The return of the frying Scotsman

The Snapshot

- Canola prices in Australia have been high since mid-2021.

- This has caused vegetable oil prices for consumers/fast food retailers to increase dramatically.

- In reality, farmers in 2022 are likely to see margins potentially poorer than in 2021, as they combat high input costs and declining output prices.

- Consumer pricing levels may reduce as the canola prices decline.

- Palm oil prices have crashed during the past two months. As one of the world’s most important oils, this has a flow effect on canola.

The Detail

Late last year, I wrote a piece ‘The Frying Scotsman‘. This article discussed the rising oilseed prices around the world and why this would start to be reflected in the cost of frying our fish and chips.

This is clearly a major concern to all consumers. The new ABS stats have raised this issue again, and it seems to be getting some more traction as fish and chippers discuss the large rises in price for vegetable oils.

Let’s look into it.

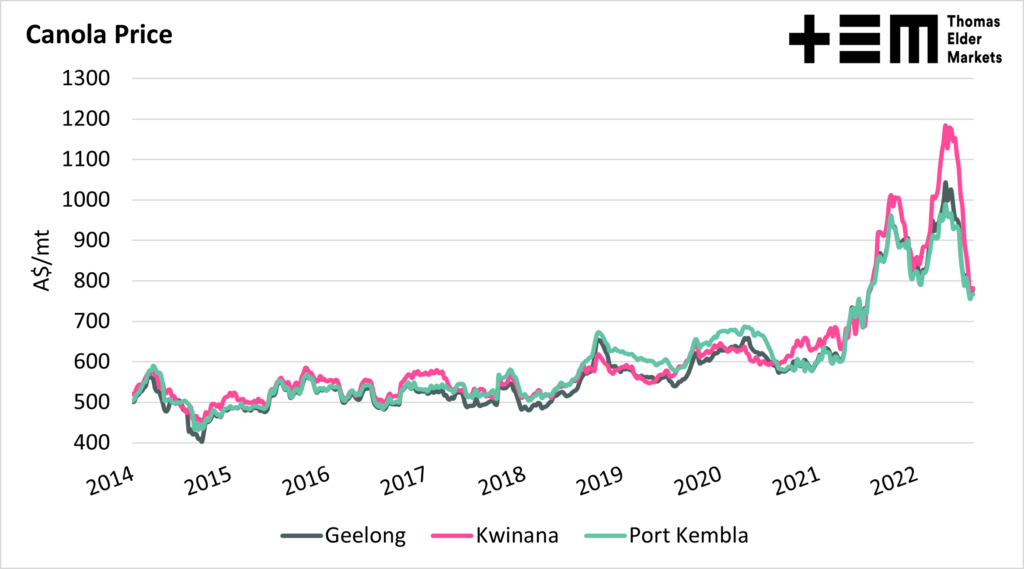

Firstly, let’s look at the spot price of canola. If we look at canola prices in recent years, we can see that since April last year, prices have been pushed through the roof. Firstly by the loss of Canada through their drought, and then issues with both Ukrainian sunflower and Indonesian palm.

Whilst there are complaints that vegetable oil prices have significantly risen at the consumer level, the reality is that canola prices have dropped significantly during the past two months.

It is important to note that there is a long supply chain for vegetable oils, therefore, the prices being paid by consumers and fast food retailers will likely reflect the input price of canola (or others) from months ago. This is some solace for these buyers, as likely they will see lower prices reflected in their oil in the future.

It’s not much good for grain growers who held onto volume.

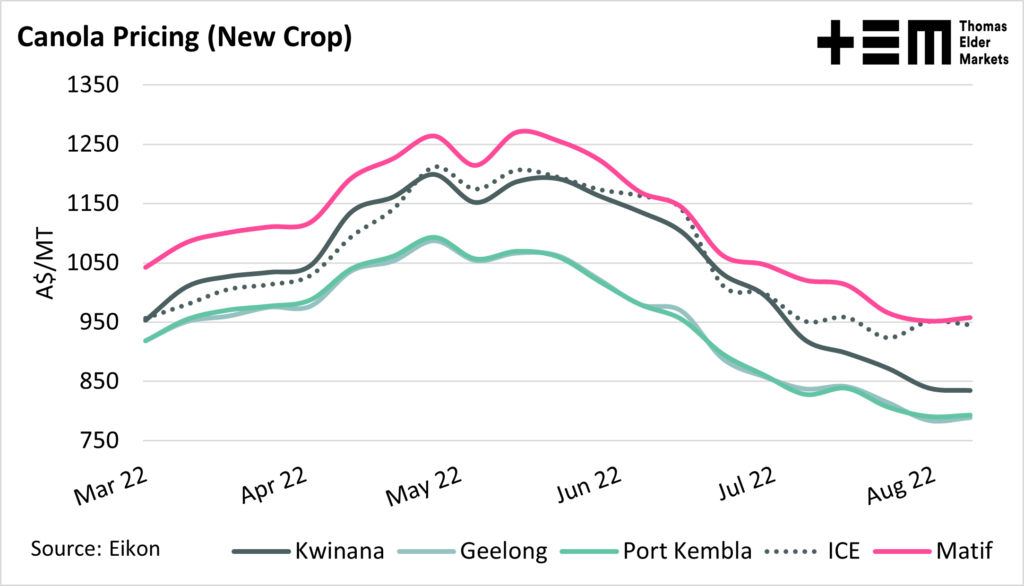

The prospect for new crop is also not promising. The new crop bids for harvest have also come under major pressure over the past two months.

One of the major concerns I have had this season is the cost price squeeze. We heard arguments that because fertilizer prices were high this meant that grain/oilseed prices had to remain high. This isn’t the case, as outlined in ‘Buy High, Sell Low‘.

Unfortunately, this is starting to occur. The majority of farmers have paid for their inputs upfront at high pricing levels. This would have worked if grain/oilseed prices remained high. Unfortunately, they declined, and not many farmers participated in the higher prices achieved during the peaks in May.

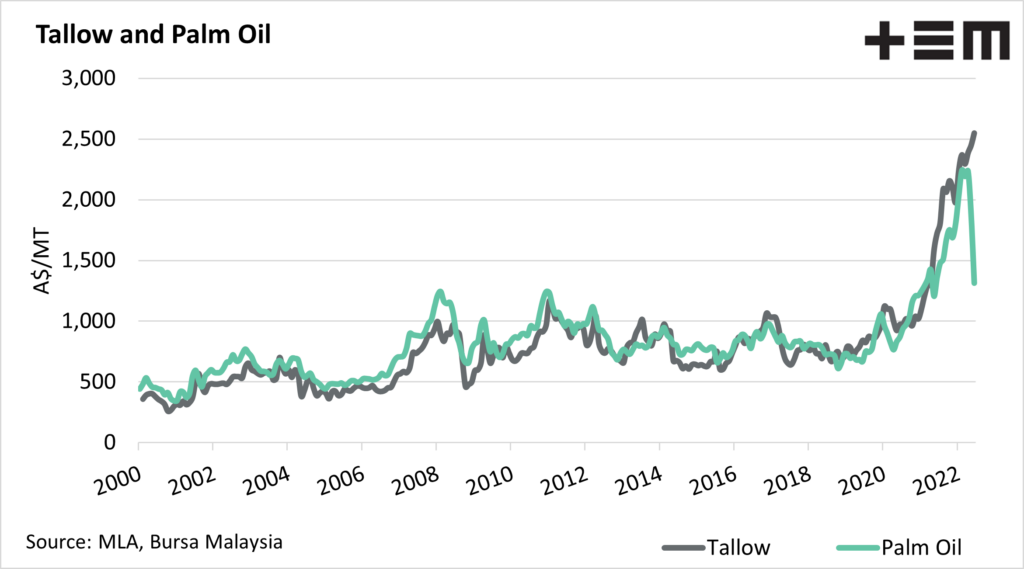

Tallow is an alternative to vegetable oils, which can make a much more tasty chip. Tallow prices tend to have a strong correlation with palm oil.

In recent months tallow has continued to rise, but palm oil has been smashed. Indonesia, the world’s largest palm exporter, banned the export of veg oils in April (see here) to reduce the domestic price and food inflation.

Even when well intended, government intervention in markets tends to have negative consequences. The reality is that Indonesia couldn’t afford to maintain a ban on it’s most significant export commodity. The export ban caused a supply glut caused by uncertainty and the removal of the export market.

The palm price has now crashed as they reopened the market.