Global cattle pricing update June 2026

Get short video updates on your phone

For quicker updates as markets move, follow @themeatwatcher on Instagram. I regularly post short summaries and charts breaking down what’s happening in meat proteins and broader ag markets so you can stay across the key moves without having to read through pages of analysis. If markets are moving quickly, that’s usually where the updates will land first.

Global cattle price update - June 2026

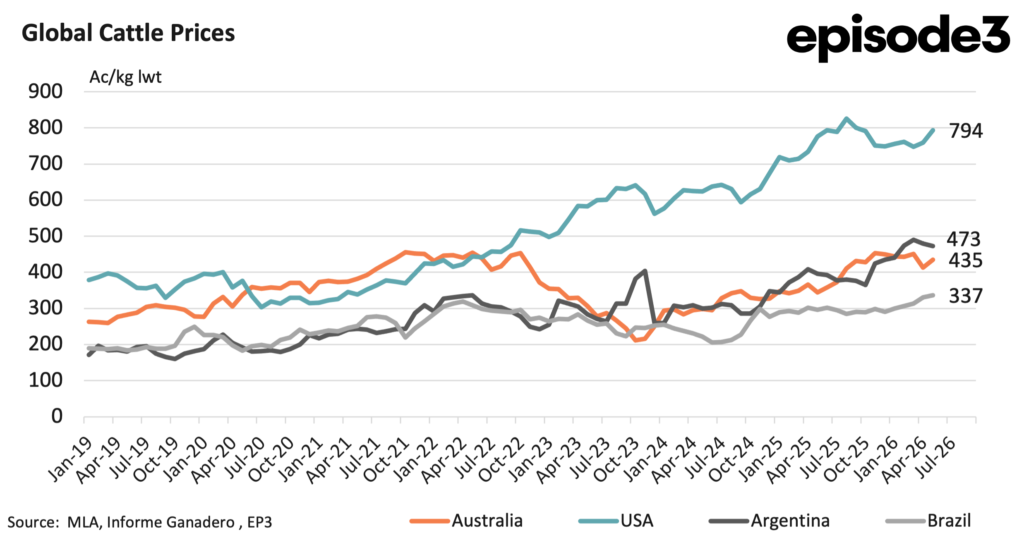

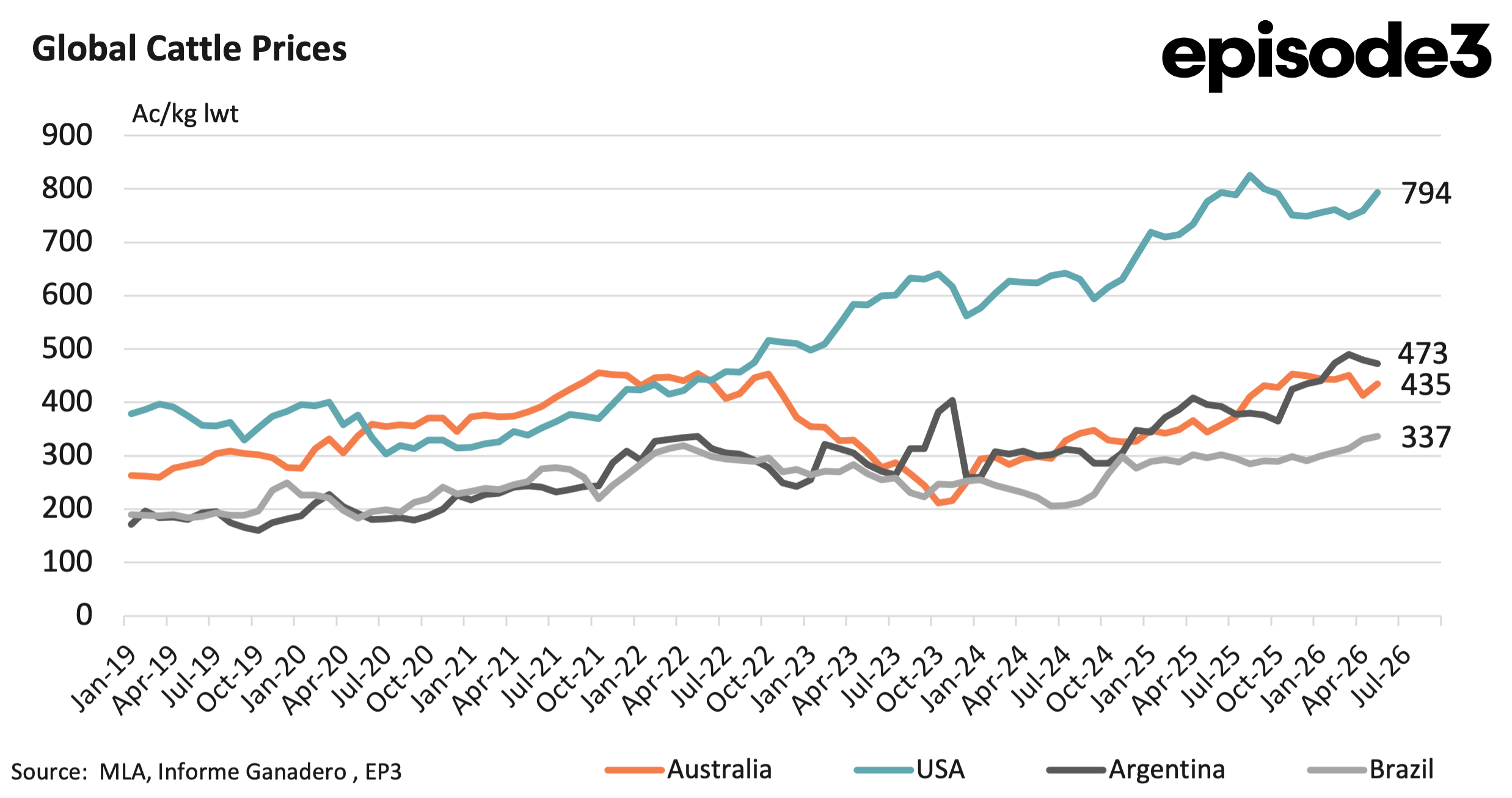

Global cattle prices strengthened through May, although the gains were not evenly spread across the major beef producing nations. The latest EP3 global cattle price update shows Australia posting a solid monthly lift, but the US also moved higher and remains far and away the most expensive market in the comparison.Brazil edged up from a much lower base, while Argentina was the only one of the four markets to ease.

Measured in Australian cents per kilogram live weight, Australian heavy steer prices rose from 414Ac/kg lwt in April to 435Ac/kg lwt in May. That was a 5pc lift over the month and a useful rebound after the softer tone seen earlier in 2026. Helpfully for Australian beef export competitiveness is that the US matched that move.

US heavy steer prices rose 5pc as well, increasing from 759Ac/kg lwt in April to 794Ac/kg lwt in May. That keeps the US firmly in a league of its own. Australian heavy steer prices are still sitting 45pc below the US. That gap remains one of the defining features of the global beef market.

The US cattle market continues to be underpinned by tight cattle supplies, with the legacy of earlier drought and herd liquidation still flowing through the system. That has kept a strong floor under cattle prices and, in turn, under US beef values. For Australia, that remains helpful from a trade perspective.

As long as US cattle and beef prices stay elevated, Australian product retains a meaningful pricing advantage in key markets where the two exporters compete directly. That is particularly relevant into key export markets such as Japan, South Korea and China.

Argentina moved the other way in May. Heavy steer prices there eased from 480Ac/kg lwt to 473Ac/kg lwt, a decline of 1pc. Even with that softer result, Argentina still sits above Australia in the global ranking. Australian cattle are currently 8pc below Argentina.

That discount is much smaller than the gap to the US, but it still matters. Argentina remains an important global beef producer and, when the policy and economic settings line up, a significant export competitor.

Brazil remains the cheapest of the major cattle markets in the comparison. Brazilian heavy steer prices lifted from 330Ac/kg lwt in April to 337Ac/kg lwt in May, a 2pc increase. Even so, Australian prices remain 29pc above Brazil. Brazil’s price advantage continues to be most important in price sensitive export markets, especially China and other destinations where cost can carry more weight than provenance or quality.

So where does that leave Australia. The answer is in much the same position as before, just with slightly better domestic pricing. Australia sits in the middle of the global cattle price pack. It is still heavily discounted to the US, modestly discounted to Argentina, and clearly above Brazil. That is not a bad place to be.

Australia remains competitively priced against the US, which matters in premium export channels. It also now holds a small pricing advantage against Argentina. But it is still well above Brazil, meaning price sensitive competition remains a challenge.

The May result is therefore positive without changing the broader global structure. Australian heavy steer values improved, which is good news for local producers. But the global pecking order remains intact with Australia continuing to occupy the middle ground and still competitive in the key export markets that matter.