Market Morsel: Has the Fertiliser Storm Passed? Urea prices crash

Market Morsel

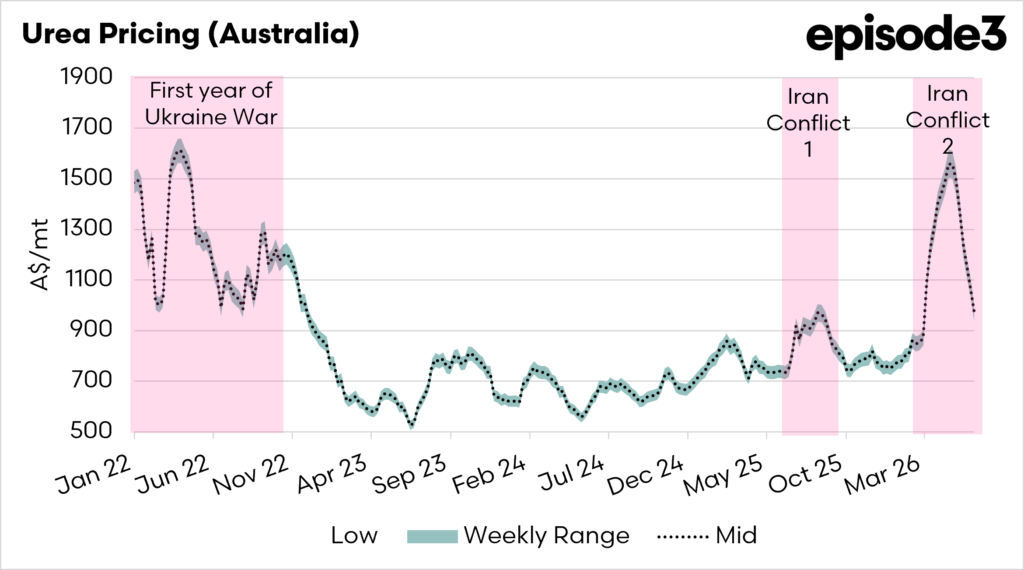

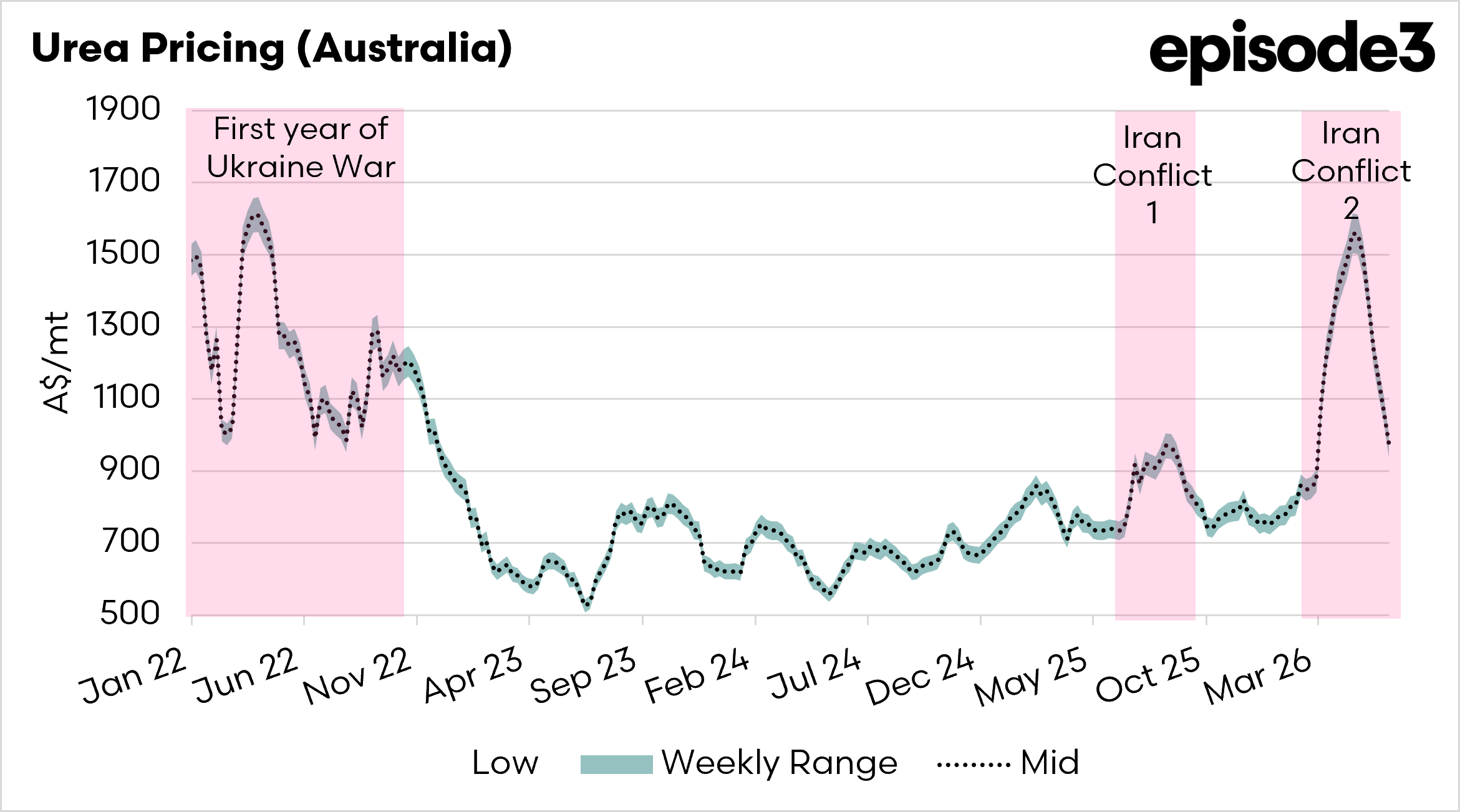

The fertiliser market has undergone a remarkable shift over the past month. Only a few weeks ago, growers were focused on whether global supply disruptions would push nitrogen prices even higher. Today, the conversation has changed to how much further prices might fall.

The reason for the recent correction has been the easing of concerns surrounding Middle Eastern supply. Earlier fears that conflict in the region could severely disrupt fertiliser exports and shipping routes through the Strait of Hormuz helped push urea prices sharply higher. Since then, production has resumed at several facilities, shipping flows have improved, and buyers have become less concerned about immediate supply shortages.

China’s return to the export market has also weighed on prices. Export quotas have been released, and additional tonnes are expected to reach international markets over the coming months. At the same time, India, the world’s largest urea importer, has moved to secure supplies through a major purchase tender. The market expectation is that values achieved in that tender will be well below the levels seen during the recent supply scare.

The impact is clearly visible in the EP3 Urea Import Parity Model. The model estimates the landed replacement cost of imported urea into Australia, including purchase values, freight, unloading costs, and an allowance for commercial margins. According to the model, the mid-range replacement value has fallen from around $1,237/t a month ago to $971/t this week. That is a decline of more than $260/t in just four weeks.

While that is welcome news for growers, some perspective is still needed. These price declines may not be reflected at once to the grower. The current replacement value remains roughly $230/t higher than the same time last year. In other words, fertiliser has become considerably cheaper than it was a month ago, but it is not yet cheap by historical standards.

The broader fertiliser market is also telling two different stories. Nitrogen values have retreated sharply, but phosphate markets are still far more stubborn. Global DAP and MAP prices continue to be supported by Chinese export restrictions, elevated sulphur prices and ongoing supply constraints from major exporters. As a result, phosphate affordability remains challenging despite the decline seen in urea.

For Australian growers, the recent correction in nitrogen prices provides some relief heading into key fertiliser application periods. However, fertiliser markets remain heavily influenced by geopolitics, energy prices and government policy decisions. The sharp fall in urea values over the past month demonstrates how quickly sentiment can change. While the immediate supply panic appears to have passed, fertiliser remains one of the most volatile input markets facing Australian agriculture.