Winners and losers in wheat.

The Snapshot

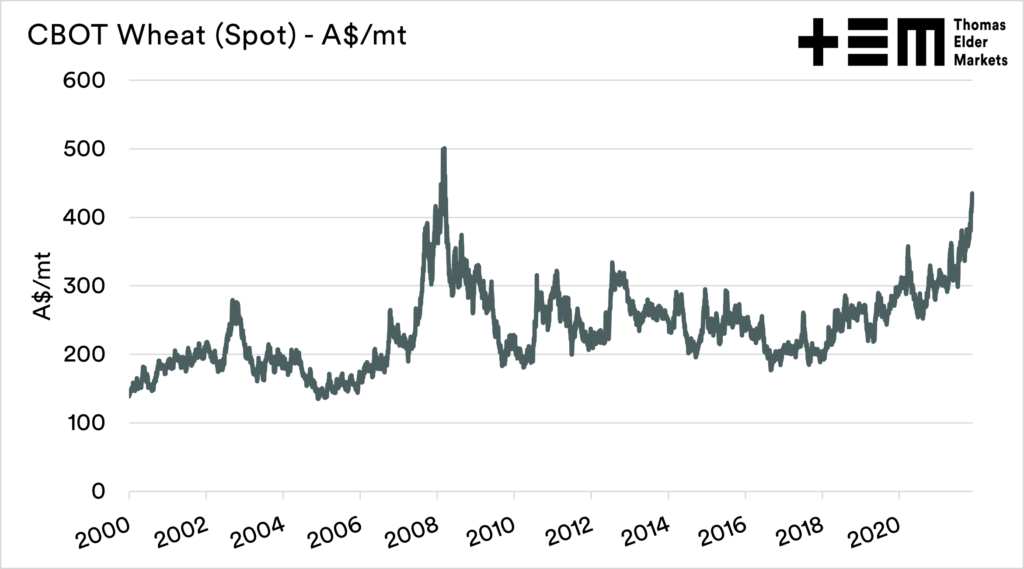

- Chicago wheat is trading at very strong levels.

- In A$ terms, last week the price was ranked 15th highest for the period 2000 to present.

- Our price is largely driven by factors overseas, with the majority of movement explained by futures.

- Basis levels have been low since last harvest, and for November are trading at their lowest levels for a number of zones.

- Our values are discounted to the rest of the world when compared to APW, and even worse when compared to ASW and below.

The Detail

The global wheat market is firing on all cylinders at present. During the past week, Chicago wheat futures traded were trading at the 15th highest pricing point since 2000. We still have got a little bit of distance to go to reach the nominal record, but we are closing in on it.

As an export nation, our pricing levels are heavily dependent upon what happens overseas, so the rise overseas is welcome. However that isn’t all that drives our pricing, and we are currently heavily discounted.

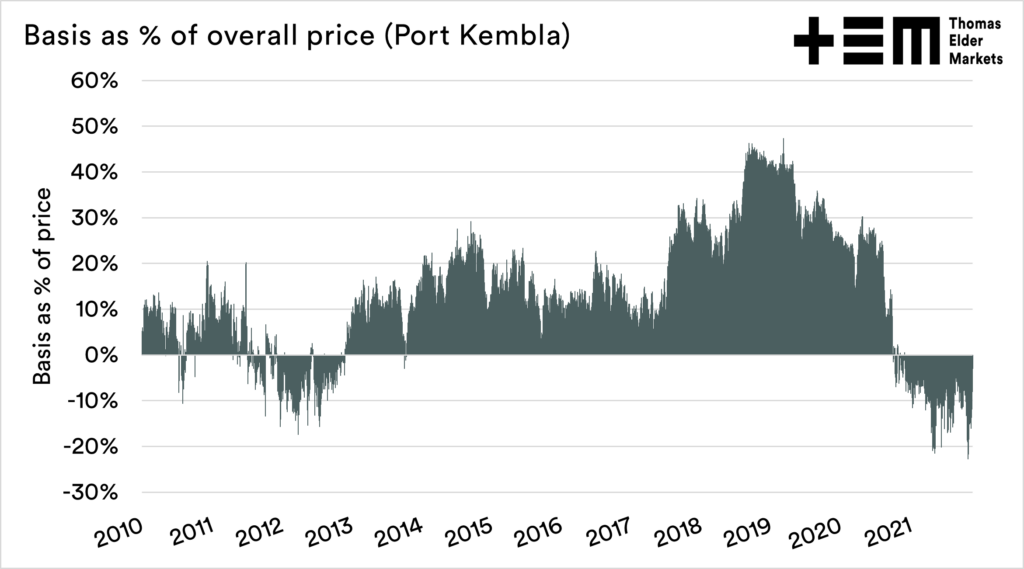

Let’s talk about our basis.

The chart below is a good example of the relative importance of basis. This tracks the percentage of the flat price received by the farmer that is made up by basis for the Port Kembla port zone.

Basis contributes on average 13% over the period 2010 to present. It has been as high as 47% of the overall price. The peak was achieved during the height of the 2018-2019 drought, a time when due to our deficit in supply, Australian wheat prices were achieving very strong premiums versus the rest of the world.

Basis is largely driven by supply; when we have low supply, it is higher. When we have large supplies, it is lower. (You can read more about basis here)

Luckily at present, overseas pricing levels are driving our flat price higher – but our basis is suffering.

How are our basis levels?

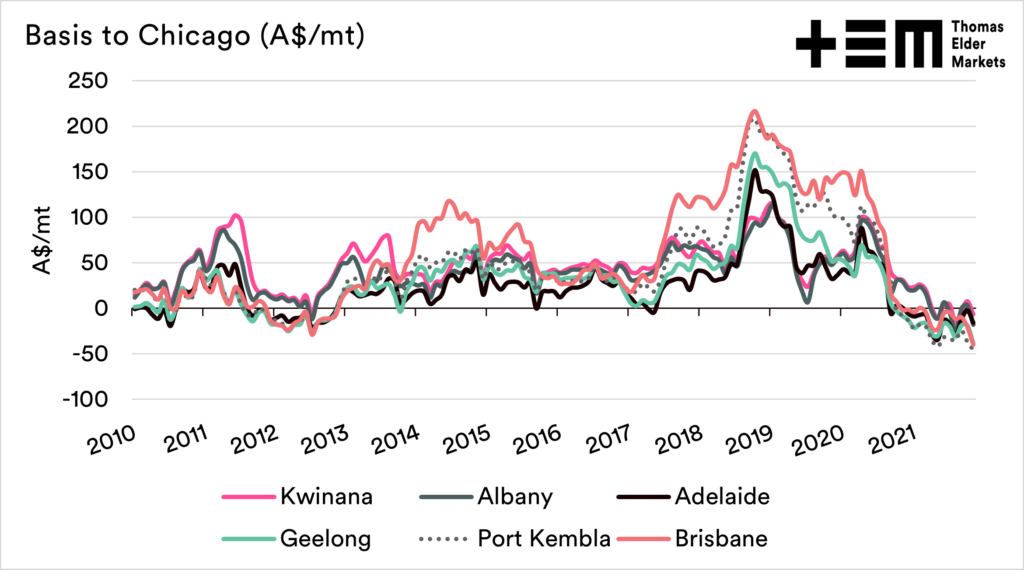

The chart below shows the basis levels for APW wheat against Chicago wheat futures since 2010 on a monthly average. We can see that overall, the basis level around the country is at the lowest levels that we have seen since 2010. These low basis levels have persisted since last harvest.

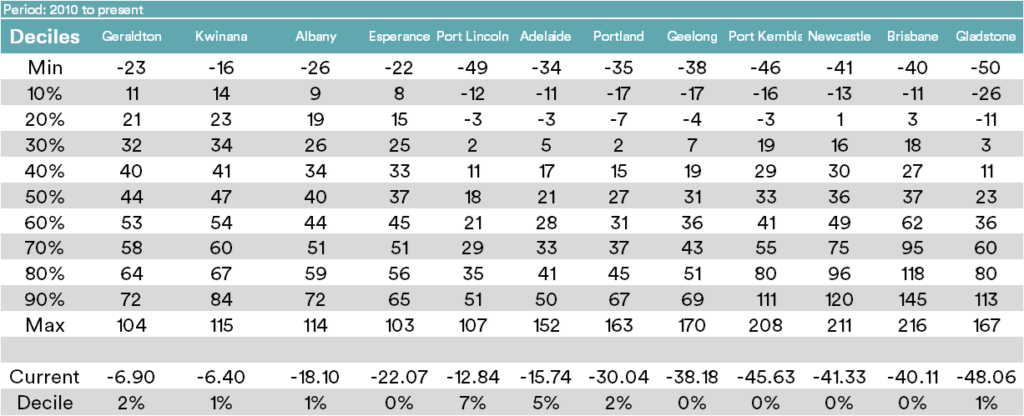

Below the chart is a table of deciles, which gives an indication of how our pricing is compared to history. The decile table shows that November has seen the lowest basis level since 2010 across many port zones.

All zones have basis levels below the 10th Decile.

Our pricing in Australia is extremely cheap compared to Chicago futures. An important point to note is that this is a comparison of APW, and that our other grades ASW (and below) are trading at substantial discounts to APW (see here, here).

We are trading at a time with substantial disparities between grades, between states and with our competitors overseas. Maybe we should be asking for a bit of a bump when we are negotiating with our buyers.