Barley bonanza back on for Australia?

The Snapshot

- China announced that it was removing the barley tariff on Australian barley.

- CBH may still be restricted from exporting barley to China.

- The price of barley improved as a result of the expected tariff removal.

- Our price of barley relative to other origins has been discounted since the start of the tariff.

The Detail

China was due to come back with the conclusion of its internal review of the anti-dumping tariffs placed upon Australian barley this week. They announced their decision a week early: to remove the tariffs as of Saturday morning. You can read the announcement here.

We briefly spoke about the barley tariff on our hobby podcast ‘Agwatchers’ which can be listened to here.

There are many in the industry, analysts included, who have commented that the impact of the barley tariff on Australian farmers has been minimal. It has not been minimal; it has been considerable.

The four articles below are examples of some of the pieces we have covered, the impact and opportunity for China.

- The two-year review of the Chinese ‘Ban’ on Aussie Barley

- How much did the Chinese barley tariff cost?

- Market Morsel: China is the opportunity for barley

- Should a trade deal faze Australia? The origin of the barley tariff?

So how did the market react?

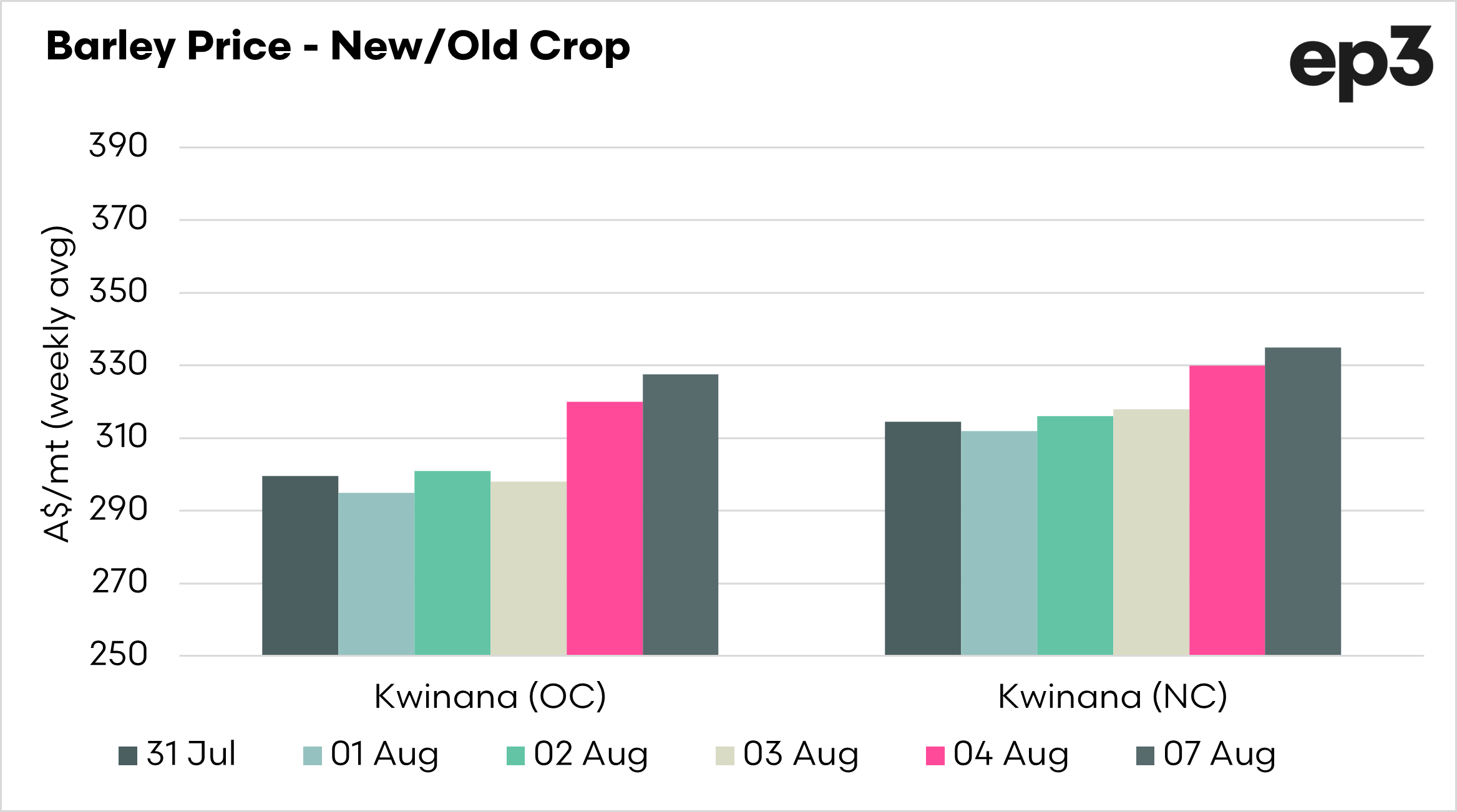

The first chart below shows the past week of pricing. We can see a considerable jump in barley values for Kwinana. Western Australia is where the majority of exports of barley will come from.

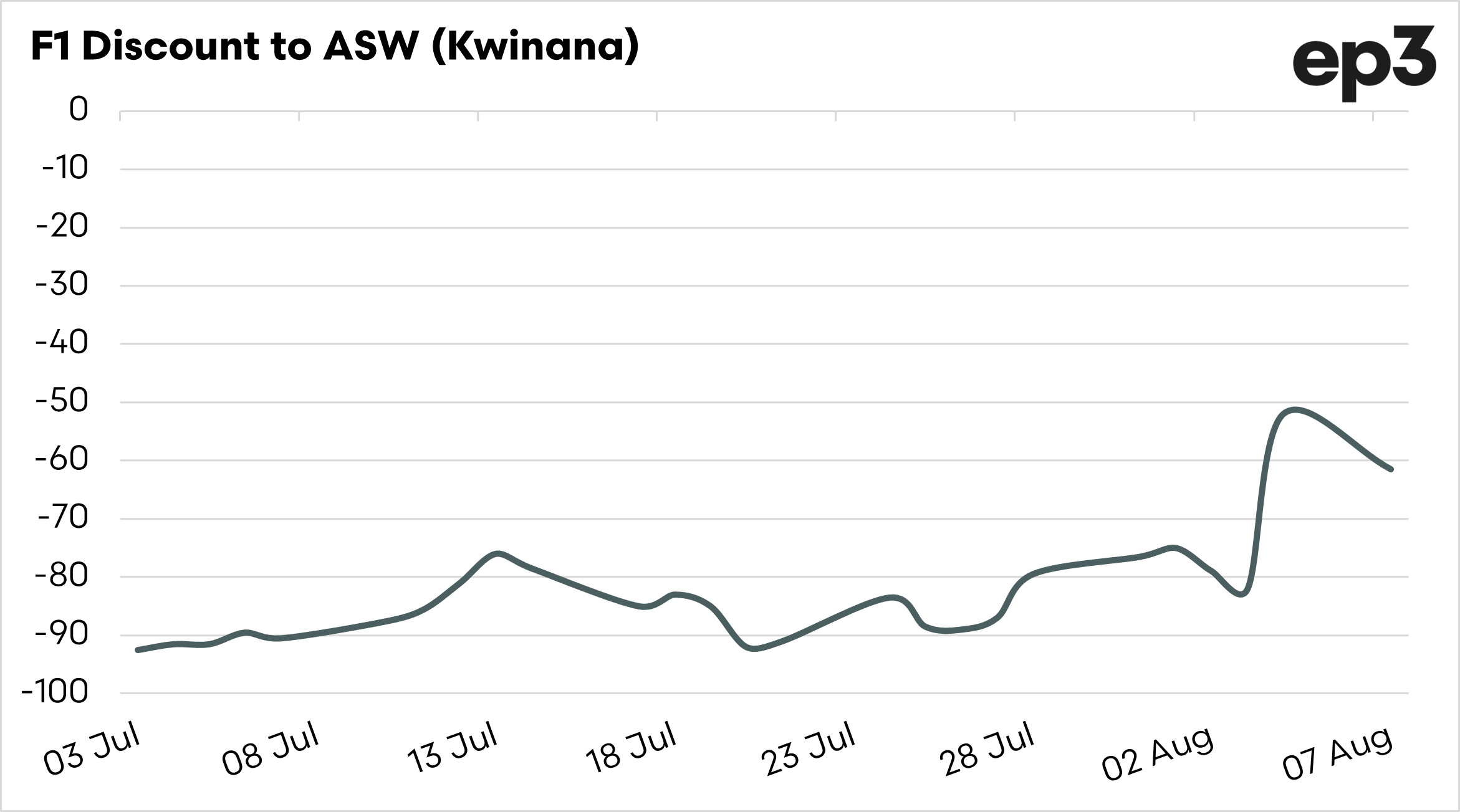

The benefit can be seen immediately in the chart below, which displays the F1 discount to ASW over the past month. The discount has narrowed. Feed barley has a discount to feeding wheat in a rotation, as it is nutritionally poorer.

As barley gets more expensive and anecdotally moves back closer to a A$35 discount (from my experience with pigs), then wheat inclusion in rations is likely to increase. The removal of the barley tariff can have an impact on the domestic demand for wheat in Australia.

We look at the F1 discount to ASW as one of the indicators of the value lost in the barley industry since the start of the tariff introduction.

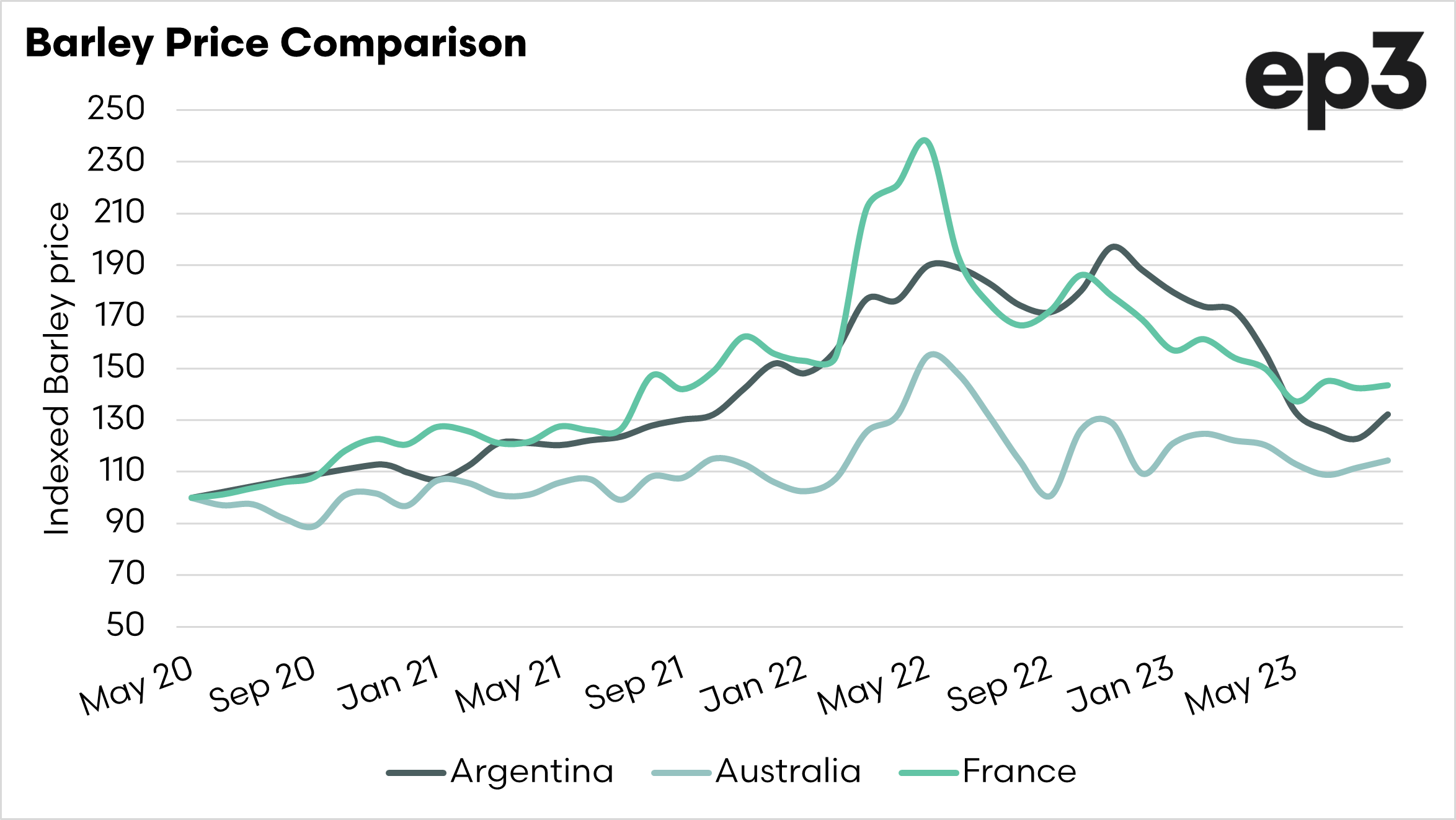

This third chart displays an index of barley pricing (feed) which commences the month of the introduction of the tariff. We can see that Australian barley has been discounted against Argentinan and French barley.

These are two nations that had been direct beneficiaries of the loss of Australian barley into China. In the coming weeks and months, it will be interesting to see whether these pricing levels move closer to the level seen in our competitors.

The question will be whether they drop to meet us or we rise to meet them. Let’s hope it’s the latter.

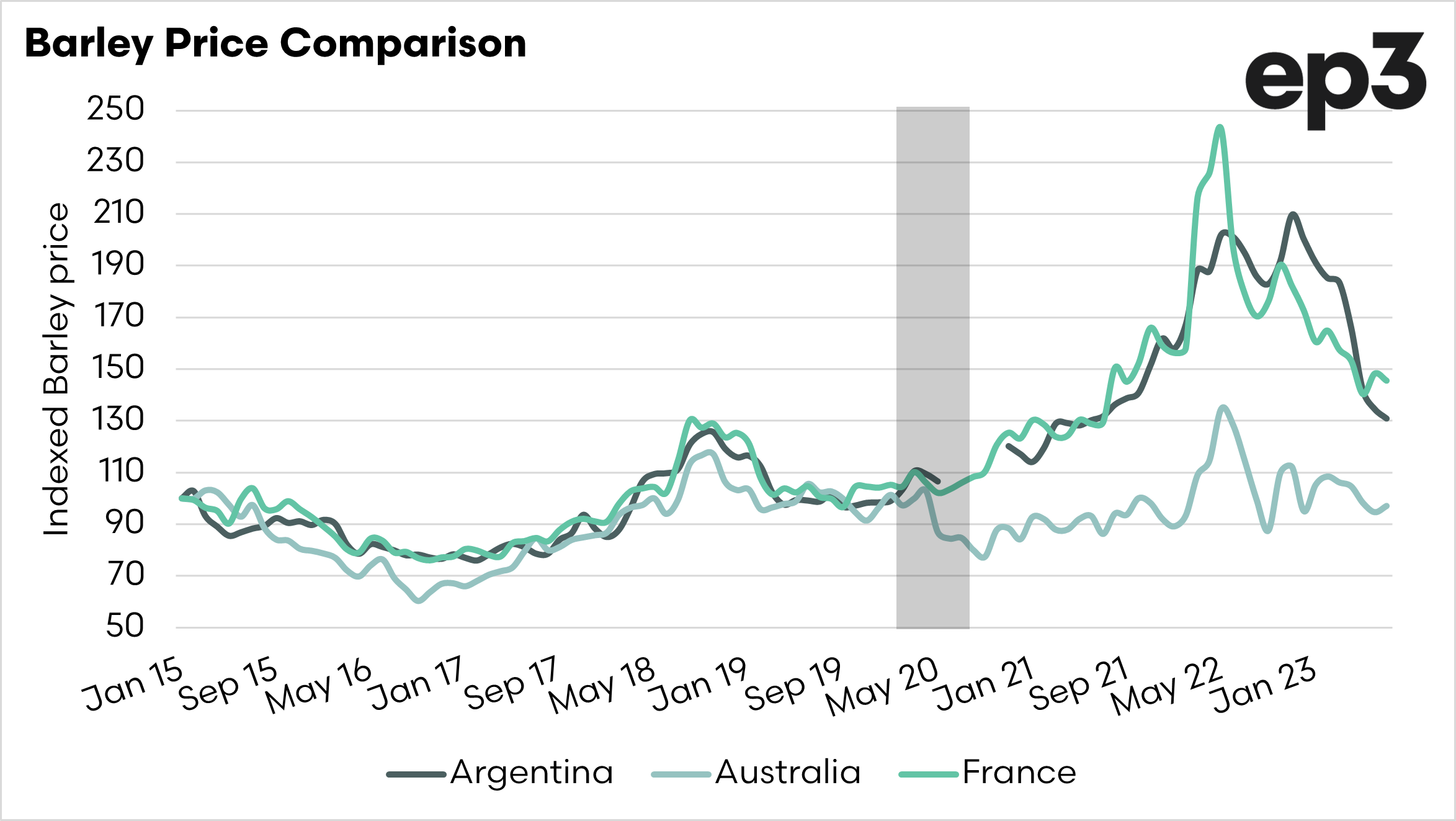

The chart below looks at the same nations but commencing back in 2015. Australia tended to be much closer in pricing level than Argentina and France.

I have highlighted May 2020, the month in which the tariff was introdcued. There was an immediate drop in relative value between Australian barley and these two nations. This discount has persisted.

There could be arguments that this is due to our large crops. This is true; we would likely have seen discounts. The discount would have been smaller.

So what does it mean?

Australian barley will start flowing back into China (possibly with the exception of CBH). There has been much talk about Australia diversifying away from China and that we have won new markets.

My points on diversification, which I have talked endlessly about:

- We diversified our markets because we didn’t have a choice.

- We were also cheap compared to our competitors.

- Australia doesn’t trade any grain. Trading companies do.

- Trading companies will run their own risk profiles and decide how much to trade with China.

- Traders aren’t charities. Much like growers, they will sell to the highest bidder.

- China will be our biggest buyer of barley.

The end of the barley tariff is good news for barley producers, especially for malt barley. It will be interesting to see whether this thawing translates to better outcomes for meat and wine.