The Grain Rally Farmers Cannot Take at Face Value

The Snapshot

- Wheat markets are being supported by poor crop conditions, with ratings still weak despite a small improvement.

- Energy volatility is feeding into grain markets through higher fuel, freight, fertiliser and biofuel costs.

- India has resumed small wheat exports for the first time in four years, but high local prices should limit any major surge.

- Local feed grain prices have strengthened sharply, especially F1 barley and APW1 across northern and eastern ports.

- The main message for growers is that higher grain prices are helpful, but margins remain under pressure from elevated input costs.

Wheat has again moved to the centre of the grain market story. The latest rally has been built around crop stress, planting delays, energy volatility, freight pressure and a renewed focus on input costs. It is not a simple weather story, although weather remains the starting point.

The key issue is the condition of the US winter wheat crop. Dryness has already affected yield potential across key growing regions, and while rainfall forecasts have eased some concerns, timing matters. Rain can slow deterioration, but it cannot always repair damage already done. That is why the market has remained supported even with some moisture in the outlook.

The crop condition numbers reinforce the point. The good-to-excellent rating only improved from 30pc to 31pc, which remains weak at this stage of the season. Once the market starts to believe yield has been lost, the risk premium tends to stay in place until the crop either stabilises or harvest proves the damage was overestimated.

Energy is the other major influence. Higher crude values flow into fuel, freight, fertiliser and biofuel markets. That matters because grain markets are not just pricing production risk. They are also pricing the cost of growing, moving and replacing grain. Corn and oilseeds have been pulled into the same story, with planting delays adding support in some areas, while stronger biodiesel demand and firm crush margins have helped soybeans.

Trade flows are also shifting. India has started exporting wheat for the first time in four years, with a small shipment being loaded for the United Arab Emirates. This follows the lifting of export restrictions after improved harvest conditions allowed reserves to rebuild. The key point is that this is not expected to become a major supply flood. Higher local prices mean Indian wheat remains relatively expensive against other origins, so the opportunity is likely limited to nearby buyers with urgent short-term requirements. It does, however, show how higher global prices and freight disruption can reopen trade windows that had previously been closed.

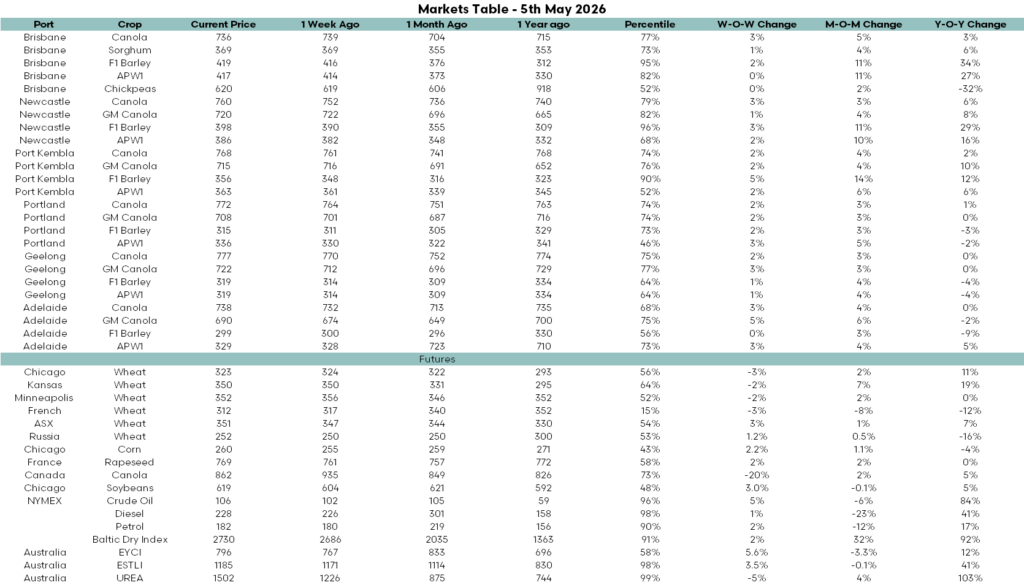

The updated markets table shows how these global themes are feeding into local values. The strongest moves are in northern and eastern feed grain and wheat prices. Brisbane APW1 is at $417, up 11pc over the month and 27pc above last year. Brisbane F1 barley is at $419, also up 11pc over the month and 34pc year on year, placing it in the 95th percentile. Newcastle shows the same pattern, with F1 barley at $398, up 11pc for the month and 29pc above last year, while APW1 is up 10pc over the month and 16pc year on year.

Port Kembla barley has recorded one of the strongest monthly moves, rising 14pc to $356 and sitting in the 90th percentile. This points to a domestic market where feed grain tightness is doing much of the heavy lifting. Canola has also remained firm, although the move has been steadier rather than explosive. Most port values are sitting between $730 and $780, with percentiles generally in the 70s.

The futures section is more mixed. Chicago wheat is up 11pc year on year, Kansas wheat is up 19pc, and ASX wheat is up 7pc, while French and Russian wheat are lower than a year ago. That tells us the wheat story is not uniform, with some markets pricing in more production and logistics risk than others.

The clearest warning in the table is the cost complexity. Crude oil is in the 96th percentile and 84pc higher year on year. Diesel is in the 98th percentile and 41pc higher. The Baltic Dry Index is in the 91st percentile and 92pc above last year. Urea remains the standout at $1,502, sitting in the 99th percentile and 103pc above a year ago.

For growers, this is the important conclusion. Firmer grain prices are welcome, but they are being matched by a much higher cost base. This is not simply a bullish grain story. It is a margin story.