The input spike leaves a long shadow

The Snapshot

The danger for farmers is not just that input prices rise. It is that they rise at exactly the wrong time. When fuel and fertiliser markets move sharply higher, growers are often forced to make decisions under pressure. They do not always have the luxury of waiting for the market to settle. Diesel is needed to keep machinery moving. Fertiliser is needed when the season demands it. If supply feels uncertain, or if prices look like they could rise further, the rational decision is often to secure the product.

That is where the risk of a cost-price squeeze begins to build. Many growers may have already bought diesel and fertiliser near the top of the market. They may have done so not because they wanted to chase higher prices, but because the operating window left them little choice. Once that cost is locked into the business, a later market downturn does not undo the damage. The price on the screen might be lower today, but the farm budget is still carrying yesterday’s higher cost.

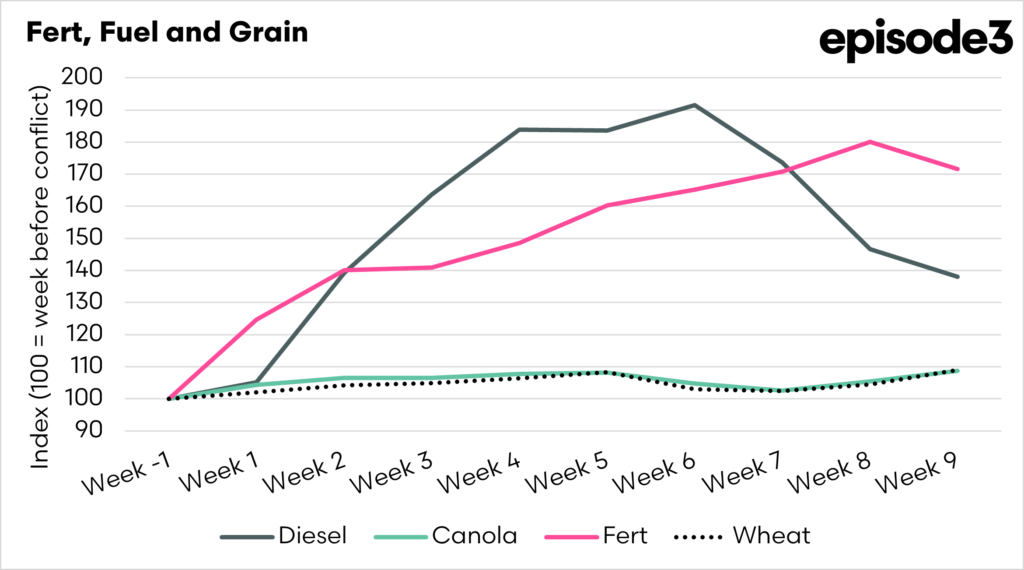

This is where the recent movement in fertiliser, fuel and grain prices matters. Since the pre-conflict base period, diesel spiked to nearly double its starting level before easing back. Fertiliser moved even more persistently higher, climbing to around 80pc above its starting point before softening slightly. By Week 9, diesel had pulled back to around 38pc above the base, while fertiliser was still around 72pc higher.

Wheat and canola have not followed the same path. Both are only around 9pc higher than the pre-conflict level. That is the core problem. The major input lines moved much faster and much further than the grain prices that ultimately drive revenue. The result is a margin squeeze, even in a market where grain prices are higher than they were before the shock.

This is also why easing input prices can be misleading. It may look like the pressure is easing, but that depends on when the product was bought, how much was locked in, and whether farmers still face exposure to lower replacement values. For those who purchased during the spike, the price drop is not a clear benefit. It can actually sharpen the frustration, because the market has moved lower after the money has already been spent.

The risk now is that growers head into the production period with elevated costs already embedded, while grain prices have only offered a modest offset. That does not mean every farm is caught in the same position. Timing, storage, purchasing strategy and seasonal exposure will all matter. But the broad message is clear. A falling input market does not automatically remove the squeeze. For many farmers, the squeeze was created by having to buy.