo position is not a small bet. It is a major exposure.

That is also why the debate should not be reduced to whether a farmer can buy a cheaper tonne of urea this week. Every grower wants lower input costs, particularly in a season where margins can be squeezed from both sides. But the bigger question is who bears the risk behind that cheaper tonne. If the market falls, does the importer bear the loss? Does the reseller wear it? Does the grower indirectly wear it through future supply and pricing? Or does the taxpayer now sit behind part of the trade?

Fertiliser is also different from many agricultural commodities because the hedging options are limited. In grain, there are futures markets, visible benchmarks and a wider set of tools for managing price risk. Fertiliser is more opaque. It is physical, negotiated and often dependent on timing, location, freight and replacement values. Mark put it plainly: “There’s no real hedge market. Our hedge is a sale to a reseller who’s backing that risk with a farmer. So it’s all physical.” In that type of market, a government-backed price-risk mechanism is not a minor intervention. It changes the way risk is allocated across the supply chain.

This is where the facility moves from being a supply-security tool to something more complicated. If one importer has part of its downside risk removed, while another continues to trade with full exposure, the two businesses are no longer running under the same conditions. One has a safety net. The other has to price, buy and sell with its own balance sheet fully exposed. Mark summed up the practical concern clearly: “We’re now in the market competing against companies that have what’s called a price-risk mechanism to cover them on the downside.” That is the heart of the issue. The policy may have been designed to secure supply, but if it is not applied evenly, it can create a two-speed fertiliser trade.

The strongest argument for the scheme is that growers may receive upfront help from cheaper fertiliser. That should not be dismissed. In the short term, it is entirely understandable that growers care most about whether fertiliser is available and what it costs. But short-term price relief and long-term market health are not always the same thing. Mark acknowledged the farmer’s benefit directly, saying: “To be upfront, it’s fantastic for the farmer to get that discount upfront. But there’s an opportunity cost, because long-term competition and free markets are compromised.” That is probably the most important line in the whole discussion. It recognises the short-term benefit while warning about the long-term cost.

This is the classic problem with government intervention in markets. The first-order effect is often easy to see. More product on the water. More confidence around availability. A lower price to the end user. The second-order effects are harder to measure but often more important. What happens to importers who committed to stock before the intervention? What happens to resellers who bought at full market risk? What happens if unsupported businesses become more cautious about taking future positions? What happens if the market ends up with fewer active participants because emergency support effectively favoured some balance sheets over others?

The risk does not disappear. It moves. In some cases, it moves from the importer to the taxpayer. In other cases, it stays with those outside the scheme. Either way, the intervention changes behaviour. That is the whole point of the policy. But once government support changes behaviour, the need for transparency becomes much greater. This was the unresolved question from the start. Who determines the import price? Who determines the realised sale price? What benchmark is used to decide whether a loss has occurred? How is that loss verified? Who audits the scheme? Are the rules the same for all participants? Is there any restriction on supported firms using government-backed downside protection to discount into the domestic market?

These are not academic questions. They sit at the heart of whether the facility is simply supporting national supply or whether it is unintentionally picking winners in the fertiliser trade. Mark’s comments on AgWatchers went directly to this point. “We don’t know exactly the inner mechanics of it, and it’s not being shared with other fertiliser businesses, as far as I know, or the general public. If you thought fertiliser was opaque, now it’s even more opaque.” That is a serious statement. It should worry growers, importers, resellers and taxpayers alike. Once public money is used to underwrite private market risk, the public deserves to know how the mechanism works.

The scheme may not be a subsidy in the traditional sense. It may not involve a fixed payment per tonne, and it may only operate when the market moves against an importer. But in commercial terms, it can still behave like a subsidy because it reduces risk for selected participants. If supported importers can sell with downside protection while unsupported importers must meet the market and take the hit themselves, the government is no longer just supporting supply. It is changing competitive conditions. That may not have been the intention, but unintended consequences are exactly the point.

This is why the discussion with Mark Been on AgWatchers is worth listening to in full. Fertiliser is often discussed from the grower’s end, where the focus is understandably on price and availability. But the podcast gets into the mechanics behind the trade: how importers take physical positions, why fertiliser is difficult to hedge, how quickly a falling market can damage a balance sheet, and what happens when government support changes the risk profile for some participants but not others. It moves the debate away from simple supply security and into the less visible issues of market structure, transparency and competitive neutrality.

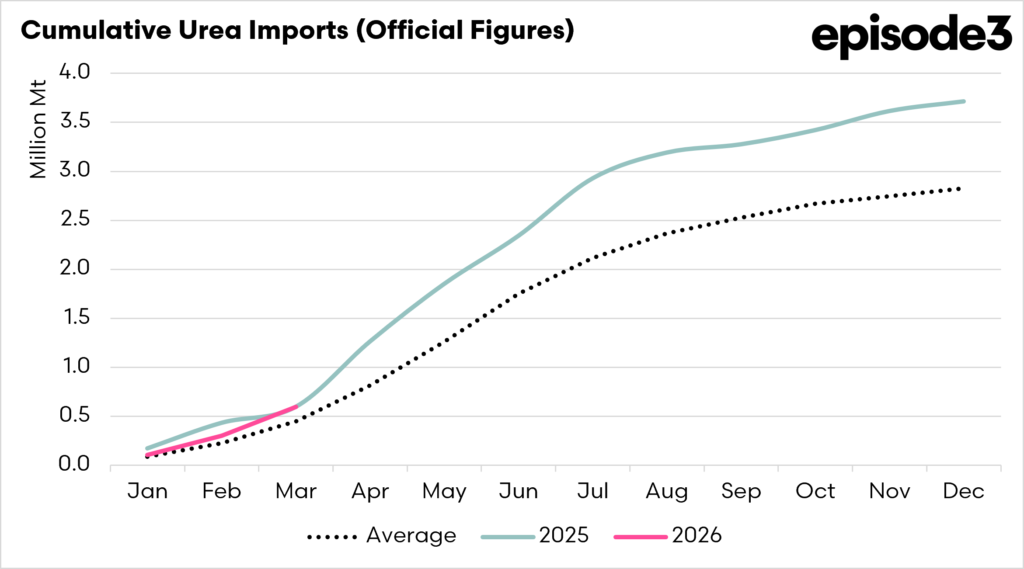

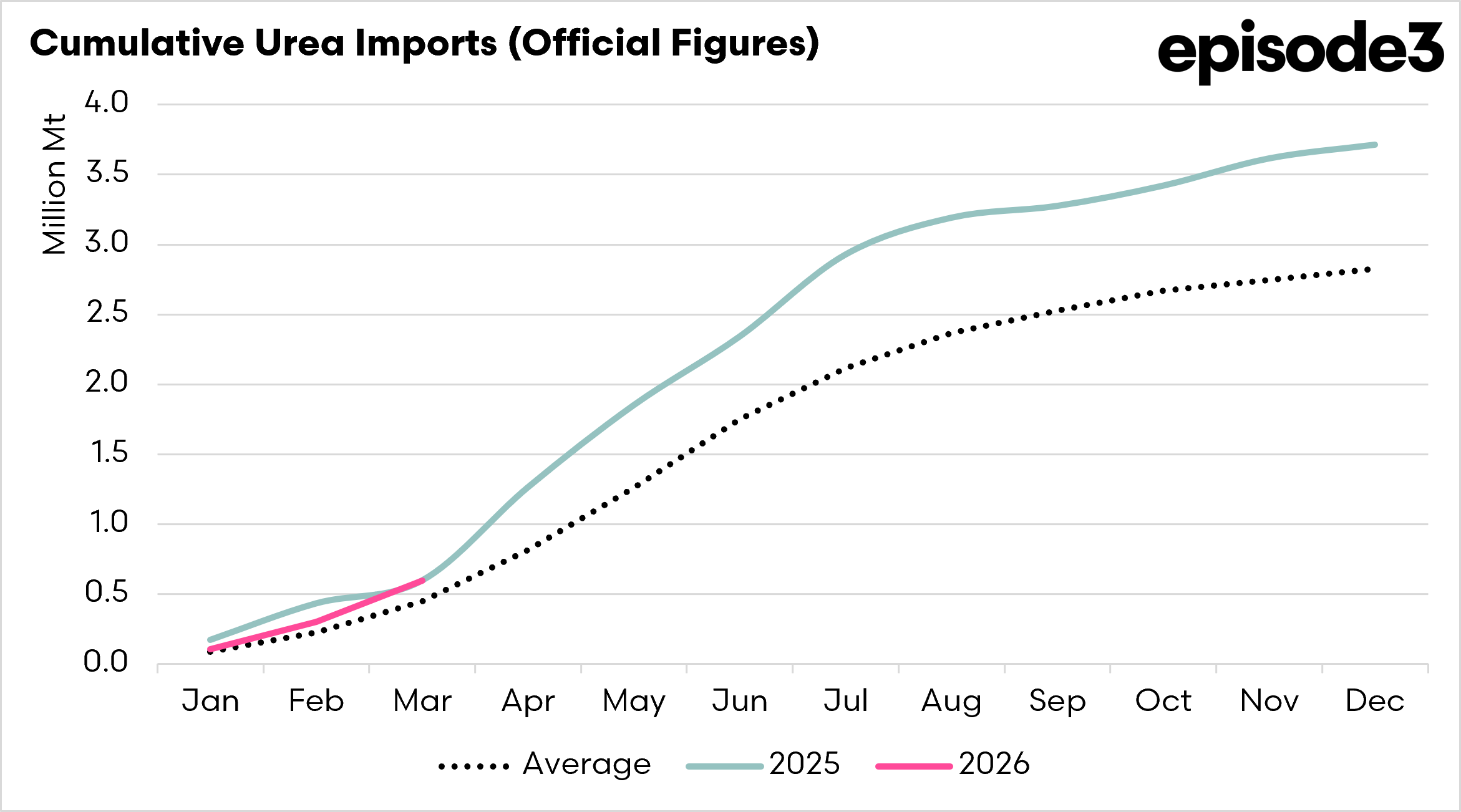

This matters even more because urea may not be the final test. On AgWatchers, Mark argued that nitrogen supply has largely settled for the time being, but phosphate is the next pressure point. “From a nitrogen perspective, it is fixed for the time being,” he said. “When I said tenuous, I was really looking forward to phosphates.” That warning matters because if the first intervention was rushed in response to a perceived urea supply crisis, the next one should not be designed in the same fog. If phosphate supply tightens further, the government needs clear access rules, clear pricing rules, and clear oversight from the start.

Fertiliser security is important. No one should pretend otherwise. Australia cannot afford to be complacent about critical input supply, particularly when global trade flows are fragile. But public underwriting of private market risk needs sunlight. It needs clear rules, open access criteria, consistent treatment, independent verification, and public accountability for the taxpayer exposure it creates. The aim should be fertiliser security, not fertiliser favouritism. Emergency support may be justified, but it must not accidentally reshape competition in one of Australian agriculture’s most important input markets.