Why I love agriculture

Independent Contributor

I’m going to start by making a bold and possibly insulting statement, clearly working in Melbourne with a dairy farm in NZ I am a part time farmer. However, so is every one of you….

Allow me to elaborate, ‘Wealth Creation’ is a relatively new phrase and sounds like it was invented by a spoilt millennial with an Art’s degree. However, lets break down where your wealth has been created over the last 20 years, unless you are ‘playing the long game’ you should probably invest elsewhere.

So let’s do a basic high level analysis of a 2,000 acre livestock or cropping property worth circa $2000/acre in 2004 and $6,000/acre now, with an average EBIT of $80/acre then to $200 now, half of this going in interest costs and a quarter in Capital improvements.

Let’s give it an average left over of $40/acre/year or $80,000/year or $1.6 million in 20 years.

Meanwhile the land has increased from $4 million to $12 million.

Now you can winge all you like about droughts and being asset rich and cash poor, but the reality is at these figures 85% of your wealth improvement is effectively real estate. Even if you double you EBIT or halve the land value improvement, it’s still the larger part of your business.

For those who have taken risks, (many had unfortunate timing and left the industry) and expanded their operations, often seeing all their EBIT gone in interest or even carrying losses, the wealth creation can be over 90% of their business.

I will use our family as a classic example, my parents brought their first farm together in 1971 (the year I showed up) with a $15,000 deposit on 800 acres for $150,000. 10% equity or an unfathomable risk appetite today.

In our case as soon as land values increased, and our equity increased to 60-70% we kept buying and borrowing back down to 40-50% equity. 50 years later my 2 brothers and sister agreed on how we split circa 10,000 acres across sheep, beef, dairy and grapes, still operating at 50-60% equity.

We honestly don’t know the exact split of the wealth improvement, but it would be at least 90% real estate. It’s a hell of a good yarn, but 3 of the 4 of us work full time off farm and our disposable incomes are no better than our city dwelling cousins, a common scenario I will delve into later.

So I would like to explain how we did this and in doing so show how thousands of other farmers have taken risks and grown their wealth exponentially even making very little profit.

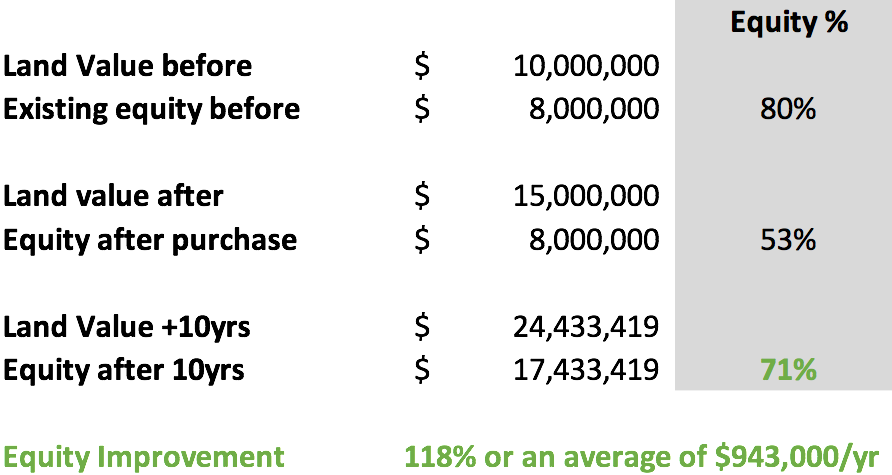

The table above shows the differing level of equity growth starting with 100% equity and 50% equity. The Compound Annual Growth Rate or CAGR is effectively inflation (Australia has averaged a circa 8% CAGR for the last 20 years), our current CPI is 4-6% with a long-term target of 2-3% so I used 5% for the CAGR and a 5% average interest rate on the 50% debt.

There are other variables and the CAGR and interest rates fluctuate, but as you can see the equity percentage growth is double. This is a relatively small number so let’s relate it to real life, a realistic example is you own 1,000 acres with 80% equity, 500 acres comes up next door at the same per acre rate. You borrow another $5 million to buy it and now have $7 million debt and $8 million equity. Over the next 10 years using a 5% CAGR and 5% Interest Only/year on the extra $5 million borrowed this happens

In this calculation the farmer has paid the extra 5% interest per year on $5 million ($250,000/yr). In real life there are other variables, drought, higher interest, commodity prices and they may have to capitalise the interest. Even capitalising the interest for a few years and halving the CAGR the improvement is substantial.

Now ‘Lazy Equity’ is a relatively new term, likely from a Gen X’er like myself who is considering an ‘Arts degree’ to cure a mid-life crisis……but I think you can see what I mean and the link to wealth growth. The pessimists among us would say ‘yes but growth can’t continue like this’……history shows us that whilst not directly correlated to inflation year on year, over a 20-year period land values will continue to increase at minimum the CPI, and most of us can use new technology or management to improve productivity or value as well.

This leads us to discussing why land values have jumped to an historical peak and who is driving this. As shown in various media recently North American pension funds are leading the charge……WHY?……because unlike local funds who require higher liquidity levels, they have a 20 to 50-year investment mindset.

They do their modelling with an IRR (Internal Rate of Return) which is a combination of CAGR and EBIT. An historical CAGR of 5-7% and an EBIT budget of 5-7% they easily hit 10%+ IRR. Its not really our business, but with much of North America domestic borrowing at 2-3% for 30 years I expect their investment debt is substantially lower than the circa 7% we have to pay when buying the neighbours.

It was a ‘tongue in cheek’ as I know most of you aren’t part-time farmers, and regularly work 60 to 80-hour weeks. I would suggest that the ‘other’ side of your business is given more serious consideration and ‘lazy equity’ options considered.

In future articles I will discuss further the millennials and gen X’ers with and without arts degrees, and link it with ‘asset rich and cash poor’ in an attempt to inspire our next generation of pot smoking entitled hippies to take over the farm instead of the Canadians (again perhaps referring to my own situation).