Supply squeeze sets in as slaughter slips

Market Morsel

The latest slaughter data from March to April confirms that sheep supply continues to tighten across all major producing regions, while lamb throughput is now also beginning to ease in most parts of the country. This shift marks a further move away from the earlier seasonal flush and reinforces that the supply cycle is transitioning into a more constrained phase.

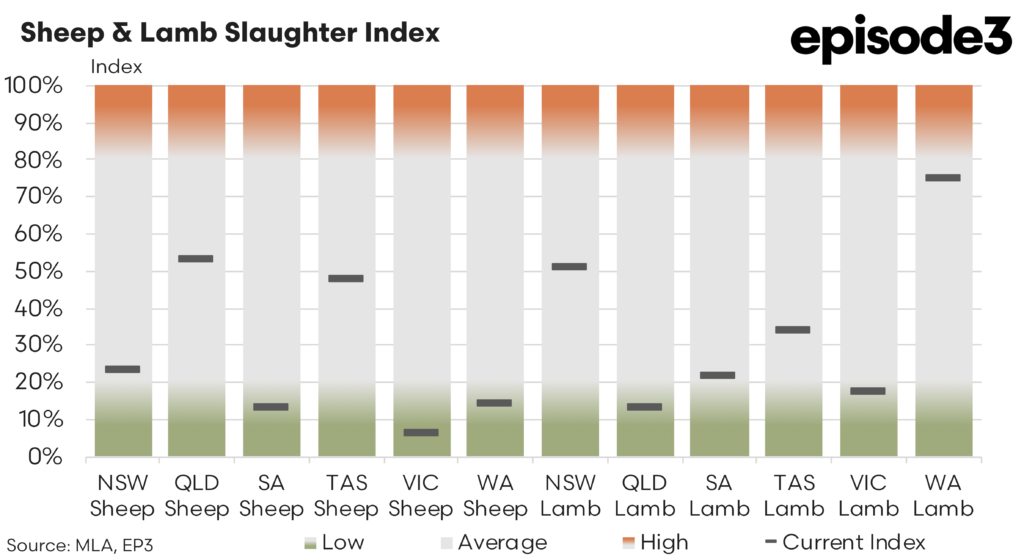

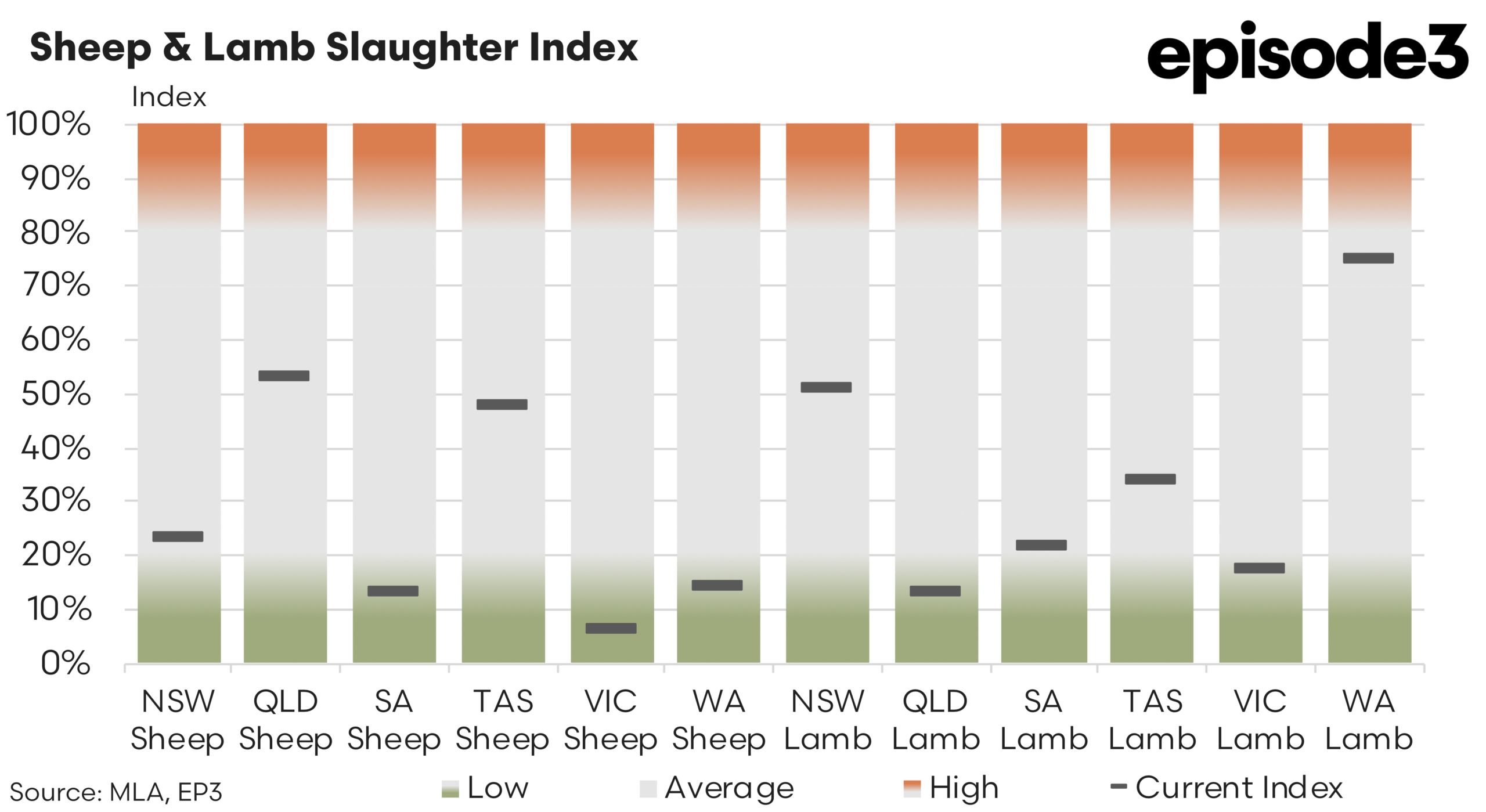

Sheep slaughter trends show a consistent decline across every state, highlighting the broad based nature of the tightening. New South Wales edged lower from 24pc in March to 23pc in April, which on its own appears modest but continues the steady downward trend seen over recent months. Victoria recorded a more pronounced contraction, falling from 14pc to just 6pc, indicating a sharp reduction in available sheep and reinforcing the tight conditions already evident in the southern mainland.

Western Australia also declined meaningfully, dropping from 22pc to 14pc, which points to a continued drawdown in supply following earlier processing strength. Tasmania eased from 53pc to 48pc, suggesting that the earlier uplift in throughput has begun to fade as availability tightens. South Australia remains one of the tightest regions in the country, falling from 18pc to 13pc and continuing to operate well below typical seasonal levels.

Queensland, which had previously been the outlier with stronger sheep flows, also moved lower, declining from 75pc to 53pc, signalling that northern supply is now aligning more closely with the tightening seen elsewhere.

The sheep slaughter data presents a clear and consistent picture of declining availability across the entire country. This broad based contraction suggests that the earlier pull forward of stock has now largely worked through the system, leaving processors with fewer animals to maintain previous kill levels. While sheep supply is tightening across all regions, lamb slaughter trends are more varied but still point toward an overall easing in throughput.

New South Wales lamb slaughter dropped significantly from 70pc in March to 51pc in April, indicating that the earlier wave of lamb supply is now beginning to taper off. Queensland also recorded a decline, falling from 23pc to 13pc, which suggests that northern lamb availability has tightened after a period of moderate supply.

South Australia saw one of the sharper contractions, dropping from 43pc to 22pc, reinforcing that much of the earlier lamb supply in the state has already been processed. Victoria followed a similar direction, easing from 25pc to 17pc, which points to a continued moderation in throughput in one of the key producing states.

In contrast to these declines, Tasmania recorded a notable increase, lifting from 18pc to 34pc, indicating a regional uplift in lamb availability. Western Australia also remained strong, edging higher from 73pc to 75pc, confirming that it continues to be the standout region for lamb supply at present.

Despite these regional increases, the overall national trend for lamb is one of softening throughput, particularly across the eastern states. The divergence between regions highlights the uneven nature of the current supply cycle, with some areas still moving through residual supply while others have already tightened significantly.

The combined sheep and lamb slaughter data points to a market that is clearly moving further away from the earlier seasonal flush. Sheep supply has tightened rapidly and consistently across all regions, while lamb supply is now following a similar path, albeit with greater regional variability.

This shift in supply dynamics has important implications for pricing and processor behaviour in the coming weeks. With fewer sheep available, competition for mutton is likely to remain firm, particularly as processors seek to maintain throughput in the face of declining numbers. The continued easing in lamb slaughter across several key states suggests that the pool of available animals is no longer expanding and may begin to contract more noticeably as autumn progresses.

At the same time, the strength in Western Australia and the uplift in Tasmania indicate that supply has not yet tightened uniformly, which may temper the pace of any price increases in the short term. However, as these regional pockets of availability begin to ease, the broader tightening trend is likely to become more pronounced at a national level.

The transition now underway reflects the natural progression of the seasonal cycle, where the spring and early summer flush gives way to reduced availability as the year advances. As the market moves deeper into autumn, these supply constraints are likely to play an increasingly important role in shaping price direction and processor margins.