Rock up for the cheapest grain in the world.

The Snapshot

- Cost and freight matrixes provide an insight into our relative pricing compared to our competitors.

- We need to be competitive to ship our grain, but not overly.

- Our grain prices are cheapest in the world, and are pricing competitively.

- The price received by the grower is attractive, due to the overall market rising.

- Price are heavily discounted to the rest of the world.

- We can see that in our pricing comparison to both futures, and through our relative cost and freight pricing to our customers.

The Detail

A month ago, I wrote about our competitiveness on barley (see here). I thought it was time to take a look at our competitiveness for other commodities.

The purpose of this analysis is to determine our pricing relative to other competing nations. In partnership with our friends at AgFlow, we are charting the cost and freight to some popular destinations. This is in reverse to our fertilizer modelling, which is used to shine some light on Australian Urea/Dap pricing (see here).

This provides an overview of how competitive we are with our customers.

Why is it important? We need to be competitive to get our grain out of the country and to our customers, but we don’t need to be over-competitive. Wheat on a global level is largely undifferentiated; price is what wins tenders.

Our cost and freights for Australia are based on a grower bid. Therefore they don’t take into account margins and are intended merely to give an idea of the trend.

So let’s dive in and take a look.

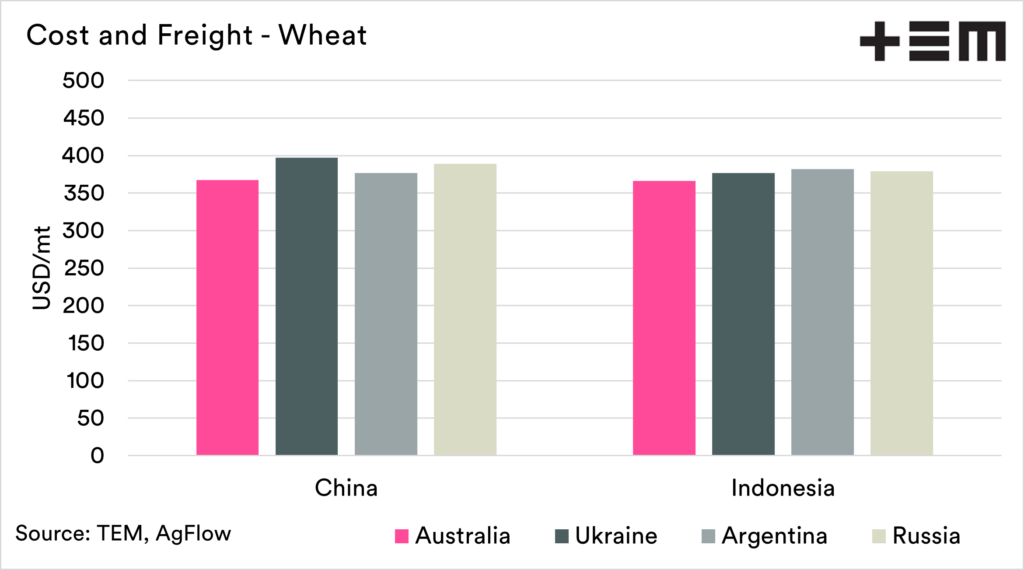

Wheat

We had a great 2020 season, and until the rains, we were having a great 2021. Two big crops in a row have given us a surplus of production. The result has been that Australian wheat pricing has become the most competitive in the world.

It is important to note that Russia at present is saddled with export taxes, which are not taken into account in these charts, so they are far more uncompetitive than these numbers suggest.

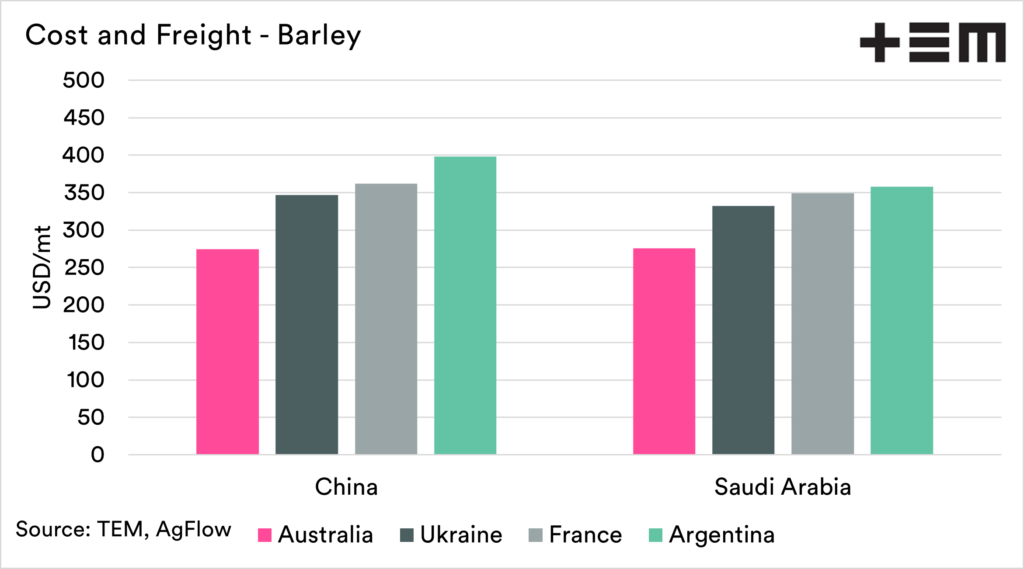

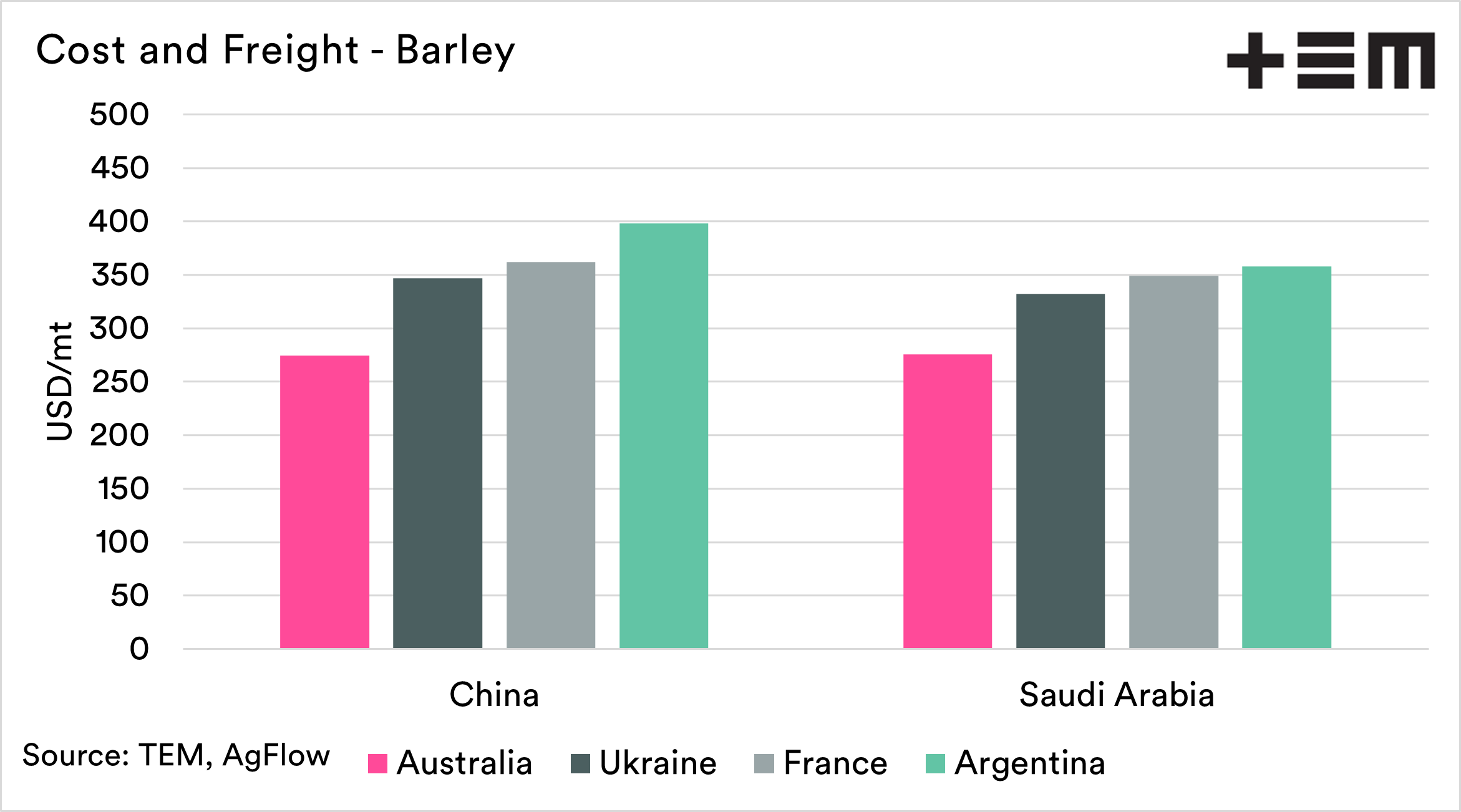

Barley

Our barley pricing is still stuffed. The Chinese tariff has reduced our available avenues to ship to. Whilst growers are receiving a number that is historically quite attractive; the reality is that we are still pricing at levels that are quite low.

Conversely, our friends in China are now paying substantially more than they would have been by locking out one of the worlds largest barley exporters.

So if people tell you that gap left by China hasn’t impacted us, I can give them a number of different charts showing that not to be the case.

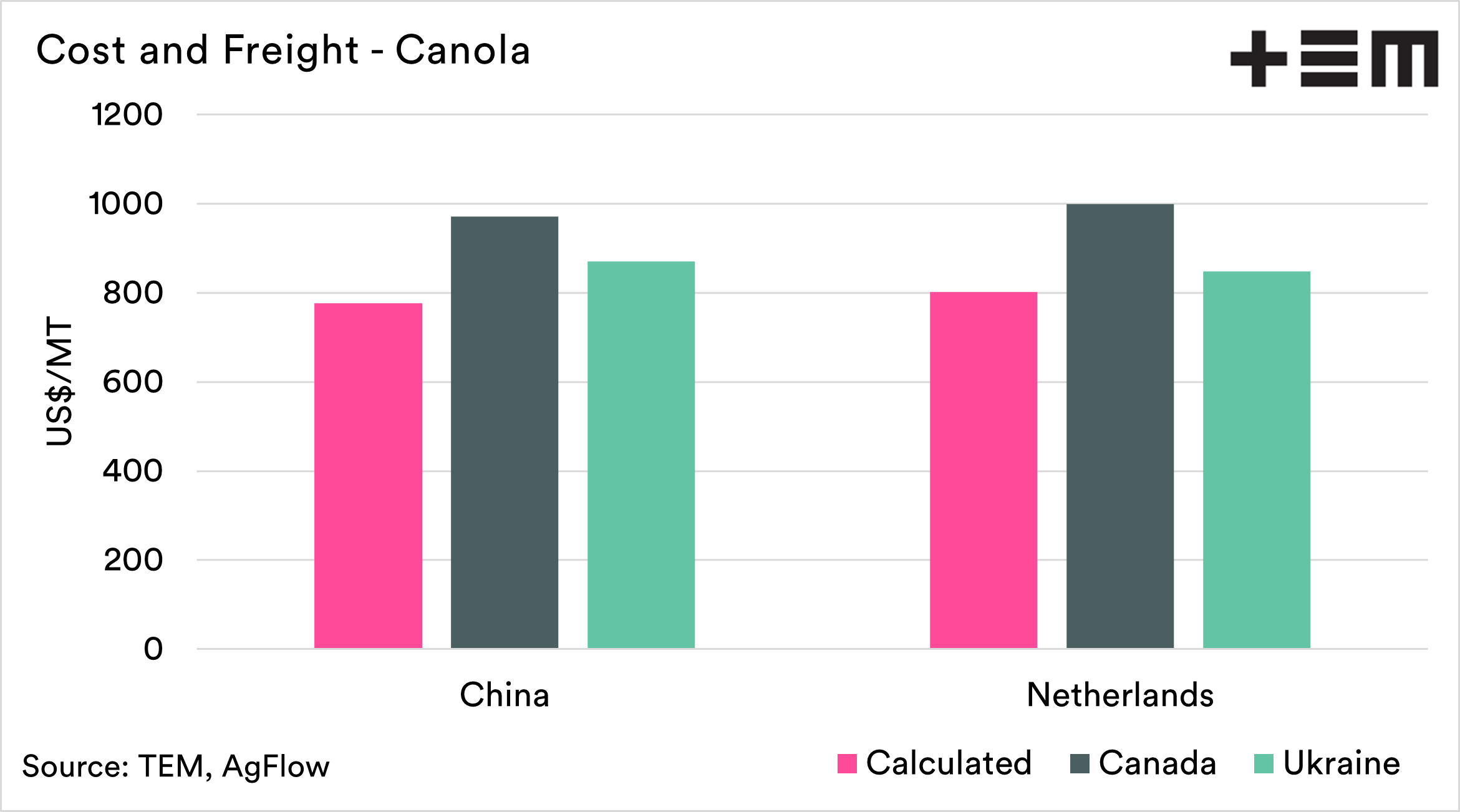

Canola

Canola pricing again is excellent at a grower level when we look historically. Last week, I wrote about our disconnect between our physical pricing and futures (see here). This trend is unsurprisingly similar to the cost and freight matrix.

Canada is pricing exceptionally high due to their drought premium. However, we are also pricing well below Ukrainian levels.

As mentioned many times on EP3, with Canada out of the way (see here) due to drought and now impacted by floods (see here), there is scant availability globally. Whilst substitution is an issue with other oils; we should be in pole position.

To summarise, our grower bids are pricing competitively, and across a range of commodities, we are the cheapest in the world. We are receiving a good price at the moment, but we are still heavily discounted versus the rest of the world.

The wet crop might change some of this……… (see here)

NB: The FOB bids for Australia are not actual traded numbers; these are a calculated price based on the grower bid, taken through to the destination. They are only intended to show the trend. These are being constantly worked on to improve the efficacy with our partners at AgFlow.