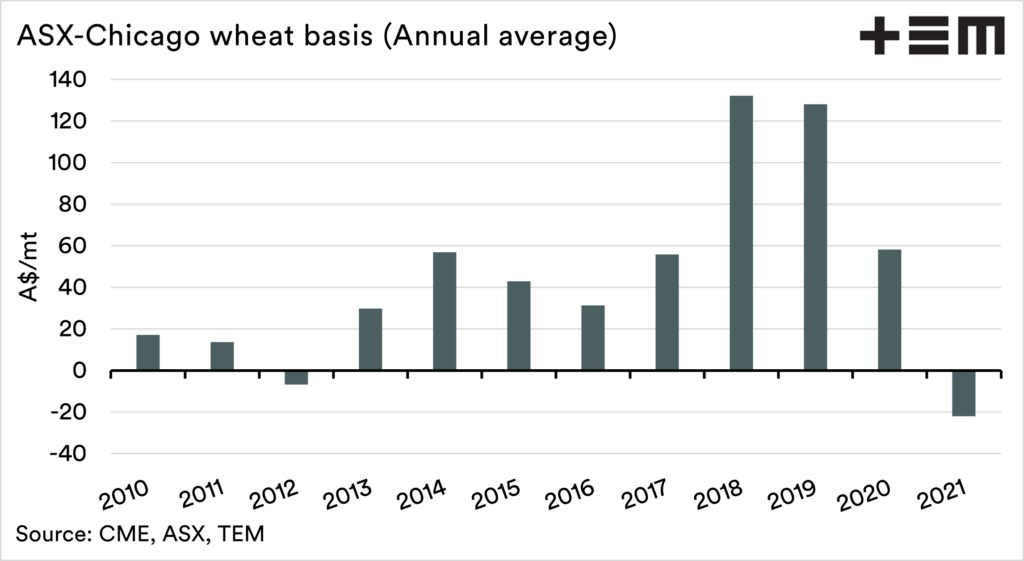

Unusually big discount for Australian wheat in 2021.

The Snapshot

- Basis sunk to low levels in 2021.

- This meant that Australian wheat pricing levels were heavily discounted to overseas values.

- Basis is generally driven by supply. Higher supply = lower basis (and vice versa).

- Two years of solid production are the main reasons for the discount.

- Buyers know they have access to grain. Therefore they have no FOMO (Fear of missing out).

- We do not know how this year will pan out, whether it will be boom or bust or somewhere in between.

The Detail

Basis isn’t the be-all and end-all of pricing grain. However, it is an important part of the overall picture. The basis lets us know if we are receiving a premium or a discount for your wheat. To get the most of your grain marketing, it is important to understand the concept of basis.

As we start the new year, I thought it might be worthwhile doing a quick update on basis for last year.

Let’s jump into it.

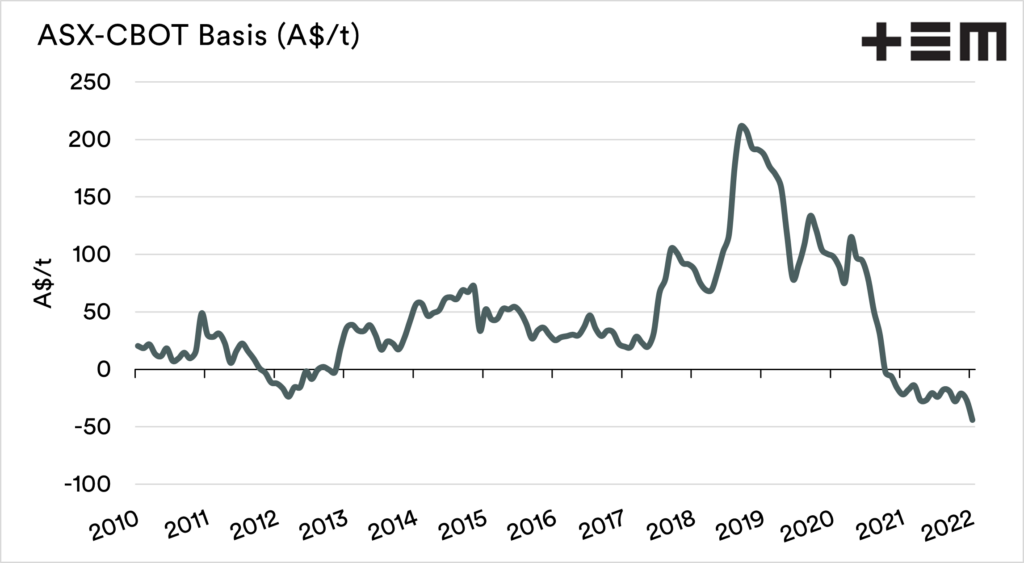

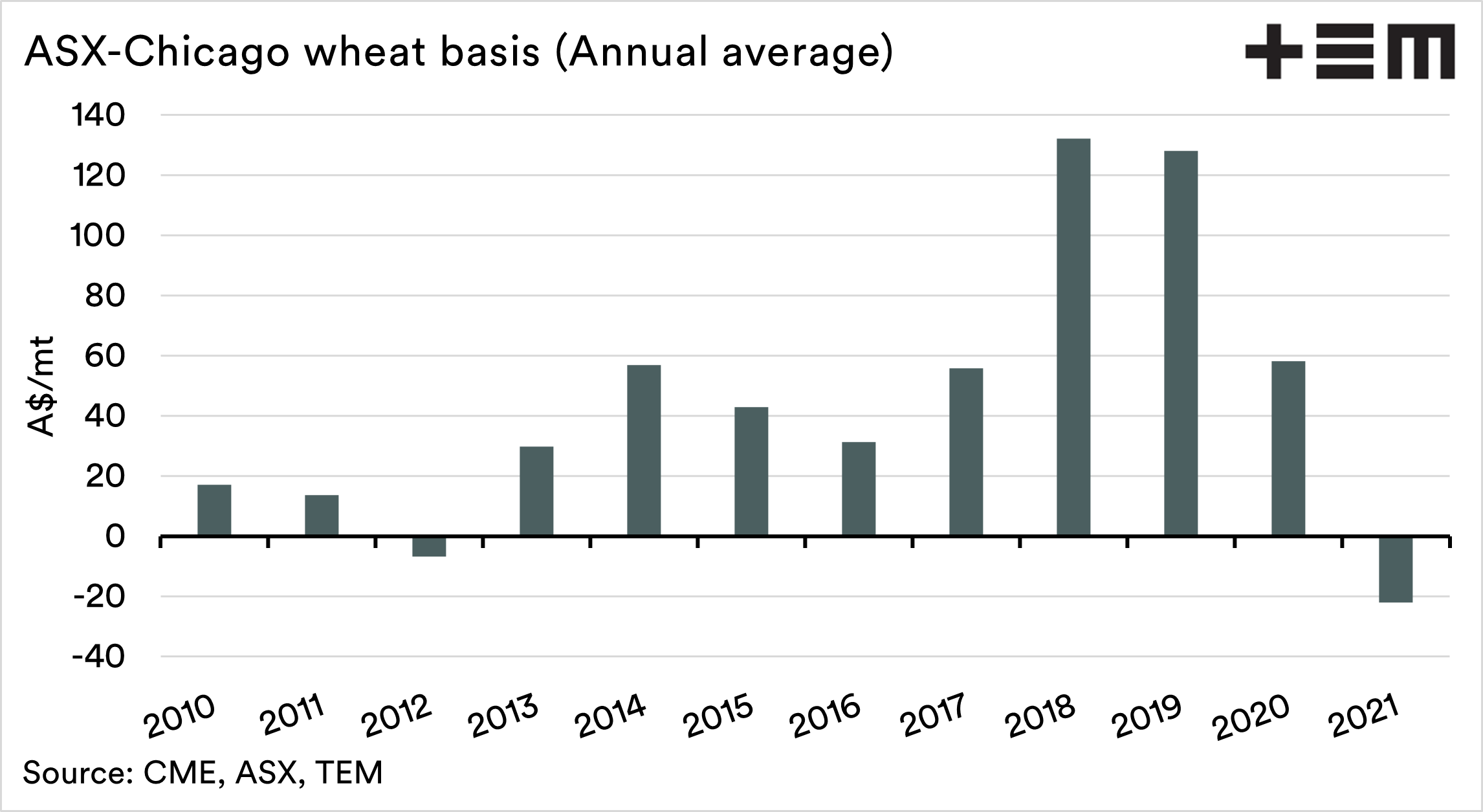

The chart below shows the basis between the ASX wheat contract and CBOT wheat on an annual basis since 2010. I have used the ASX as it reasonably represents Australian wheat pricing.

We can see from this chart that there have only been two years in this period where the average basis level has been negative – 2012 and 2021. The discount in 2021 was substantially larger than previously experienced.

A discount was not unexpected, due to two large crops in a row. The 2018 and 2019 period was a time of drought, resulting in large premiums vs Chicago due to local deficits.

On the range

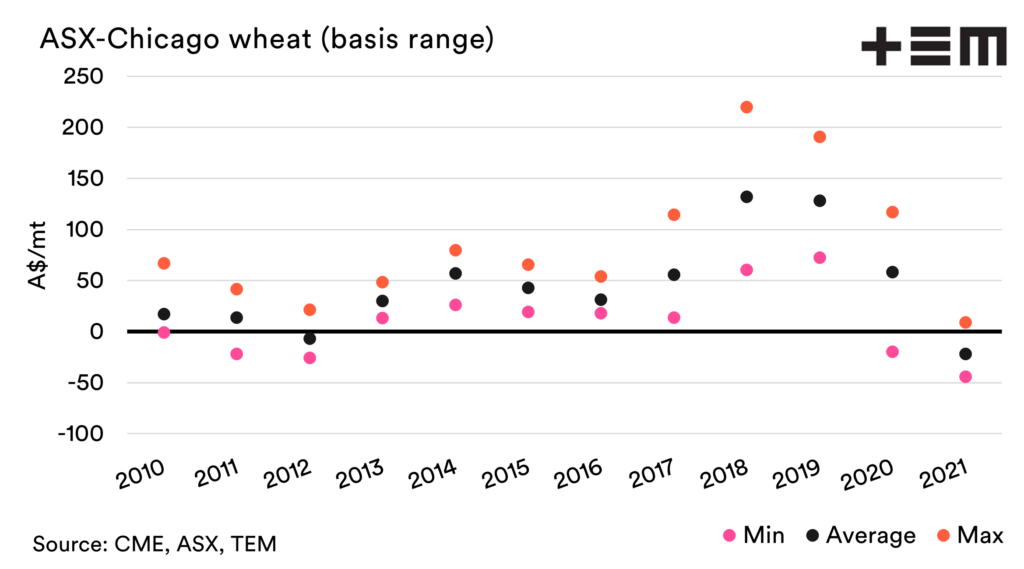

What about the range? The chart below shows the minimum, average and maximum basis for each year. In the majority of years, the difference between the max and minimum is relatively tight. The exceptions appear to be around years with more distressing production prospects.

This chart provides a good visual of how bad the basis level got to at its worst during 2021.

Not all are created equal.

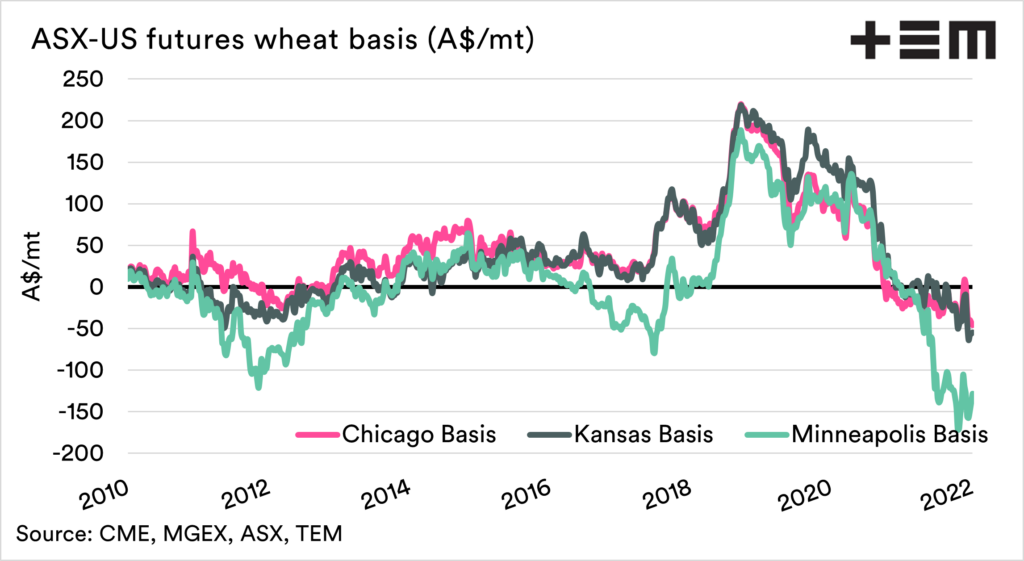

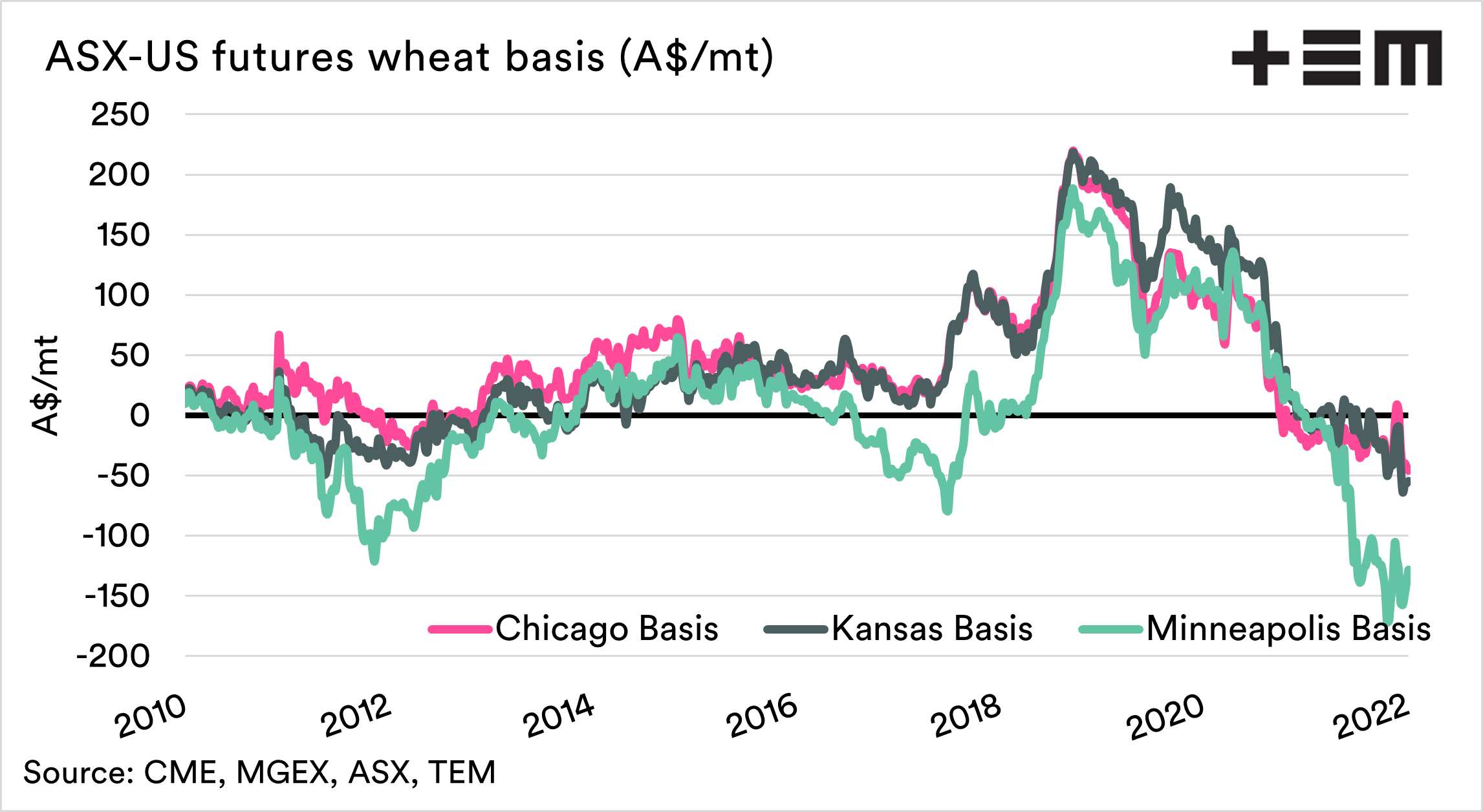

The US has different futures contracts for different qualities of wheat. The chart below shows our basis to the three futures contracts. One of the stark points is the discount on Minneapolis wheat (spring wheat).

Minneapolis has such a strong premium due to the localised drought issues, something we point out would occur in May/June updates last year (see here & here).

The Minneapolis premium will erode back to more normal levels when production in the Northern US/Canada becomes more assured.

Where to from here?

The basis level between Australian pricing and overseas futures is largely driven by supply. A low supply in Australia will lead to a higher basis; an increased supply environment results in Australian pricing being discounted.

We have had two great years in Australia. This has led to discounts growing. As we move through 2022, we have no idea what the crop will be like at the end of the year, but we are likely to have large stocks left over by the end of the year.

If we move back to more average production, then we will then see the basis return to more normal levels.