Sheepmeat export update March 2026

March 2026 - Sheep Meat Export Update

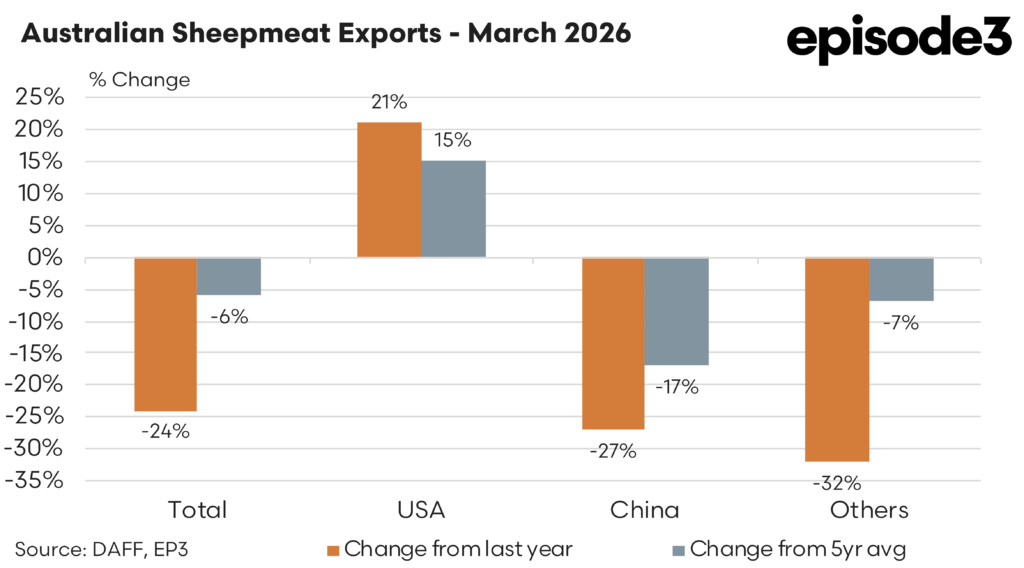

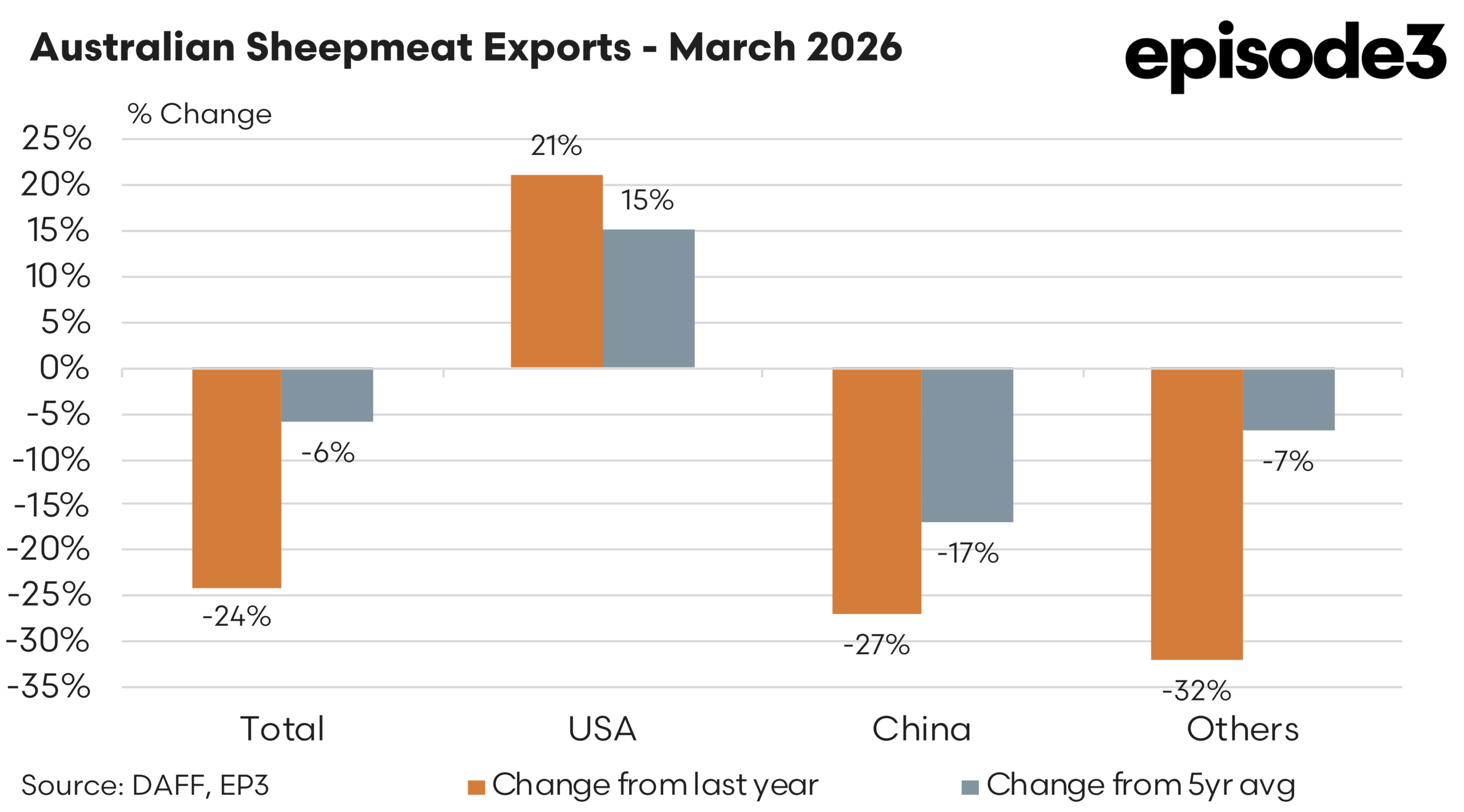

Australian sheep meat export flows softened in March 2026, with total combined lamb and mutton shipments reaching 42,656 tonnes, down 24 percent year on year and sitting 6pc below the five year average.

The pullback in total volumes marks a clear shift from the stronger export pace seen earlier in the year and reflects a combination of softer demand across several markets and a pronounced contraction in shipments to the Middle East and North Africa region. While global demand remains broadly intact, the March result highlights the sensitivity of sheep meat trade flows to changes in access and regional buying activity.

The United States was the standout performer in March, continuing to absorb a growing share of Australian sheep meat exports. Shipments reached 8,825 tonnes, up 21pc on last year and 15pc above the five year average. This sustained growth reinforces the structural expansion of the US market, particularly for higher value lamb cuts, and reflects strong underlying consumer demand supported by limited domestic supply. The US is increasingly acting as a stabilising force within the export mix, offsetting weakness in other regions and providing a consistent outlet for Australian product.

In contrast, exports to China softened materially through March. Volumes totalled 9,513 tonnes, down 27pc year on year and 17pc below the five year average. This decline suggests a moderation in buying activity following a strong start to the year, with China remaining a key volume market but exhibiting more variability in monthly demand. Despite the pullback, China still accounted for the largest single country destination in March, underlining its ongoing importance within the export portfolio even as conditions fluctuate.

The most significant shift in March occurred across the ‘other markets’ category, where exports fell sharply to 24,317 tonnes, down 32pc year on year and 7pc below the five year average.

Looking at the broader composition of the export market provides additional context. China accounted for around 19 percent of Australia’s sheepmeat exports, while the United States represented roughly 18 percent of total shipments. The Middle East and North Africa region continues to play a major role as well, absorbing around 17 percent of exports, while other Asian markets collectively account for roughly 14 percent. The remaining third of the trade is spread across a variety of smaller markets.

That diversified export structure has become increasingly important for the industry. While China and the United States remain the two largest individual buyers, a significant share of Australian sheepmeat now moves into a wide range of secondary markets. This breadth of demand provides a degree of resilience when conditions soften in any single destination.

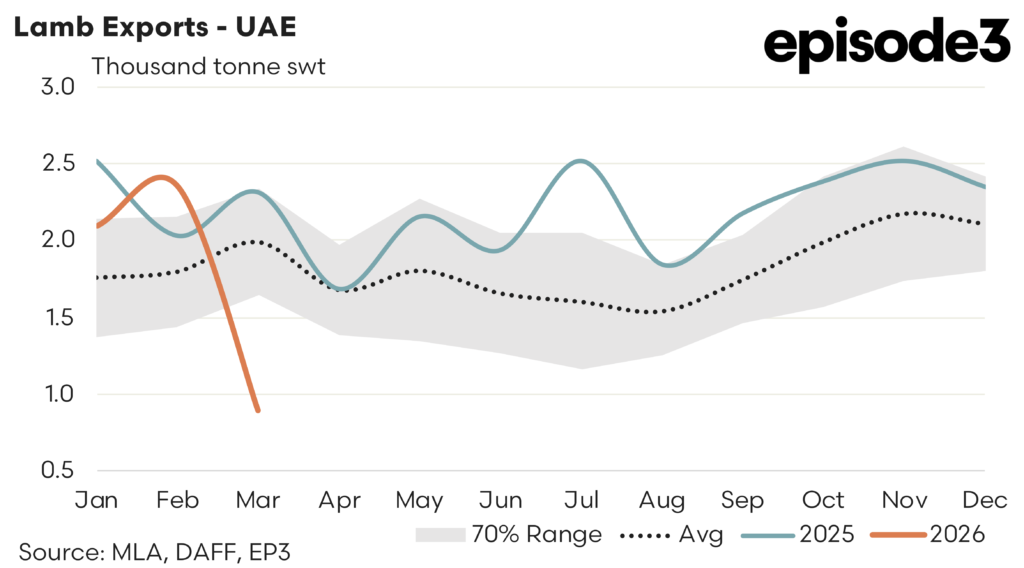

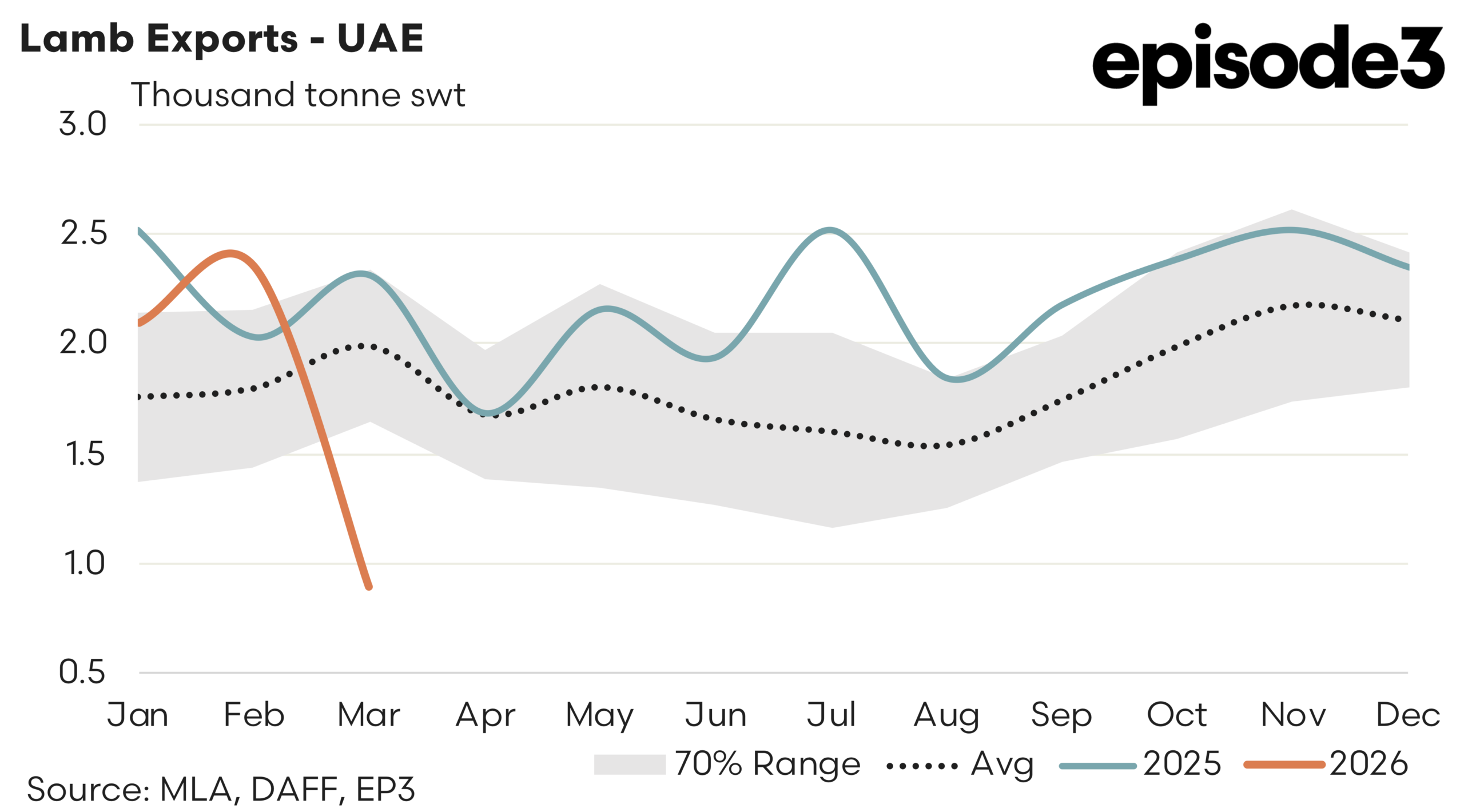

Much of this decline was driven by a steep reduction in flows to the Middle East and North Africa region. Lamb exports to the United Arab Emirates were 55pc below the five year average for March, while Qatar also recorded a 55pc decline and Jordan was down 44pc. There were no lamb shipments to Bahrain during the month. Mutton flows showed a similar pattern, with exports to Saudi Arabia down 49pc on the five year average, Oman down 87pc and Kuwait down 25pc.

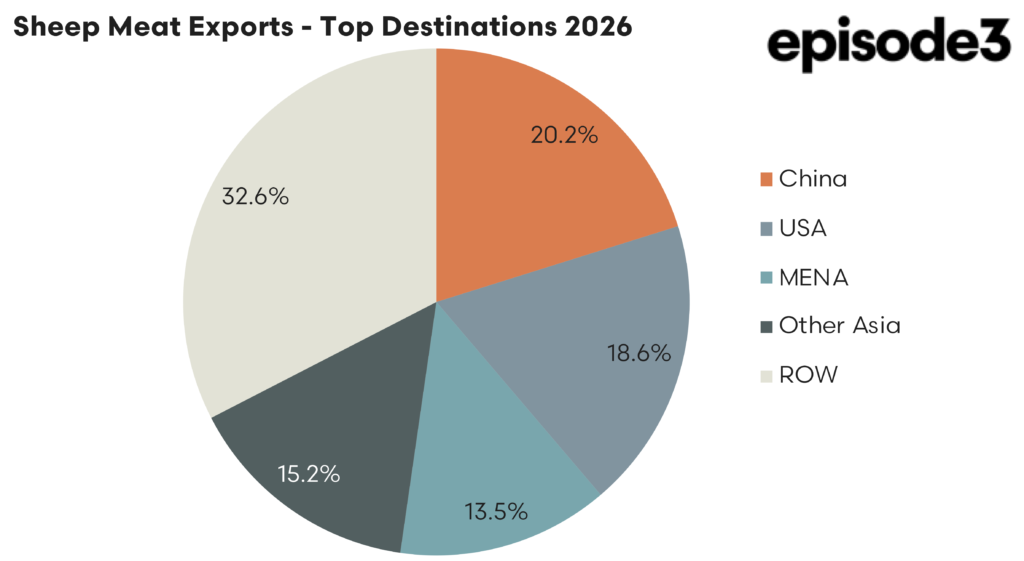

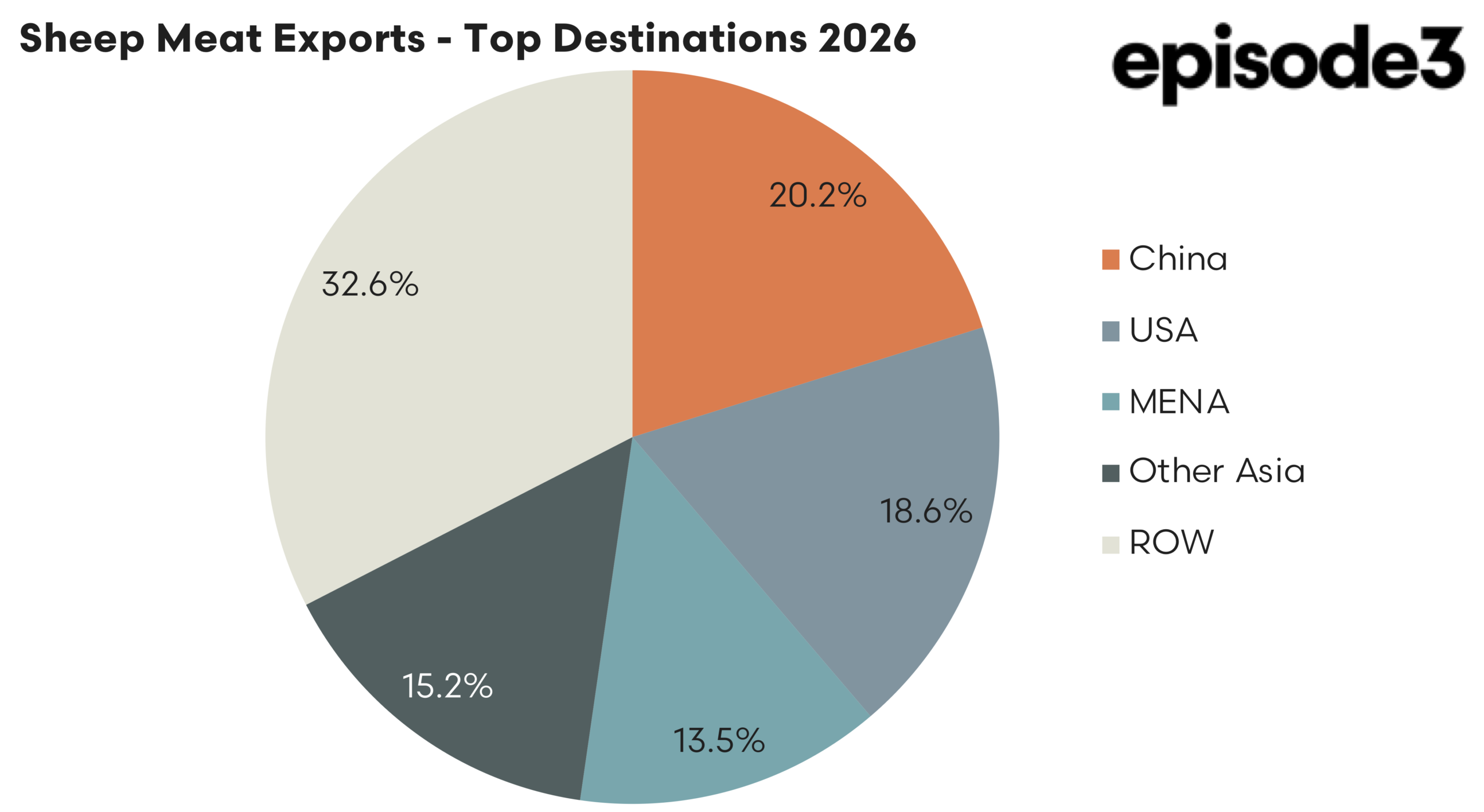

These declines point to a broad based contraction in the region rather than an isolated market disruption, suggesting that access constraints and reduced buying activity have materially impacted trade flows. This shift is also reflected in the changing distribution of export market share. Just one month earlier, the MENA region accounted for 17pc of total sheep meat exports. By March, that share had declined to around 13.5pc, indicating a meaningful redistribution of product toward other regions.

At the same time, China and the United States have maintained relatively balanced shares at 20.2pc and 18.6pc respectively, while other Asian markets continue to hold a steady portion of the export mix. The overall distribution remains relatively even across major destinations, but the reduction in MENA participation has altered the balance at the margin.

The March data highlights a market in transition. While total export volumes have eased, underlying demand in key markets such as the United States remains strong and continues to provide support. However, the sharp contraction in MENA trade flows has exposed the importance of regional diversification and the impact that access constraints can have on overall export performance. As the year progresses, the extent to which MENA demand recovers will be a key factor in determining whether total sheep meat exports can return to the elevated levels seen earlier in 2026.